Is Celsius a buy?

Celsius. The New Disruptor! Equity Research! Part 3/3.

Welcome to 3rd and final part of this Celsius Deep Dive. I am Ray Myers and this is Global Equity Briefing!

Excellent stock performance doesn’t guarantee continued growth, however, it also doesn’t mean that the Celsius is done growing! Are there attractive opportunities that Celsius could pursue? Has stock growth been driven by great financials? What about valuation? These questions will be answered!

In Part 1 we discussed how the company came to be and what marketing strategies propelled Celsius to where it is today. Whilst, in Part 2 distribution strategy and the competitive environments were explored. I recommend one reads Part 1 and Part 2 before continuing with Part 3.

1. Opportunities

2. Financial Analysis

3. Valuation

4. Base Case

5. Bull Case

6. Conclusion

1. Opportunities

Now that we understand Celsius business model, let us look at the opportunities!

Growing Industry

For thousands of years and across many cultures people have been consuming caffeine, primarily through coffee and tea. Today both drinks remain extremely popular and are some of the most consumed products in the world. However, energy drinks have been steadily gaining ground and their popularity has exploded in the last 2 decades. In Part 2 of this report, we explored how Red Bull and Monster led the way. With both Red Bull and Monster still growing, can the industry handle another large player?

I believe the answer is clearly yes!

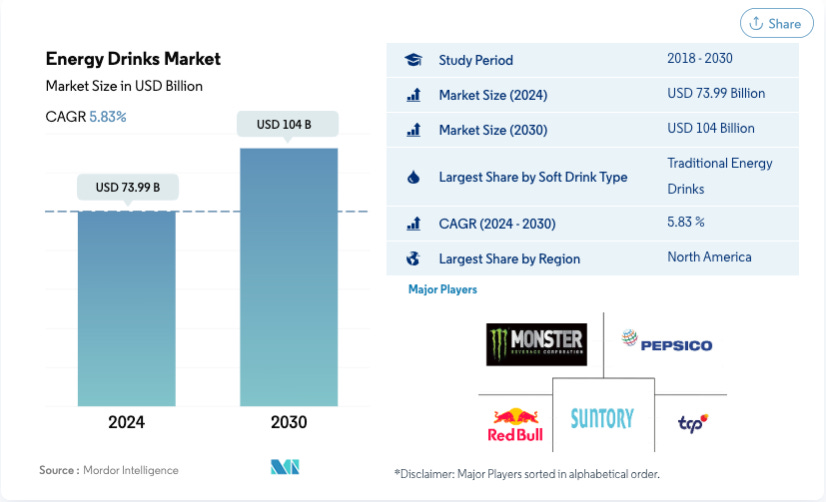

The sale of energy drinks is a massive global industry. Mordor Intelligence estimates the global turnover to reach $74B in 2024. Furthermore, the industry is expected to grow with a 5.83% CAGR, reaching $104B by 2030. With its unique market positioning, Celsius could capture an outsized share of this global growth.

It is way easier to enter a growing market than a mature market!