Is Google a buy?

Google Investment Case!

Google revolutionized how people search for information and created one of the best high-moat businesses in the world!

For over 2 decades, “Google” has been used as a verb when people want to search the internet. Today, however, the narrative around the company is worse than ever. Despite their massive financial success, the age of AI that started with the release of ChatGPT has brought dark clouds over the company.

Many investors believe rather than being the beneficiary of the AI revolution, Google will be one of its biggest victims!

I find this notion ridiculous, and in this Google Investment Case article, I will present my case for why I find the company a great long-term investment, with many positive trends driving its growth story.

In this article, I will look at Search, Cloud, YouTube, Waymo, and the Valuation. Lastly, I will present my take on AI and the Breakup risk!

Let’s have a look!

1. Search

2. Cloud

3. YouTube

4. Waymo

5. AI and the Break-up

6. Valuation

7. Conclusion

1. Search

Search is, of course, Google's largest and most important business. With a 90% global search engine market share, Google dominates this industry. Billions of people use Google every day, generating 8.5 billion queries. Moreover, research suggests that 68% of online experiences start with a search engine, and 93% of all web traffic comes from searches! This means that Search is the most important activity on the internet!

Some have even called Search “the best business in the world” because it essentially functions as an aggregator of the entire internet!

Google captures and organizes our online information in a way that is both indispensable to users and highly monetizable. Its search engine acts as the primary gateway through which people access knowledge, entertainment, and more, making it the ultimate intermediary in our connected digital age.

Intermediary businesses can be very profitable because they act as connectors between supply and demand. People want to consume content(Demand), whilst websites need viewers to earn income(Supply). Google connects the two parties, taking a cut of the economics.

Google’s dominant position and massive scale enable the company to earn extremely stable, high-margin revenue.

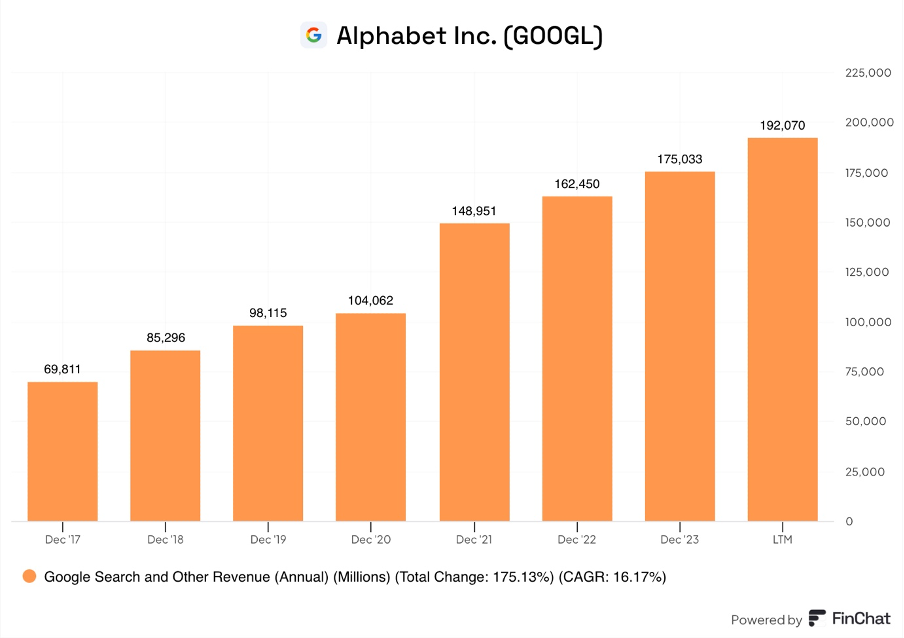

In the last 12 months, as of Q3 2024, this segment earned the company $192B!

In the graph above, we see that despite its already massive scale, search continues to grow at a rapid pace every year. Since 2017,