$180B Fintech Business!

Mercado Libre. More than Amazon! Equity Research! Part 2/3.

Welcome to Part 2 of this Mercado Libre Deep Dive!

In the first part, we talked about how Mercado Libre built its e-commerce and logistics businesses. I recommend readers start with it. Today I will tell you how Mercado empowers the money to flow!

Mercado Libre. More than Amazon! Deep Dive Part 1/3.

For as long as humanity has existed, people have been trading with each other. Apple for an orange, fish for bison, labor for shelter. As we evolved from hunter-gatherers to farmers, to urban city dwellers, the way we traded goods and services changed. People realized that by specializing in what one is best at and trading the output, we could drastical…

When a lack of great financial services slows down e-commerce adoption, it becomes a necessity to offer these services. This is how Mercado Pago was born. Pago is Mercado Libre’s financial platform. Its objective originally was to facilitate transactions on Mercado’s Marketplace, since then it has grown into a comprehensive financial services product.

1. Payment Processing

2. Digital Wallet

3. Loans

4. Mercado Libre Business Risks

5. Part 3

1. Payment Processing

It is not enough to have a great e-commerce marketplace and a reliable logistics service, for e-commerce adoption to continue increasing customers must be able to easily pay for their purchases and have trust in the safety and reliability of the transaction. Mercado understood this early on and developed their in-house payment processing capabilities.

“Through Mercado Pago, we brought trust to the merchant customer relationship, allowing online consumers to shop easily and safely, while giving them the confidence to share sensitive personal and financial data with us.” Mercado Libre 2023 10K

Payment processing is paramount in delivering a great user experience!

If customers experience difficulties when paying, they are less likely to return. Moreover, customers are fickle and can change their minds easily. Therefore, offering many payment methods is extremely important to reduce the likelihood of a customer abandoning the sale during checkout.

What started as an internal payments processing tool has grown into a full-service product that facilitates online and offline transactions through points of sale terminals, mobile phone payments, QR code payments, and credit card, and debit card payments.

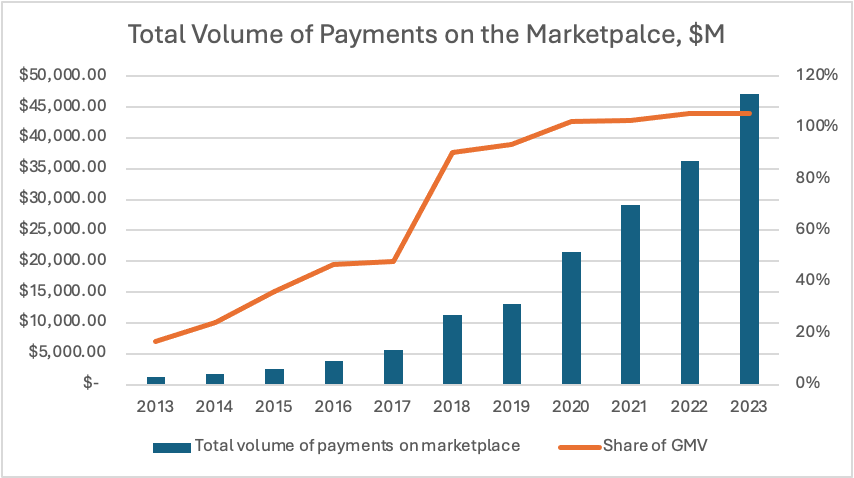

$1.2B of Mercado marketplace payments were processed using Mercado Pago in 2013, around 17% of GMV.

Since then, Pago has grown with a 44% CAGR, processing $47B last year!

In 2023 Pago processed 105% of GMV. Here Mercado’s reporting gets a little bit confusing. The reported GMV includes only Mercado Libre Marketplace transactions. While it seems the volume of payments on the marketplace also includes classifieds, shops, and financing linked to the marketplace. Thus, the share is above 100% of GMV. It would be interesting to see how much of the actual GMV is processed using Pago as it is most likely not 100%.

2. Digital Wallet

Latin America historically has had a high percentage of unbanked people engaged in the “informal economy”. Millions of people work without a formal contract and don’t have bank accounts and credit cards. The World Economic Forum estimated that in 2018 there were 140 million people in Latin America who engaged in some form of “informal economy”. Where legacy banks saw nothing, Mercado saw 140 million potential customers.

“….individuals and micro, small and medium- sized enterprises ("MSMEs”) in the physical world were being underserved or overlooked by incumbent payment providers and financial institutions in Latin America, and that a very large number of retail transactions were still being settled in cash throughout the region “.…….” We envision Mercado Pago as a powerful disruptive provider of end-to-end financial technology solutions that will generate financial inclusion for segments of the population that have been historically underserved and operate in the informal economy today.” Mercado Libre 2023 10K

Pago’s digital wallet allows people to deposit cash into it and then use it not only on Mercado’s platform but also off platform. Customers use the wallet to pay utilities and other bills, transfer funds to other wallets, and withdraw cash if needed.

The adoption of Mercado Pago has been incredible. According to Mercado, Pago is the most popular fintech in Mexico, Argentina, and Chile and the second most popular in Brazil. Since 2020 monthly active users have grown by 130%, reaching 46 million by 2023. As of Q2 2024, 52 million people use Pago every month.

In a mere 6 months, Pago gained 6 million users. Incredible growth!

Pago’s success outside Mercado’s e-commerce marketplace has been outstanding. Since 2013 Pago’s total payments volume has grown with a 53.6% CAGR, reaching $182.8B.

Total payments volume is 409% of GMV, meaning Pago processed 3 times more transactions outside their platform than inside!

Mercado Libre is a massive financial services company that has only started taking market share from incumbents!

3. Loans

A general principle in economics is that the bigger the business the lower the costs for each unit of output. Loans quickly enable businesses to increase the size of their operations, helping them reach economies of scale and reduce unit costs.

Mercado’s 3P platform has thousands of sellers who need financing to purchase inventory, invest in capex, and pay employees!

Conventional banks spend money on marketing to find clients, whilst Mercado can just send an email to their merchants. Additionally, banks require business data and time to analyze it before creating a loan offer. Mercado sees all the sales that go through the platform and can easily utilize this data to assess a merchant’s creditworthiness and quickly and efficiently offer a loan.

Furthermore, Mercado can then withhold loan repayments from the merchant’s ongoing sales, reducing the risk of default. The risk of default is a crucial piece in interest rate calculations as bad loans must be covered by good loans. Thus, Pago can either offer a lower rate or pocket the difference as profit.

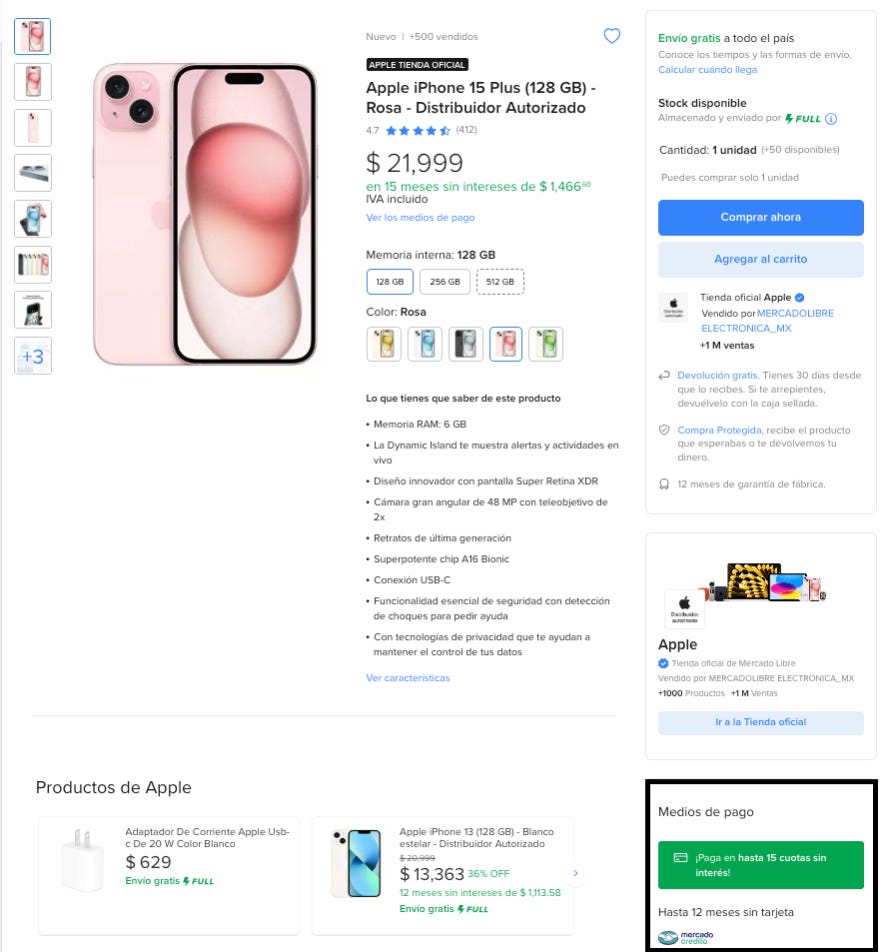

As the owner of the platform, Mercado can participate in both sides of the transaction, funding the seller and the buyer. Here again, Pago has advantages over banks, which need to be quite active at finding potential clients. Whilst Mercado’s platform is used by millions of shoppers, who as you can see in the bottom right corner of the above screenshot, can easily be offered a loan right next to the item.

Digital operations create strong operational efficiencies, coupled with lower customer acquisition costs and better credit underwriting, Pago can service loans at much lower costs than competitors. It costs Pago an estimated $1 per month per client to service a loan. It can cost legacy banks as high as $10 per month per loan in servicing.

Mercado Libre’s ability to service loans at such a low cost positions them advantageously against banks and other fintechs!

It allows them to offer more competitive loan products, with lower interest rates and fees. Additionally, lower cost enables Pago to serve a customer base that might be less profitable for traditional lenders.

4. Business Risks

Weak Economies

During the last 100 years, Latin America has lagged behind the US and Europe in development. However, with the rise of China, and the forecasted fast growth of the Southeast Asian economies of India, Thailand, Vietnam, and Indonesia, many have speculated that it’s Latin America’s turn. However, the latest report from the World Bank sheds doubts on this hypothesis.

“The region’s central task, however, remains boosting lackluster growth rates. The report forecasts that regional GDP will expand by 1.6 percent in 2024. GDP growth of 2.7 and 2.6 are expected for 2025 and 2026. These rates are the lowest compared to all other regions in the world, and insufficient to drive prosperity.” Economic Review | Latin America and the Caribbean. World Bank. April 2024.

Brazil, Mercado’s largest market, is forecast to grow GDP by 1.7%, 2.2%, and 2% in 2024, 2025, and 2026.

Furthermore, despite recent news stories of the manufacturing boom in Mexico, spurred by the US-China trade war, their economy is also forecast to grow at a low rate of around 2% till 2026.

Argentina, the home market of Mercado Libre and the third most important region is expected to have a recession this year, with GDP contracting by 2.8%. However, growth should return in 2025 and 2026, with GDP growing at around 5%.

Weak economies can put pressure on Mercado’s growth plans. Ultimately, if customers can’t afford to put food on the table, they are unlikely to increase spending on Mercado’s platform. Moreover, slow economic growth might force Mercado to reduce prices to sustain top-line growth, contracting margins and leaving less capital for expansion.

Political Instability

Apart from having a weak economy, the region is unfortunately also suffering from political instability.

During the last Brazilian presidential election, an angry mob stormed the capital and attempted to reinstall the previous president. They didn’t have the support of the military, so the attempt was unsuccessful. However, protests caused significant disruptions all around the country, hurting the economy. Luckily, Mercado’s large logistics network enabled the company to weather the storm without significant issues, but there is no guarantee of a similar result if troubles reoccur.

Recently there was an attempted coup in Bolivia. There have been multiple assassinations in the region in recent years. Large parts of Mexico are not controlled by the government, rather they are in complete control of drug cartels.

Argentina is currently dealing with significant changes. Javier Milei, the new president has promised to completely overhaul the economy. Plans to privatize various state companies and reduce the size of the state apparatus have angered powerful unions. Many benefit from the current system and will ferociously resist any changes. Furthermore, even if all reforms are implemented, it’s unclear if Milei’s anticipated results will materialize.

Political instability adds an additional layer of complexity to Mercado’s operations. The company is well-managed and would most likely find ways around any disruptions. However, depending on the magnitude of the next event, the workaround could be incredibly expensive, reducing growth and margins.

Regulation

Weak economies and hectic political climates are great breeding grounds for changing regulations. As Mercado becomes more successful, and profits increase, the company will become a villain in the eyes of many politicians. In Latin America, there is a history of newly elected politicians nationalizing successful and profitable companies in the name of socialism and equality. These attempts rarely deliver the desired outcome for politicians and their citizens. It is extremely unlikely that Mercado’s entire business in a particular country will get nationalized. However, there are other ways how regulators can make Mercado’s life difficult.

There is no unified currency in Latin America, commerce on Mercado’s platform transpires in Mexican Peso, Brazilian Real, Colombian Peso, and others.

In 2023, 52.5% of Mercado’s revenues were denominated in Brazilian Real. I mentioned in the political instability section how the country went through a troubled transition of government. Brazil went from a “far-right” president to a “far-left” one. Any massive change in government policy could significantly damage Mercado’s business in Brazil. Currency devaluation might create inflationary pressures, leading to lower sales and higher costs. Higher taxes might lower the disposable incomes of some Mercado’s customers.

Apart from manipulating currency and increasing taxes, governments can introduce price controls. Price controls are a mechanism that limits the prices of certain goods. When the supply of a particular product is limited, prices can explode. Artificial limitations to the price distort the market and lead to shortages, possibly negatively affecting Mercado’s merchants.

As a commerce platform that sells goods, Mercado is dependent on clear and simple export and import policies. Merchants want to be free to import and sell products without the financial and bureaucratic burden of various duties. Any major changes in import or export taxes could reduce the margins of Mercado’s sellers, thus hurting Mercado.

For a growing financial technology company capital controls are extremely important. Capital controls force companies to keep cash within the country. Their goal is to stop capital flight, and force companies to reinvest it in the country. As a continent-spanning business, Mercado needs capital for reinvestment.

Capital flexibility enables the movement of capital between regions allowing for the highest reinvestment returns. Reducing the cost of capital, increasing revenue growth, and improving margins. However, as capital controls limit cash from moving between regions, they tend to increase the cost of capital, decrease revenue growth, and lower margins. Any new significant capital controls in Brazil, Mexico, or Argentina could significantly affect the business.

Competition

As a large, diversified technology company, Mercado competes with thousands of companies. Small local players, and large multinational corporations alike. Let’s look at some of the big ones.

Amazon

Amazon has conquered the e-commerce markets of the US, Canada, and most of Europe and now has set its sights on Latin America. The company is investing aggressively in Mexico and Brazil. Last September Amazon opened a massive warehouse in Mexico City, its biggest last-mile delivery center to date in Latin America.

Since 2015 Amazon has invested over $3B in its Mexican business and employs over 8,000 people in around 40 warehouses. As of Q4 2023, Mexican operations are profitable and growing. The company has made similar investments in Brazil and has become quite popular. According to a NielsenIQ survey of “Purchase Intention and Top Of Mind", 19% of Brazilians said that Amazon is their main online shopping brand.

As of Q2 2024, Amazon has $89B of cash and equivalents on its balance sheet. Amazon is an extremely well-capitalized competitor who as its growth domestically slows is increasingly looking to emerging markets for growth. However, Amazon doesn’t have the first-mover advantage, local know-how, or fintech products. Moreover, Amazon’s marketplace network effects are not as strong in Latin America as domestically. Mercado is in a strong position to defend their leading market share.

AliExpress

AliExpress is the international e-commerce segment of the Chinese company Alibaba. As of April 2023, with almost 410 million visits monthly, it was the second most visited online marketplace in Latin America.

AliExpress has a reputation for selling cheap goods manufactured in China. Thus, the company is highly popular with low-income households. Since the pandemic, Alibaba has grown its international sales by almost 200%, reaching $14.2B in FY 2024. It is unclear how much of this growth is attributable to Latin America as the company doesn’t disclose it.

Similar to Amazon, AliExpress is a large well-capitalized competitor who is increasingly looking for growth outside its domestic market. Thus, it is likely that competition with AliExpress will intensify in the coming years!

Other Commerce Players

Shopee is an E-commerce company owned by a Singapore-based technology company SEA Limited. Apart from managing Shopee, Sea has a fintech and a video game platform. The company has had significant success in Southeast Asia and has expanded to Brazil. Sea Latin America sales reached $2.2B in 2023, growing by 178% since 2020.

Shopify has a large commerce platform that helps merchants manage various aspects of their business. It competes with Mercado Shops product. Their presence in Latin America is relatively small, with just $69 million in revenue in 2023, but it is growing.

Furthermore, Mercado Libre competes with dozens of local e-commerce platforms in various countries and niches. Mexican online sneaker stores, Brazilian online beauty retailers, and Chilean electronics shops. Mercado Libre truly competes with almost each and every store selling something in Latin America.

Financial Services Competitors

In financial services, Pago competes with a broad range of companies.

Its payments processing business competes with such companies as Adyen, Stripe, PayPal, StoneCo, PagSeguro, and dozens of other players.

Pago’s digital wallet solution competes with large local and multinational banks. Pago is especially eating their lunch with the new generation, who value a great app and convenience. Pago offers simple and easy loan application procedures that save its customers time and money. Many legacy financial institutions provide an inferior customer experience.

However, it is increasingly becoming apparent that one of the biggest competitors is Nu Bank. Nu Bank is a digital-only Brazilian fintech with over 100 million clients in Latin America. Nu has grown extremely quickly and is continuously expanding its footprint. As Pago continues to develop new financial services products they will start stepping more and more into Nu’s playground. While as Nu creates new products the company is likely to enter some areas that Mercado dominates.

As Pago and other fintechs grow in popularity, legacy banks will become increasingly aggressive and corrupt in how they compete. Likely trying to use their influence with politicians and government institutions to stifle fintech expansion.

Part 3

Now that we have discussed the main aspects of Mercado Libre’s business model we will look at the financials. Is Mercado Libre profitable (Yes) and how could the business look in the future? What are the biggest opportunities? And most importantly, the valuation will be analyzed and explored.

Thank you for reading, Follow me on:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

I included your parts 1 and 2 in my links Monday compilation post: Emerging Market Links + The Week Ahead (August 19, 2024) https://emergingmarketskeptic.substack.com/p/emerging-markets-week-august-19-2024

latam is a crazy market, new battleground for global players.

wonder where walmart stands.

will it ever make sense for ML to enter North AM market and give it back to amazon.