Meridian Holdings Q1 2026: Back to GAAP Profitability!

Small cap trading 4x EV/ADJ EBITDA whilst growing topline at 17% and ADJ EBITDA at 26%

Meridian just released a great Q1 earnings report, reaching GAAP net income profitability of $2.3M, the first real profit quarter since the merger.

The market liked the results, with the stock ending the day up 3.7% and 29% in the past week.

Rebranding to Meridian is completed.

Best revenue growth in 4 quarters.

Strong ADJ EBITDA growth of 26%.

Net leverage ratio down to 0.53x.

After a complex merger and a major rebranding effort, the company has proven that its diverse business model can generate cash while expanding into some of the most valuable gaming markets in the world.

This report provides a detailed look at the results of Q1 2026, exploring the performance of individual business segments and the broader strategic moves that have strengthened the company’s position.

Disclosure: This is Issuer-Sponsored Research

Let’s begin.

1. Overall Performance

Revenue: $50.1M +17.3% Y/Y

Gross Profit: $28.1M +16%, margin of 56%

ADJ EBITDA: $6.3M +26%, margin of 12.6%

EBIT: $3.2M vs -$0.11M last year

Net Income: $2.3M vs -$0.26M last year

EPS: $0.18 vs -$0.02 last year

OCF: $5.2M -33.4% Y/Y

The narrative for the Q1 2026 is one of growth, efficiency, and a successful return to profitability.

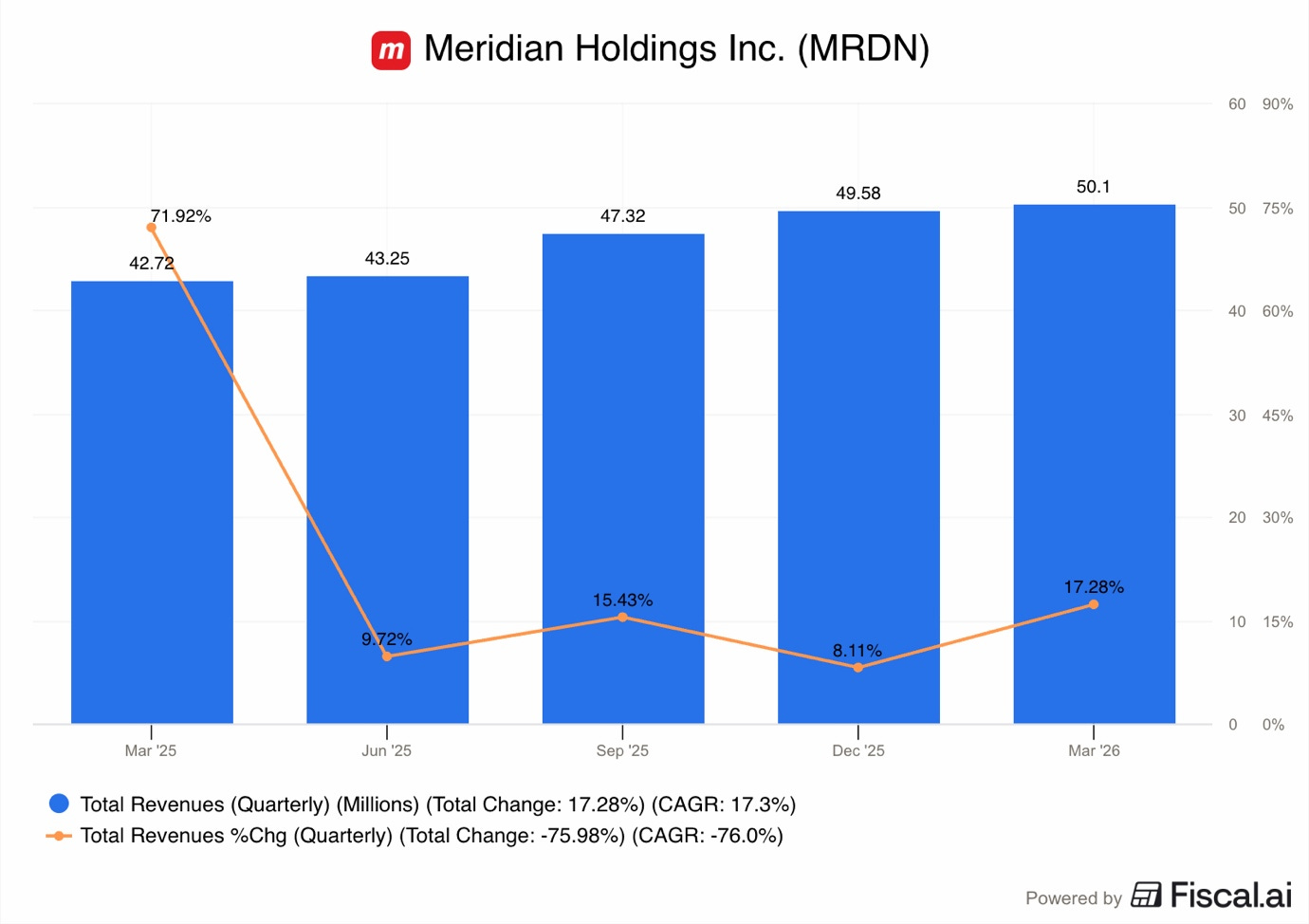

1.1. Revenue

Meridian reported total revenue of $50.1M, which is a 17.3% increase from $42.7M in Q1 2025.

As you can see in the chart above, this is the fastest growth in 4 quarters and the best performance since the merger consolidation!

This growth is quite impressive, considering it occurred while the company was undergoing a reorganization and merger integration.

The ability to grow sales by double digits while reorganizing the company suggests that the underlying business is very healthy and that customers are increasingly attracted to its betting and gaming products.

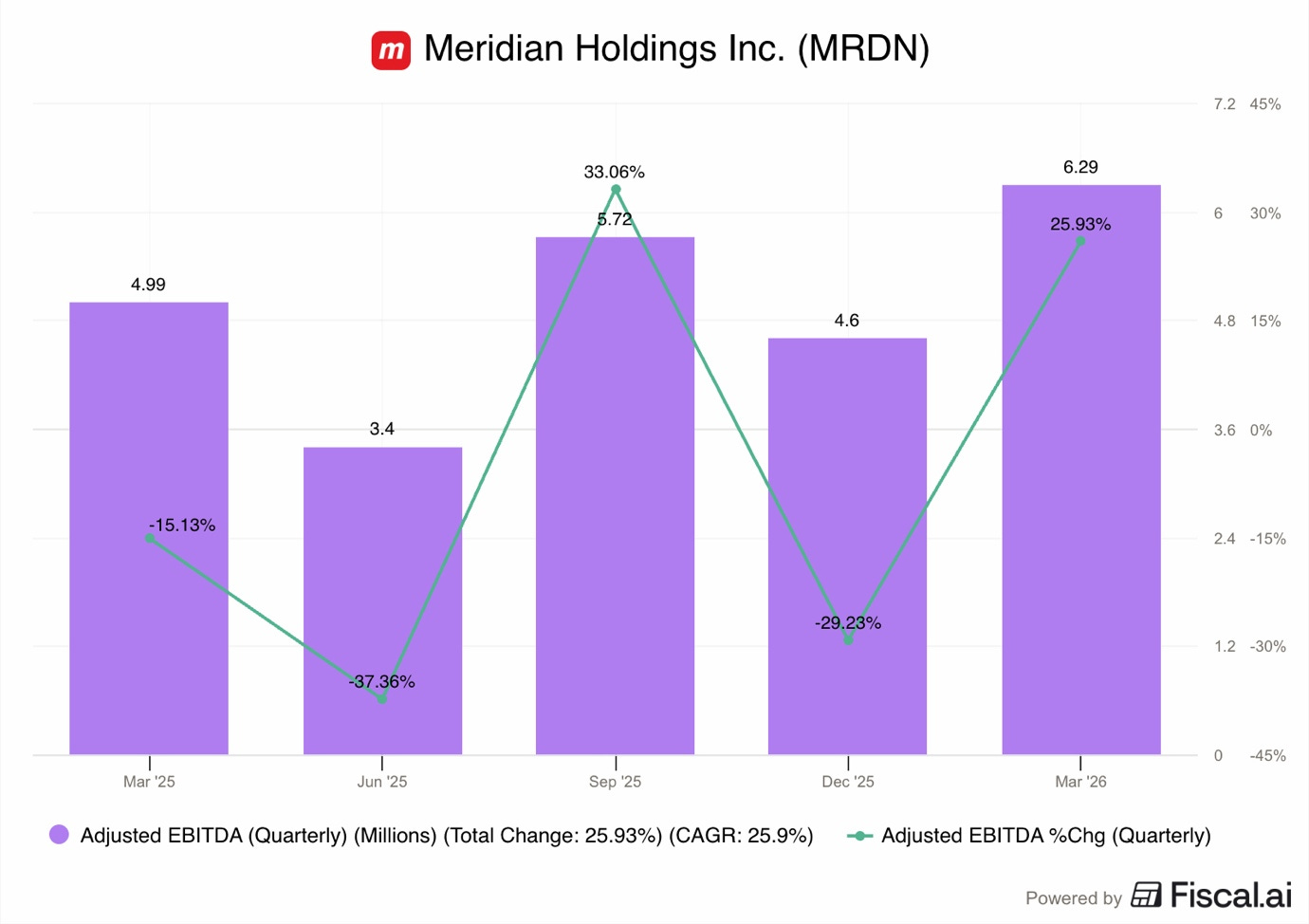

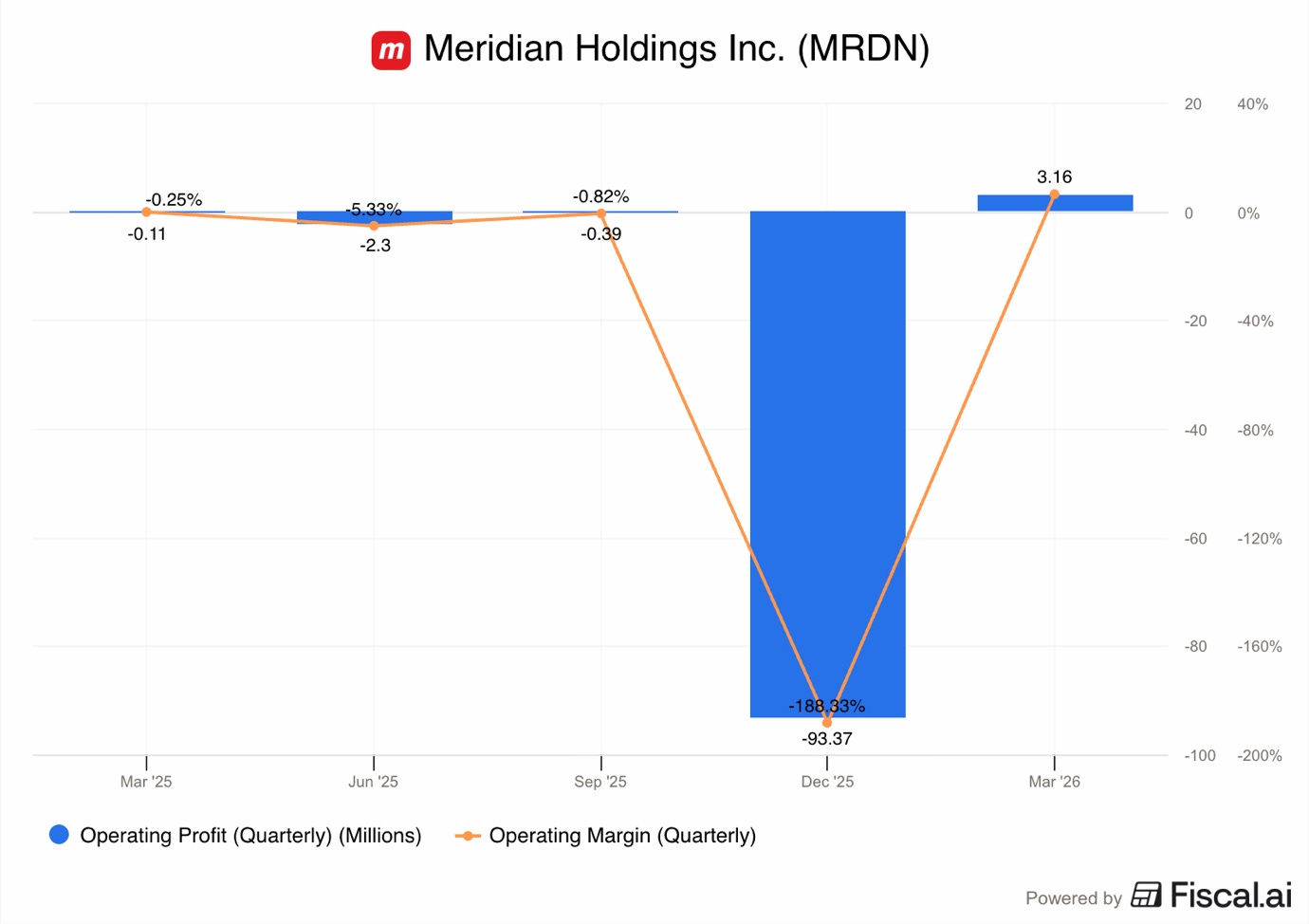

1.2. Profitability

Meridian reported an ADJ EBITDA of $6.3M for the quarter, a 26% Y/Y increase and a beat of the company’s guidance of $6.1M.

As you can see in the graph above, this was the best result in 5 quarters!

The ADJ EBITDA margin rose to 12.6%, up from about 11.7% in Q1 2025. This margin expansion is a clear indicator that the company is becoming more efficient and its growth strategy is delivering results.

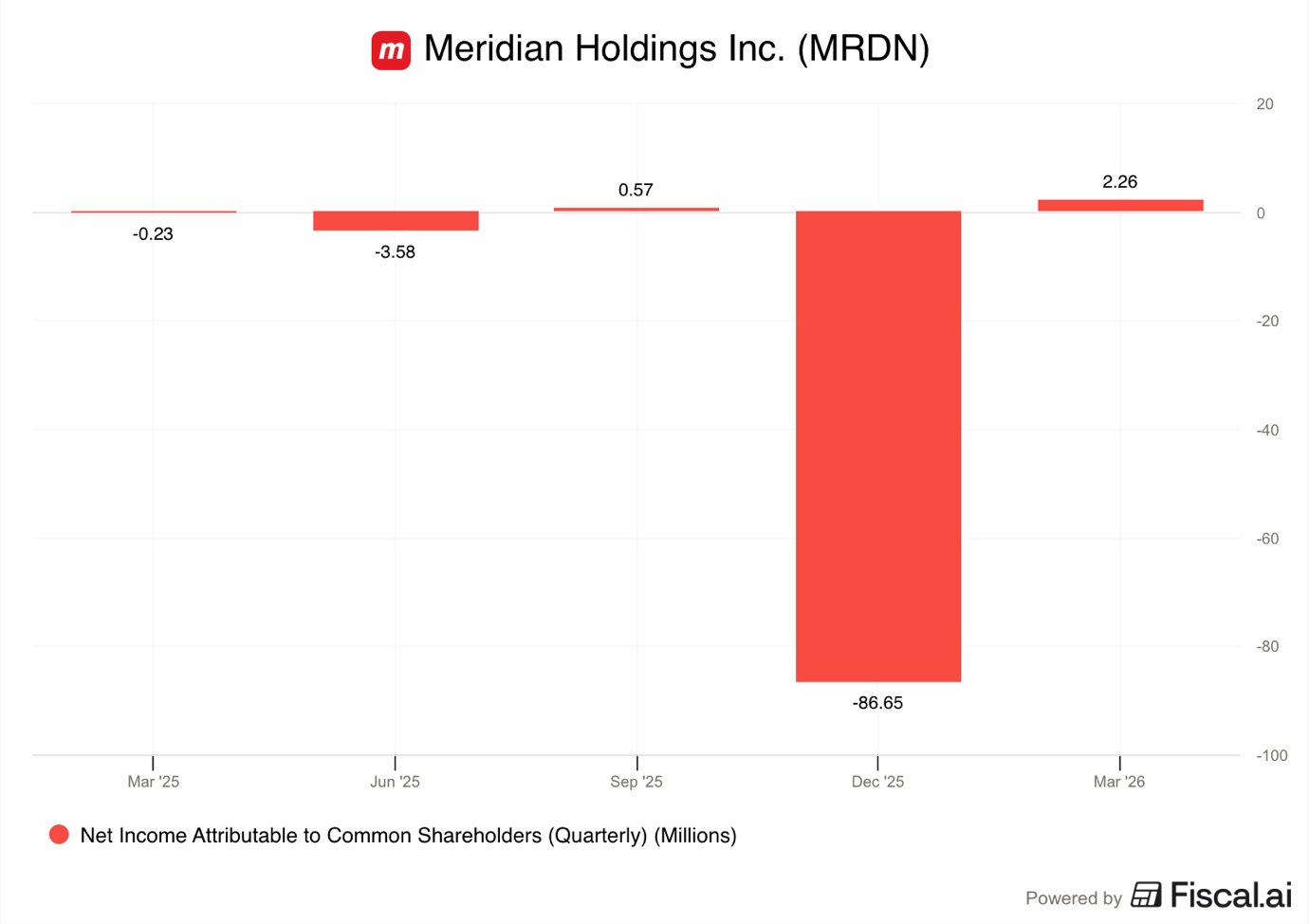

However, the most important news is that GAAP net income reached $2.3M.

One year ago, the company recorded a net loss of $230K.

This is a welcome development after the large loss last quarter, driven by goodwill and intangible asset impairment.

A reminder that last quarter, Meridian recorded an impairment charge that reduced the balance sheet value of goodwill and intangible assets by $91.8M.

This was a non-cash accounting entry, meaning it does not impact the company’s actual bank balance or daily operations.

When a business gets acquired, it is usually for a premium to the accounting value of its net assets. In such situations, the acquirer records the difference between the purchase price and the net asset value of the acquired business as goodwill on the consolidated balance sheet.

Companies pay a premium to the accounting value of net assets because they expect the acquired business to grow earnings. And we are seeing that the Meridian is now delivering strong earnings growth.

As of Q3 2025, Meridian had $129M of goodwill and other intangible assets on the balance sheet.

US GAAP requires yearly tests to assess whether that goodwill position is appropriate. Rules require that the goodwill position be reduced in certain situations when the share price goes down, interest rates increase, or some business units underperform. This reduction appears on the income statement as a loss.

These impairments, while disappointing, don’t change the core investment thesis of the company as they mostly affect the less interesting parts of the business.

We see that the company has reached a tipping point where revenue is growing faster than expenses, allowing more money to flow to the bottom line.

Let’s see what enabled Meridian to achieve such an improvement.

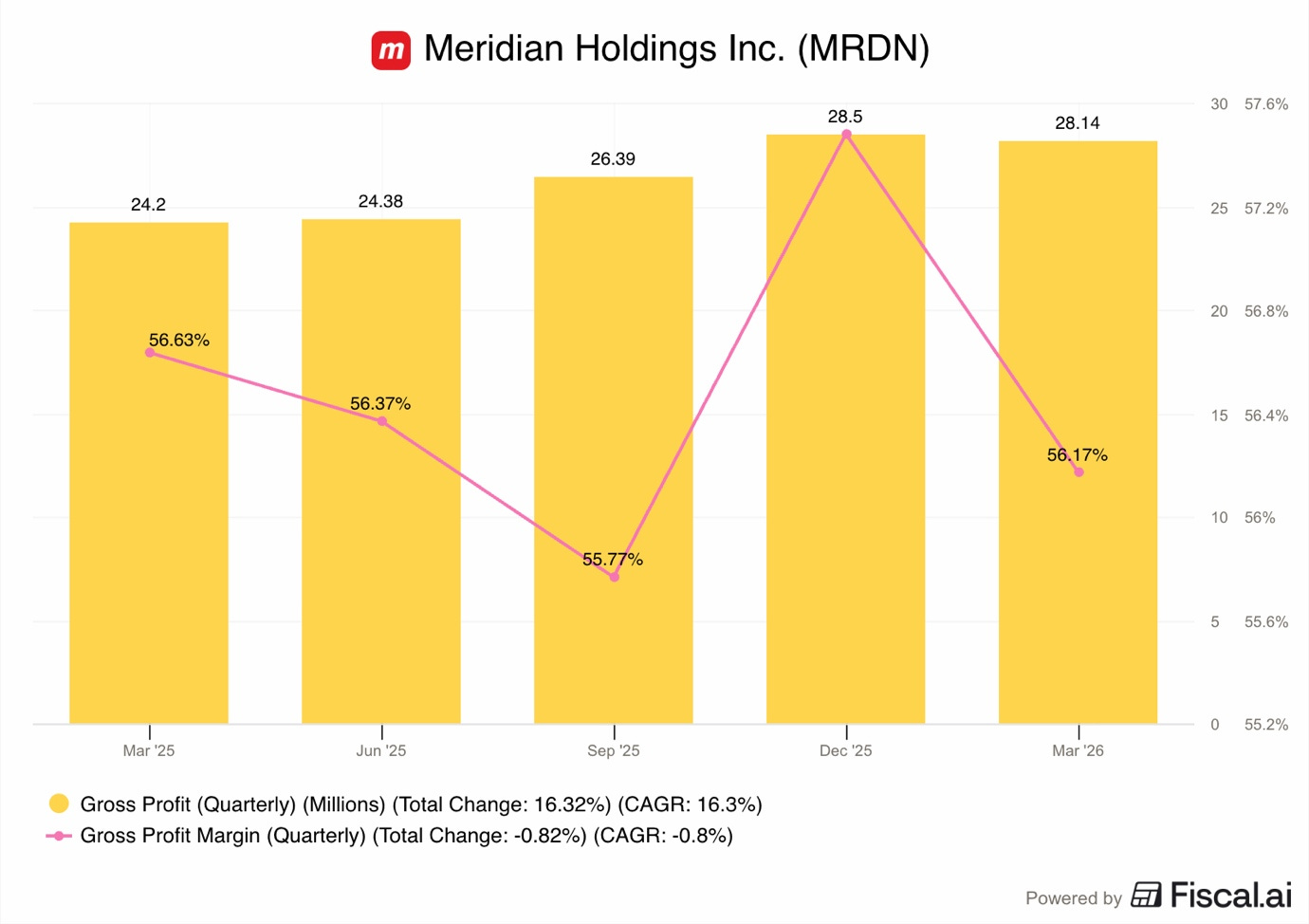

To understand how the company makes money, we must look at its gross profit, which rose 16% to $28.1M.

For a company like Meridian, gross margin shows what’s left after paying the winnings and the direct costs of serving the games and bets.

As we can see in the chart above, compared to Q1 2025, gross margin remained steady at 56%, while gross profit improved by $4M.

This stability demonstrates that the company is managing its costs well, even as it grows in new B2C markets like Brazil and Mexico, and B2B markets like the US and Canada, which incur very high startup costs.

Moreover, the operating profit was $3.1M, a massive turnaround from the small operating loss seen in Q1 2025.

This improvement happened because the SG&A increased only by 2.8% to $25M, compared to the revenue growth of 17%.

This is a clear example of Meridian improving its operating leverage, as it uses its existing infrastructure, technology, and staff to handle more business without linear expense growth.

1.3. Balance Sheet

Meridian significantly improved its balance sheet stability, countering a key bear narrative of excessive debt.

The company has been aggressively paying down the debt it took on to merge Meridianbet with Golden Matrix.

As of Q1 2026, the company’s total debt was $29.7M, down 54% from $64.4M.

If we look at net debt, which is the total debt minus the cash the company has in the bank, the figure fell by 62% to just $13.4M.

Meridian now has a net debt leverage ratio of 0.53x, which is very healthy.

Simply put, the company is generating more than enough income to cover debt obligations, giving it meaningful financial flexibility to invest in its business or new M&A.

The company ended the quarter with $16.2M in cash, which is down 45.3% Y/Y as it pays down debt.

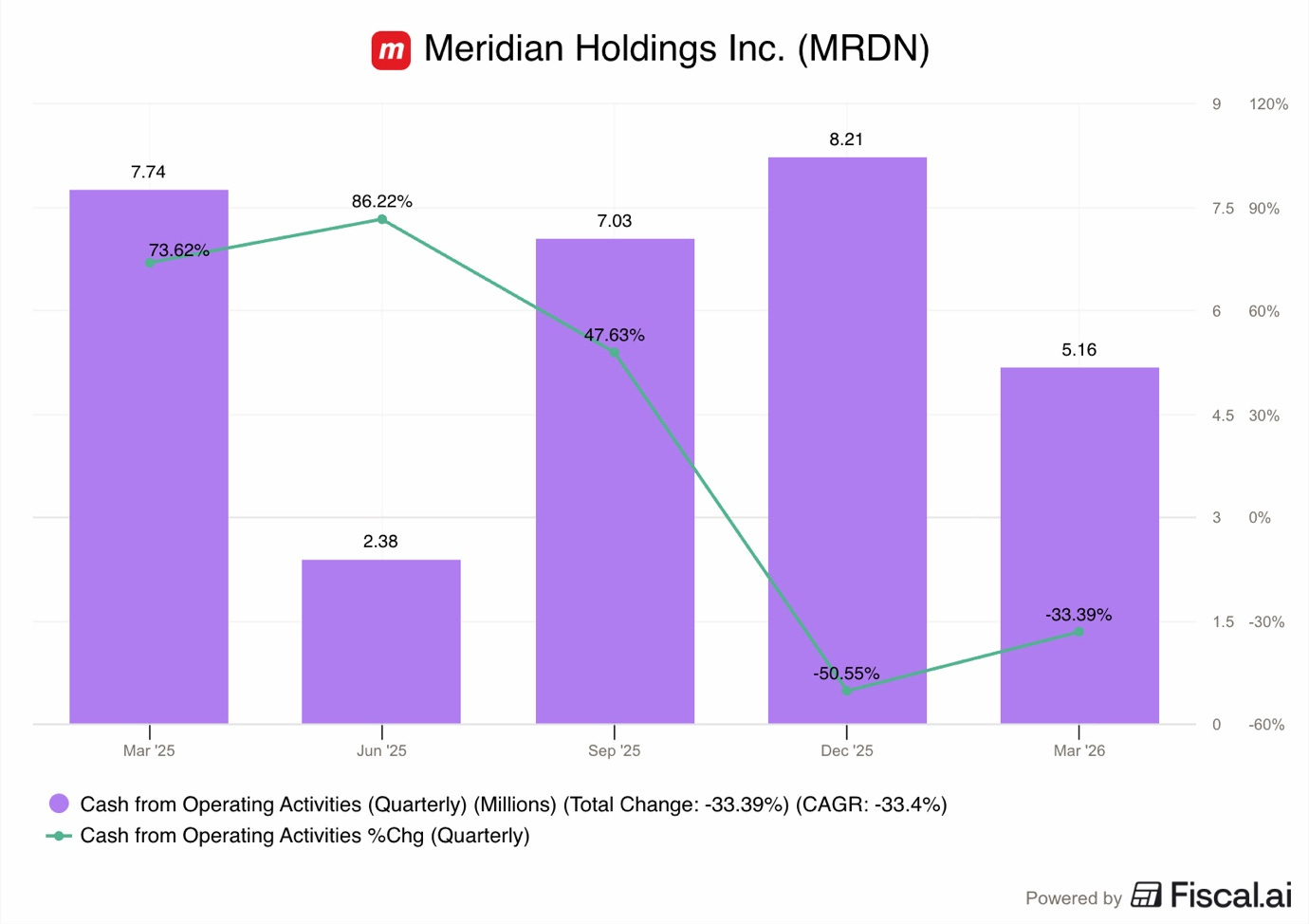

1.4. Cash Flow

Meanwhile, operating cash flow fell by $2.58M, -33.4% Y/Y to $5.16M!

As you can see in the chart above, OCF is a very lumpy metric that fluctuates a lot depending on profitability and cash outflow.

While this quarter, net income grew by $2M, Meridian paid $1.72M in accounts payable compared to last year, when it built up $4.3M in additional accounts payable during the quarter.

ADJ EBITDA is a great proxy for OCF, as it essentially shows what OCF would be if we ignored the timing of receivables and payables.

1.5. Guidance

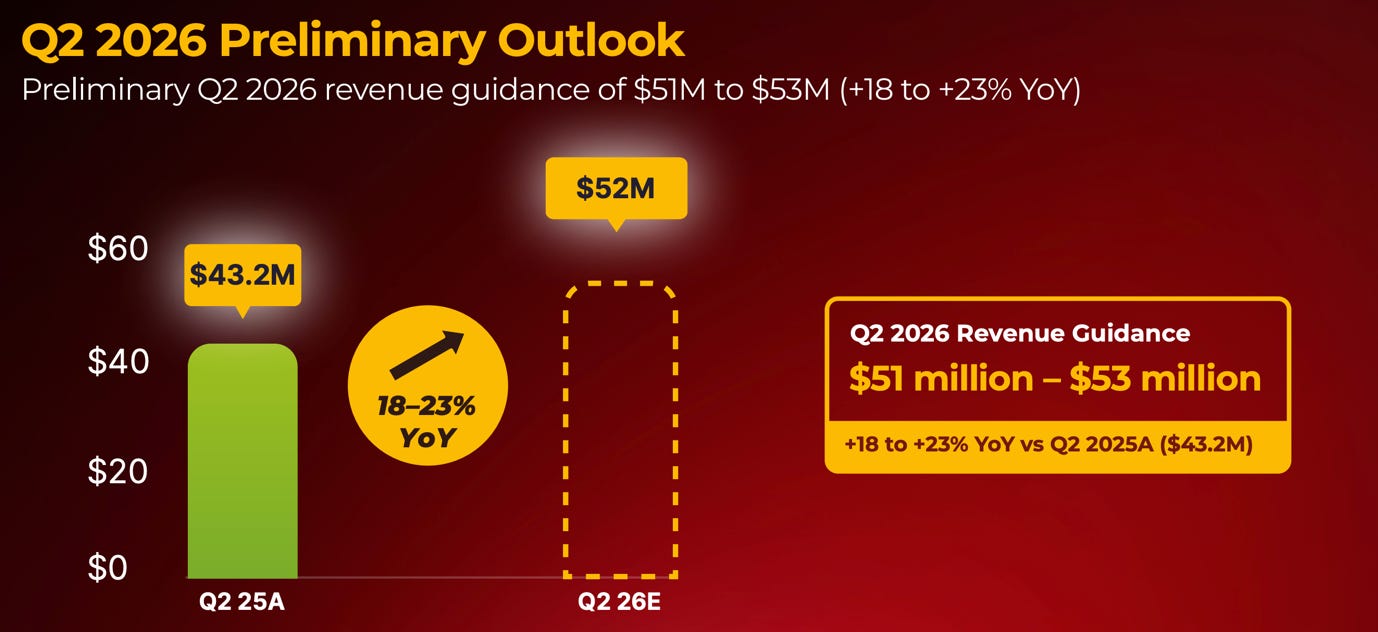

Based on this strong performance, the company has issued positive guidance for the second quarter of 2026.

Management expects revenue to be between $51-53M, which would represent Y/Y growth of 18% to 23%.

This is slightly above the analyst consensus estimate of $51.6M.

2. Meridianbet

Meridianbet segment is the core engine of the company, accounting for 70% of total group revenue.

This segment runs online sports betting and casino games across more than 18 regulated countries in Europe, Africa, and South America.

In Q1 2026, Meridianbet generated $34.9M in revenue +26% Y/Y!

This growth is coming from both the online side of the business and the company’s network of 740 betting shops.

The success of Meridianbet is driven by a massive increase in the number of people using the platform.

During this quarter, the brand signed up 428K new customers, a 41% increase compared to the same quarter in 2025.

This is a clear sign that the company’s marketing efforts are working well.

More importantly, these new users are becoming active players with the number of depositors rising by 27% to 283K, and the total number of active users grew by 21% to 334K.

This segment is also highly profitable, with a gross margin of 69.3% and an operating income of $6.6M. The 37% Y/Y growth in operating income for this segment suggests that the company is getting more value out of each customer.

3. Expanse Studios

Expanse Studios is the creative core of the company. While Meridianbet focuses on letting people bet, Expanse Studios focuses on building the actual online casino games.

In Q1 2026, Expanse continued to grow its footprint.

Its games are now available on 1,519 different operator sites, which is 175 more than at the end of last year.

The studio launched six new proprietary games this quarter, bringing its total collection of titles to 77.

Additionally:

The number of players grew by 156%

Revenue grew by 345%

Pay-ins grew by 218%

Gross gaming revenues grew by 133%

It is clear that this segment is delivering explosive growth. The revenues of Expanse are included in the Meridiabet segment revenues.

Furthermore, one of the most important moves this quarter was a new partnership with QTech Games, a leading distributor in emerging markets. This deal allows Expanse’s games to be offered to millions of new players in the Americas, where online gaming is just starting to take off.

The studio also introduced social casino versions of its games, which allow people to play for fun without betting real money, helping to build brand awareness and letting people test their gaming strategies.

To sell games in new regions, a studio must have its software tested and certified by the local government.

Expanse has been very successful in getting these stamps of approval.

During the first quarter, the studio secured new certifications in:

Latvia

Estonia

Sweden

Portugal

Furthermore, it is also waiting for certification in Ontario, Canada, and New Jersey, US, which are some of the biggest gaming markets in the world.

This business is very scalable, as by obtaining these certificates, Expanse can grow its revenue with limited capital investment.

Once scaled, the studio could become a potentially high-margin part of the business.

4. RKings and Classics

The RKings and Classics for a Cause segments are focused on prize competitions.

This is a unique type of e-commerce where people pay a small fee to enter contests to win luxury items like sports cars, houses, or vacations.

RKings is Meridian’s competition business based in the United Kingdom.

In Q1 2026, it generated $7.7M in revenue, a 12% increase over the previous year.

This was driven by the average order value, rising 29% to $16.91.

Furthermore, the value the company gets from each new person who registers went up by 15% to $17.72.

This segment is undergoing a transition in strategy, where they focus on attracting fewer but higher-value customers.

These improvements show that the company is getting better at marketing and is attracting these higher-value customers who are more engaged with the platform.

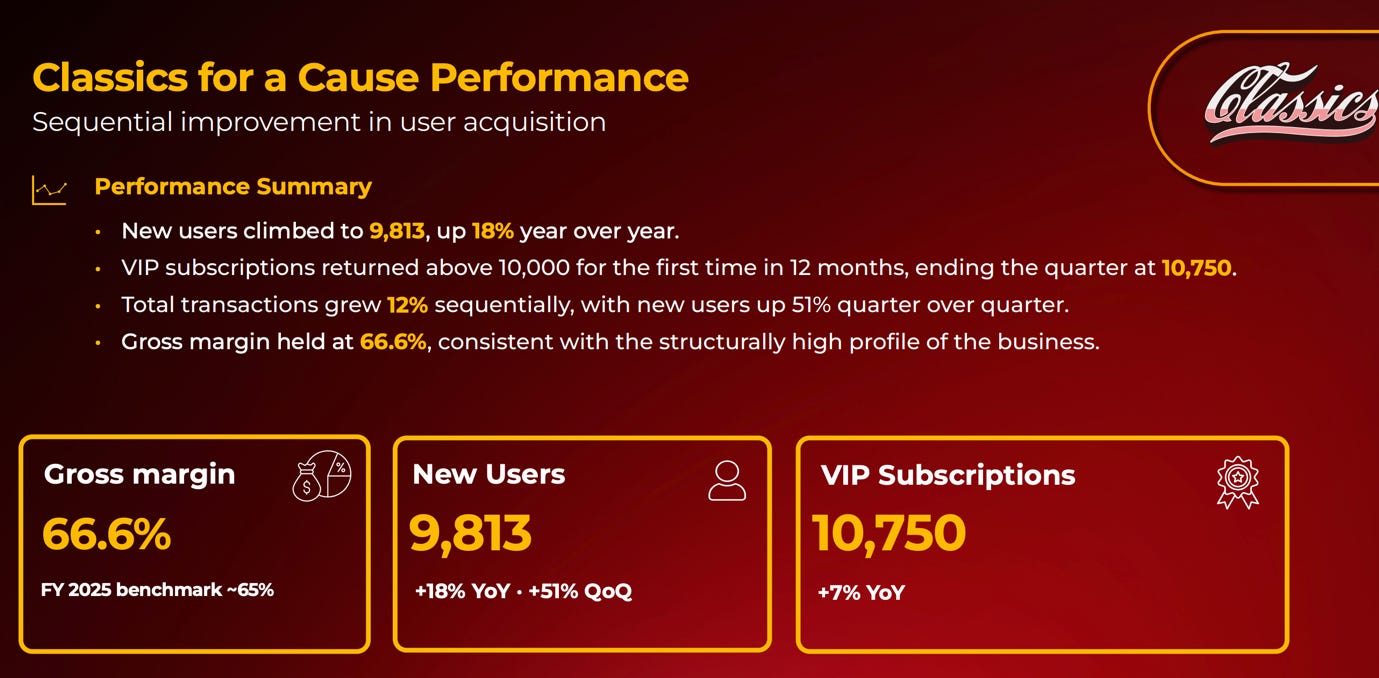

Classics for a Cause is an Australian business that focuses on car raffles.

Unlike RKings, which mostly sells single tickets, Classics for a Cause has built a promising subscription model.

People pay a monthly fee to be VIP members, which gives them regular entries into prize draws.

During Q1 2026, the number of VIP subscribers passed 10,000 for the first time in a year, ending the quarter at 10,750.

Meanwhile, the number of new users rose 18% to nearly 10,000, and the total number of transactions increased by 12% compared to Q4 2025.

Overall, this segment grew revenues by 4.3% to $4.4M!

5. GMAG

GMAG is the company’s casino game aggregator business focused on Asia, that’s been underperforming lately.

In Q1, the GMAG segment reported revenue of $3.1M, which was a 18.4% drop from the $3.8M it earned a year earlier.

This segment is not only a drag on the group’s revenue growth, but also on profitability. Gross margin is 33.9%, and the segment lost $0.4M this quarter.

To counter this slump, the company is focused on improving the GMAG offering.

During the quarter, the segment added 12 new game providers, which is a huge increase from only adding 2 providers in the same period last year.

It also added 1,382 new games to its platform.

By adding more providers and more games, GMAG is aiming to become more valuable to casino operators.

6. Mexplay

Mexplay is the company’s Mexican online casino and sports betting brand.

While it is currently a small part of the overall group, it is growing at an incredibly fast pace.

The number of people signing up for Mexplay grew by a staggering 271%, reaching a total of 74,000 registered users.

Even more important is that the number of first-time depositors rose by nearly 200% to 6,101 people, while first-time deposit value grew by 183% to $61K.

This shows that Mexplay is successfully converting people into paying customers.

The success of Mexplay is not just about the money it makes in Mexico, it is a test case for how the company can enter other Spanish-speaking countries.

By learning how to market to Mexican players and follow the local rules, the company is building a playbook that it can use as it expands across Central and South America.

7. Valuation

A market cap of $95M, TTM revenues of $190M, and adjusted EBITDA of $20M implies that the company is trading for 0.5x P/S and 4.4x EV/ADJ EBITDA.

That compares favorably to competitors.

In the above picture, you see the P/S, EV/EBITDA, and revenue growth of some key gambling companies.

Flutter trades for 2.5x the Meridian’s P/S multiple and 3x the EV/EBITDA multiple, despite comparable revenue growth.

Meanwhile, Draftkings are signficiantly more expensive than Meridian, despite growing top-line only slightly faster.

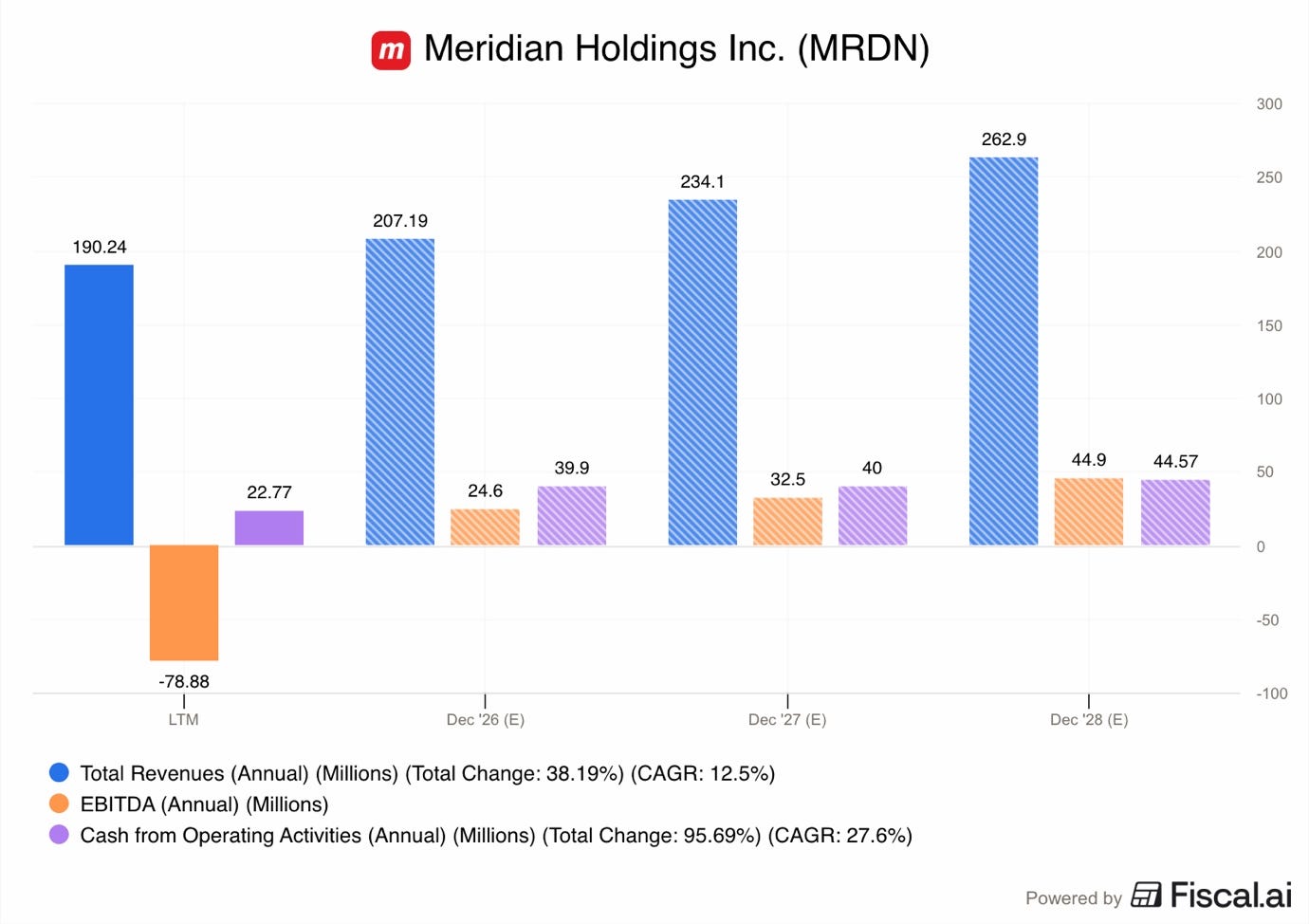

Looking at a few years in the future, the analyst consensus 2028 estimate revenue sits at $263M, EBITDA at $44.9M, and OCF at $44.6M.

Implying a 2028 P/S of 0.3, EV/EBITDA of 2, and EV/OCF of 2.

A key catalyst that could bridge the valuation gap between peers is full-year GAAP net profitability. Once that is reached, Meridian will begin to appear in stock screeners that demand it.

As a small-cap with a market cap below $100M, the company is hard to discover in a sea of thousands of publicly traded companies. Screeners are a crucial tool that investors use to discover such companies.

If the current financial trajectory continues, that could happen after Q4 2026 results.

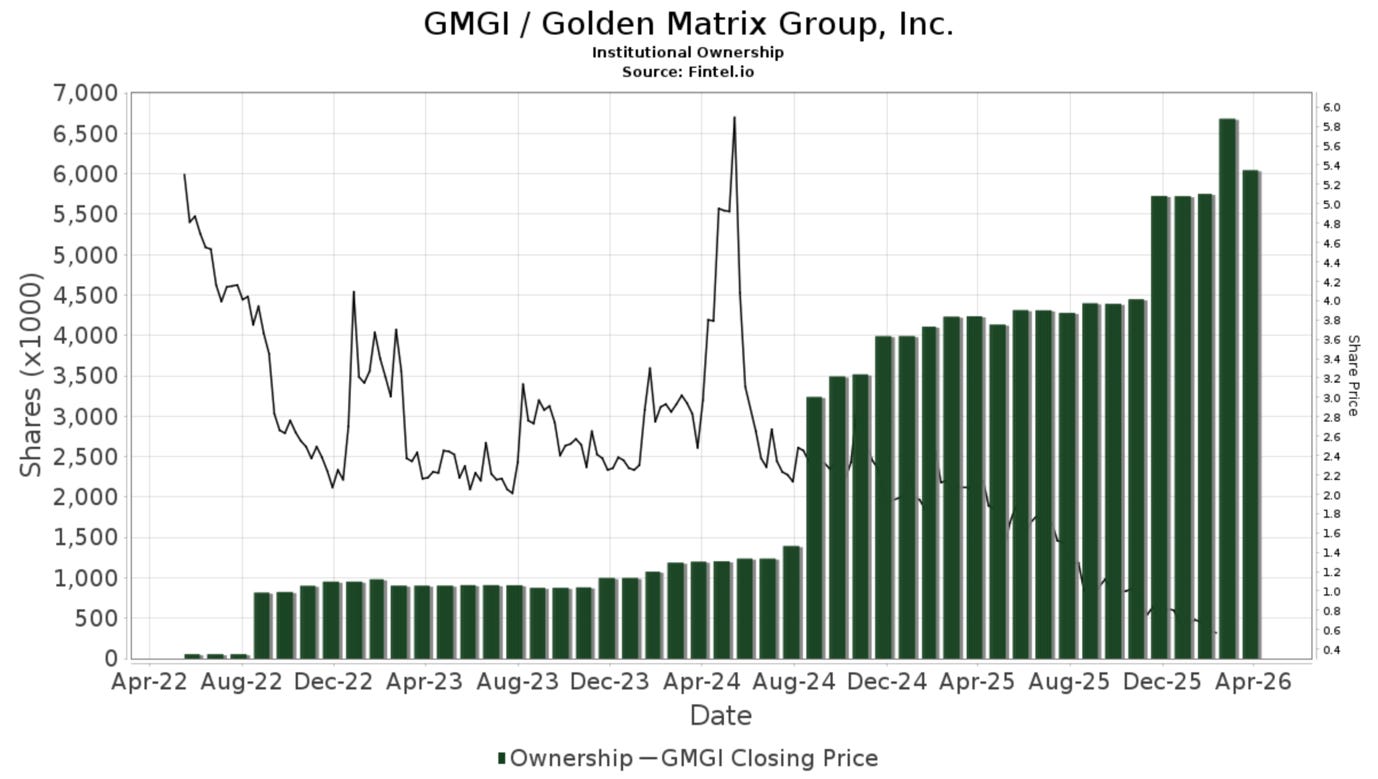

And institutions are front-running this possible catalyst.

As you can see in the chart above, per Fintel.io, while there was a small decrease post Q4 2025 results, overall institutional ownership has been growing steadily as the share price has gone down, up from 1.5M shares in August of 2024, to over 6M by April 2026.

Smart money is seeing value here!

8. Valuation Model

Let’s build a quick valuation model.

It is hard to adequately estimate the growth of the RKings, Classics, and GMAG segments. So, I am going to model a modest 5% CAGR.

For Meridian, they reported $5.33M in revenues from Latin America in 2024, so I am assuming that all of it relates to MexPlay and the recent entry into Brazil.

Meridian, excluding Brazil and Mexico, I model them growing with a 9% CAGR till 2030. This mostly consists of the core business in Europe and the expansion in Africa.

Regarding Mexico and Brazil, I model a rapid expansion, reaching revenues of $68M in 2030.

As per the 2030 forecasts, the Mexican industry would generate $2.52B in revenues, the Brazilian $3.9B. So to get revenues of $68M, Meridian would only need a market share of 1.1%. This seems a very reasonable and achievable market share target.

In such a scenario, total revenue could reach $312.6M, a CAGR of 11%!

Modeling the operating margin reaching 14%, and tax, interest, and other expenses of 30% of operating income.

Net income could reach $30.6M in 2030, a margin of 9.8%!

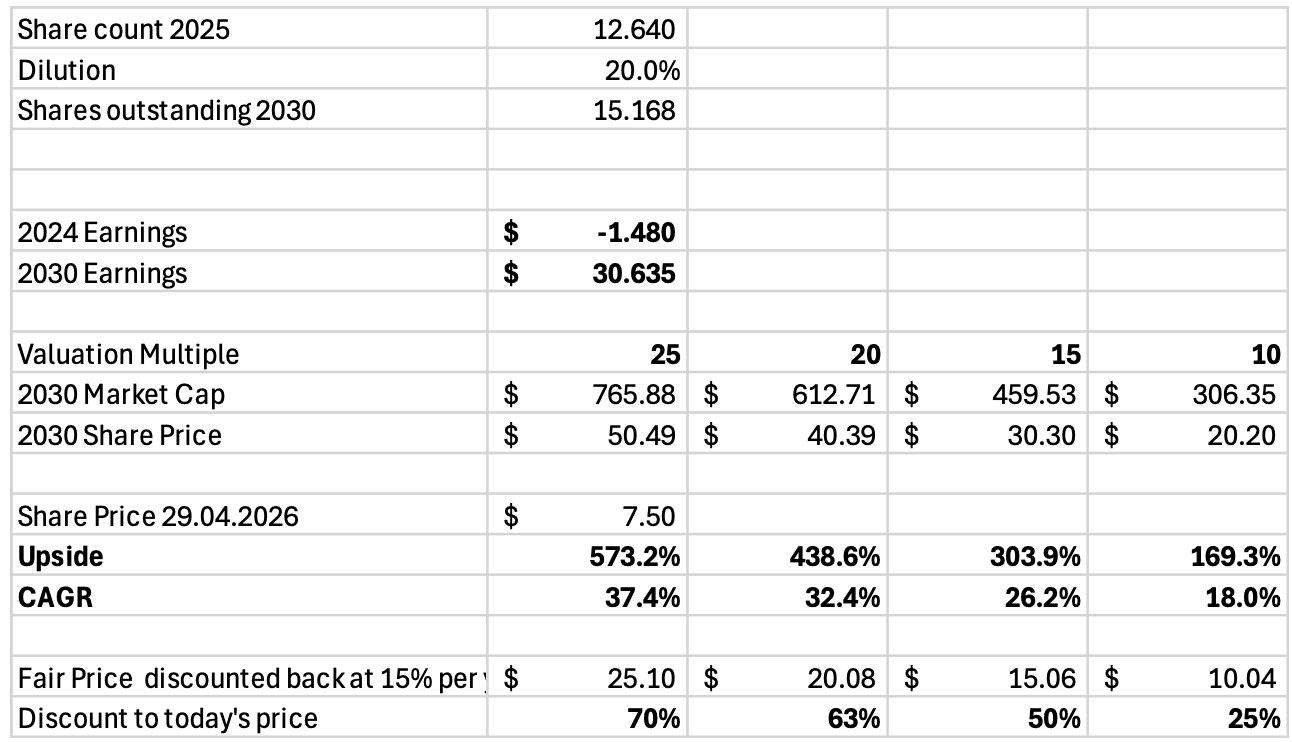

Next dilution. I am going to model 15.168M shares outstanding in 2030, an increase of 20% in 5 years. This assumes that a significant portion of the remaining acquisition debt gets converted into equity.

If the Meridian trades for a P/E of 15-20, we could be looking at a $460-613M market cap company and a $30-40 stock in 2030.

That would be an upside of 304-439% from today’s share price of $6.85!

Discounting it back at 15% per year to calculate a fair value per share, we get $15-20, implying that currently the company might be trading for a 50-63% discount to its fair value.

9. Conclusion

Q1 2026 has been a period of remarkable progress for Meridian.

The company has successfully moved from a period of heavy investment and occasional losses into a state of steady, GAAP profitability.

By growing its revenue 17% and returning over $2.2Min profit, the company has proven that its strategy of integrating successful brands like Meridianbet, Mexplay, Expnase, and RKings, and Classics is working.

Furthermore, the company’s decision to focus on its strongest brand, pay down its debt, and invest in AI technology has made its financial position the strongest in its history.

With a net debt leverage of only 0.53x and $16.2M in cash, the company is well-prepared to handle the required investments to achieve its growth strategy.

Looking ahead, the company is well-positioned for continued success. The upcoming 2026 World Cup and the full launch in the Brazilian market provide huge opportunities for more growth.

So, in conclusion, Meridian appears to be undervalued compared to what its peers are trading at. As the valuation model showed, there is further potential for strong upside.

But execution is the key!

Integration needs to go smoothly, and operational synergies must be achieved.

Legacy markets in Europe must continue to grow.

The company shouldn’t experience any issues in Africa, Brazil, or Mexico.

If that happens, Meridian Holdings could make its shareholders very happy.

The company has gone through a transformation, from a largely B2B driven to B2C. The synergies that this vertical integration can deliver have yet to be realized by the market.

However, as always, investing in small caps comes with additional risks, and this is not a guaranteed slam dunk.

Nevertheless, the business does look promising.

Disclosure:

This report is Issuer-Sponsored Research. Global Equity Briefing has entered into a research and distribution agreement with Meridian Holdings Inc ($MRDN). The compensation may create a conflict of interest; however, the Analyst maintains editorial independence and all opinions expressed in this report are strictly his own. The Analyst agrees not to trade Meridian securities during the period of the agreement. The compensation received is a fixed fee and is not contingent upon the content of the report or the performance of the issuer’s securities. This is not a recommendation to buy or sell any security. Global Equity Briefing is not a registered broker-dealer or investment adviser.

Thank you for reading Global Equity Briefing!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.