Micron: The AI Memory Supercycle!

US memory chip manufacturer experiencing AI-driven, Nvidia-like demand growth for its chips!

Welcome to Global Equity Briefing, my weekly investing newsletter.

I am Ray, a passionate investor and equity analyst. And today I am covering Micron!

For 50+ years, the memory industry was viewed as a brutal, cyclical commodity market.

Companies in this space were prone to extreme boom-and-bust cycles, where periods of high profitability were quickly followed by devastating oversupply and price collapses.

However, the rise of AI has fundamentally changed this dynamic.

Micron is transitioning from a cyclical commodity manufacturer into a structural enabler of AI.

Last quarter, the company grew revenues by an insane 196% and net income by 770%, reaching a net margin of 58%!

These types of results are unheard of for an industrial company of such scale and remind us of the stratospheric growth of Nvidia in 2024.

In this Micron Deep Dive, I will examine what is driving the growth and whether the company remains an attractive long-term investment opportunity.

Let’s begin.

1. Business Model

2. Manufacturing Strategy

3. Customers

4. Risks

5. Opportunities

6. Financials

7. Valuation

8. Valuation Model

9. Conclusion

1. Business Model

Micron is the only major American manufacturer of memory chips.

During the 1980s and 1990s, the memory industry went through brutal price wars initiated by Japanese and later South Korean competitors. Dozens of American memory makers were forced into bankruptcy or exited the market.

Micron survived through a relentless focus on cost-efficiency and strategic acquisitions. The 1998 purchase of Texas Instruments’ memory business and the 2013 acquisition of Japan’s Elpida Memory were key moments.

The Elpida acquisition, in particular, doubled Micron’s capacity and secured its position as a primary supplier for Apple’s iPhone.

In 2026 its Micron’s core products include:

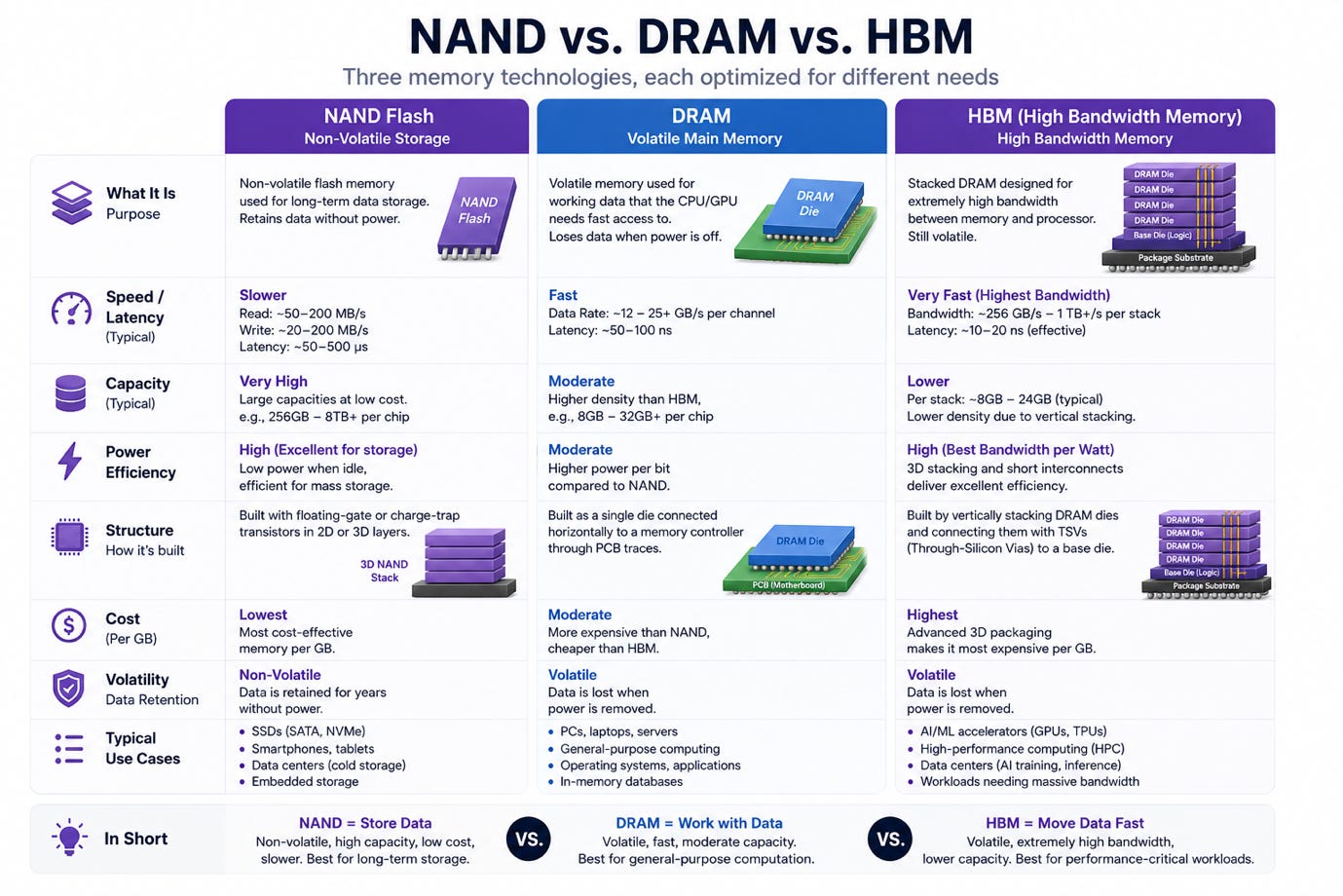

DRAM

HBM

NAND Flash

NOR Memory

Let’s expand on them.

1.1. DRAM

DRAM is the short-term memory of any computer system.

It provides a high-speed workspace where the processor stores data for immediate access. Unlike storage, DRAM is non-permanent and volatile, so the data is lost when power is removed.

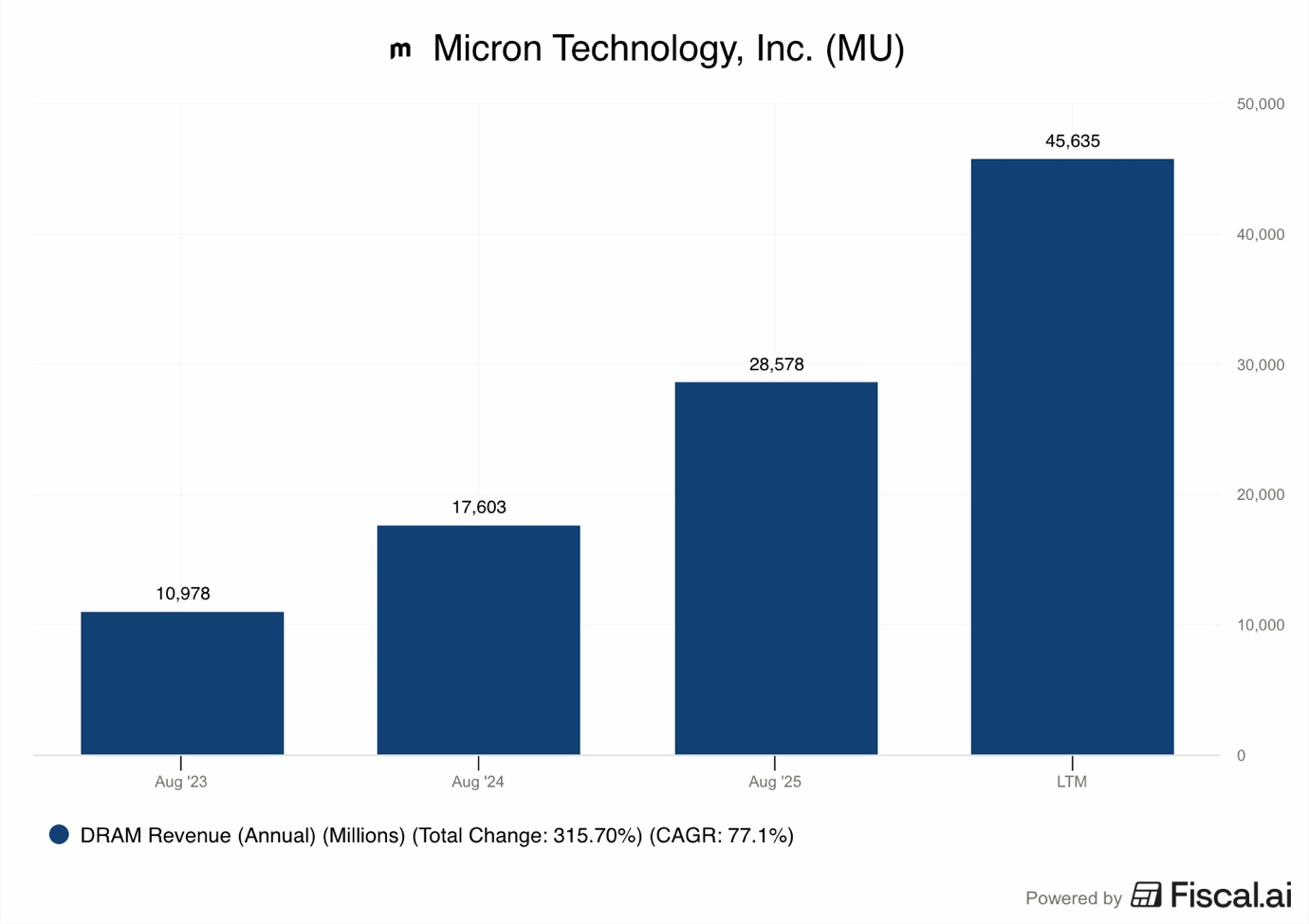

DRAM is by far the largest product category, generating $45.6B in LTM and 78.5% of total revenues!

This is also the primary growth area for the company, with Micron growing DRAM revenues by a mindboggling 207% in Q1 2026.

The growth is driven by the fact that the memory requirement for AI servers is much larger than that of traditional enterprise servers. While a standard server might require a few hundred gigabytes of RAM, an AI-optimized server requires up to 8 times the DRAM to handle the massive datasets and parameters of AI models.

Simply put, thanks to the AI boom, DRAM has transitioned from a supporting component to the primary enabler of LLMs.

Micron’s current leadership in this space comes from its 1-gamma node, which is the most advanced DRAM manufacturing process in the world.

The 1-gamma node is expected to become the highest-volume node in company history and is on track to represent the majority of the DRAM bit mix by the middle of calendar 2026.

This technology provides several benefits for AI:

Bit Density: 45% increase on 1-beta node, allowing for more memory in the same space.

Latency: 17% lower latency for AI inference tasks.

Energy Efficiency: 24% better energy efficiency, reducing data center power costs.

As AI models grow in size, they require more DRAM capacity per server. Previous generation servers use several hundred gigabytes of DRAM, but new AI-optimized platforms are pushing these requirements into the terabyte range.

This change creates a structural increase in the total addressable market for DRAM, improving on the simple replacement cycles.

In short, by utilizing ASML’s EUV machines, Micron has been able to increase bit density and improve power efficiency, which is a must for data centers where electricity costs are a major driver of costs.

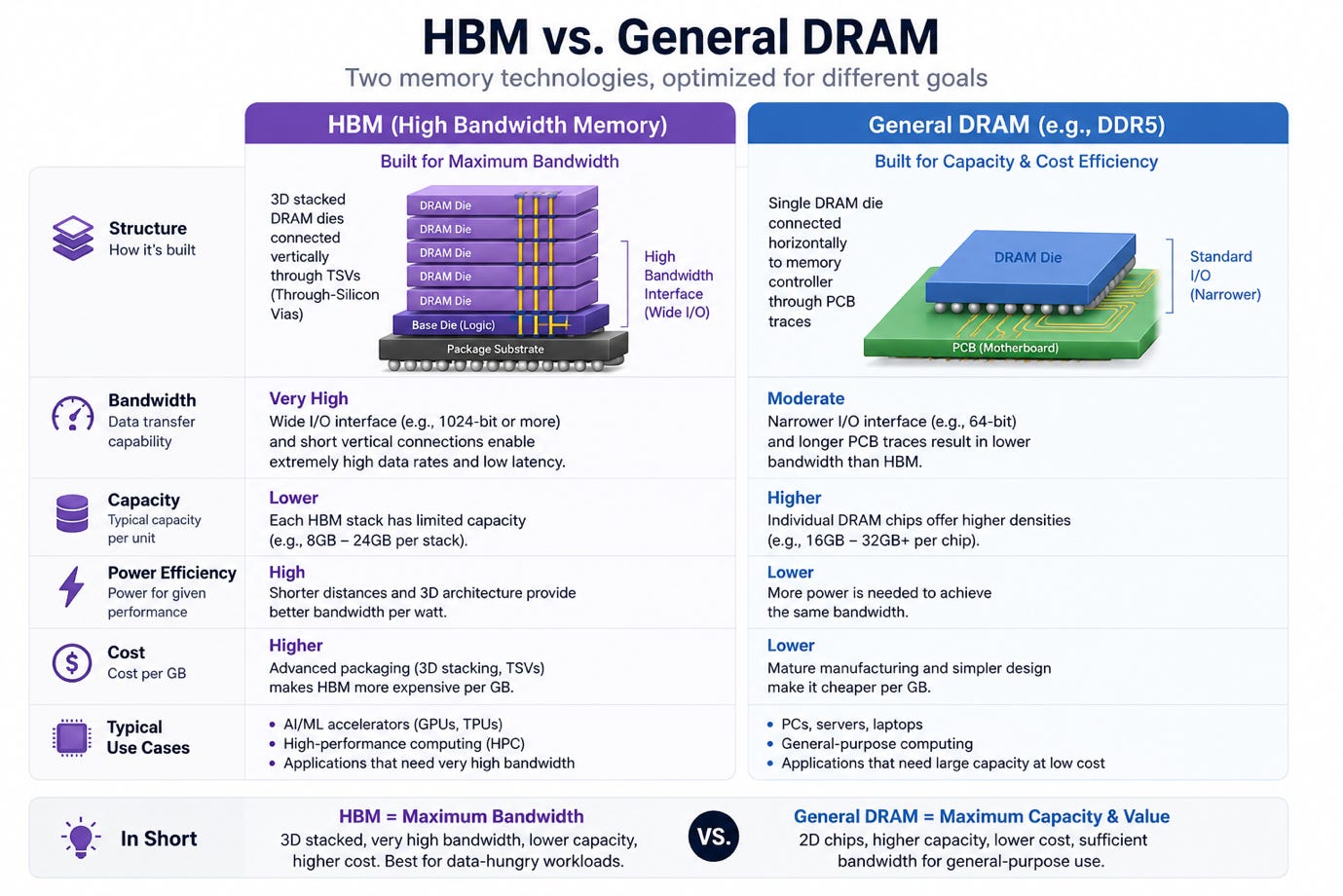

1.2. HBM

High-bandwidth memory (HBM) is a specialized type of DRAM that uses a vertical stacking architecture to achieve extreme data transfer speeds.

Instead of placing memory chips side-by-side, HBM stacks multiple DRAM dies on top of each other.

This stack is then placed on the same package as the AI processor, allowing for a much wider interface and shorter signal paths.

The main use cases for HBM include:

AI training

High-performance computing

Advanced graphics rendering

In AI systems, HBM is the most critical component because it feeds data to the GPU.

Without HBM, the GPU would be starved of data, making it effectively useless for advanced AI. Micron entered the market with HBM3E, which offers approximately 1.2 TB/s of bandwidth per stack and up to 36GB of capacity.

Micron’s HBM3E is particularly competitive because it uses 30% less power than similar products from competitors. But the industry is now moving toward HBM4, which Micron began shipping in volume during Q1 2026.

| Micron Technology Inc.")

HBM4 has a major architectural change, with more than doubling in bandwidth to 2.8 TB/s, and max capacity to 64 GB.

AI desperately needs HBM4 because the size of model parameters is growing faster than memory technology can keep up.

OpenAI’s and Anthropic’s trillion-parameter AI models are hitting a physical limit with the older 1024-bit interfaces. By doubling the interface width to 2048-bit, HBM4 allows for massive throughput without needing to increase the electricity voltage.

This helps manage the thermal wall, which is the heat trapped inside the stack that can damage the chips. Micron’s HBM4 is designed into the Nvidia Vera Rubin platform.

HBM revenues are reported within the overall DRAM segment, so we don’t know exactly, but it is likely a large share and the majority of the growth.

But some independent analysts estimate that last year Micron made about $6-10B in revenues from it, about 16-27% of total group revenues.

1.3. NAND Flash

NAND flash is the permanent, non-volatile storage technology that retains data even when power is turned off.

It is the core technology used in solid-state drives, smartphones, and memory cards.

Unlike DRAM, which is built for speed, NAND is built for high-capacity storage. The main use cases include storing operating systems, applications, and large datasets.

For AI, NAND is used to store the massive amounts of data that are needed to train models.

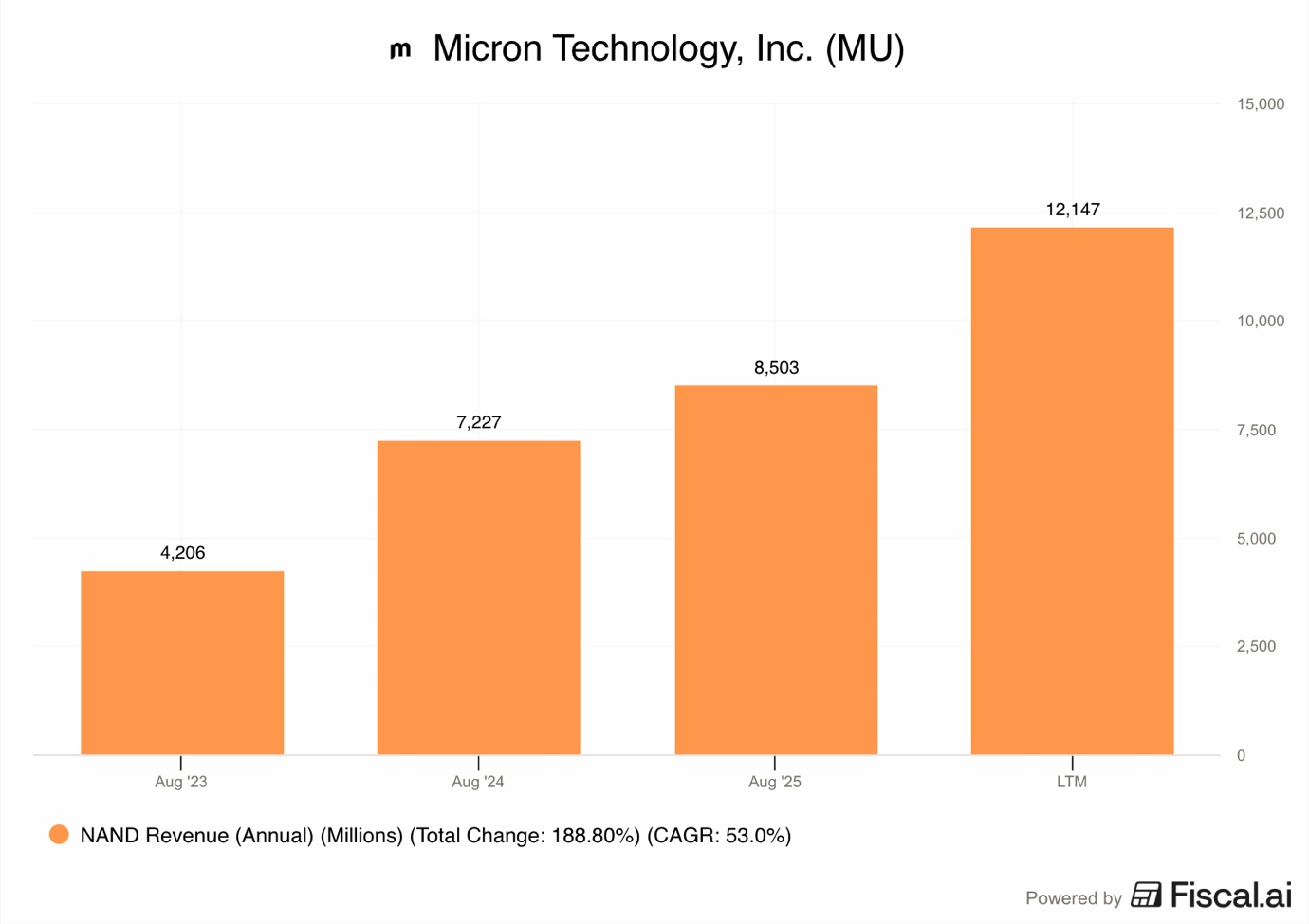

The NAND segment generated $12.1B in revenues in LTM, about 21% of total revenues!

Do you like the chart above?

FiscalAI makes managing investments smarter, faster, and stress-free.

Visualisations

AI-powered insights

Financial data

Earnings transcripts

Portfolio analytics

All in one place. Instead of wasting hours digging through filings and spreadsheets, Fiscal.ai helps you get to the important information in minutes.

Save time, stay organized, and let Fiscal.ai handle the heavy lifting so you can focus on growth.

Join with my link below by Thursday, 14 May, and get a 25% discount.

Similar to DRAM, the NAND segment has also experienced stratospheric AI-driven growth, with revenues growing by an incredible 169% in Q1 2026.

As AI data centers are increasingly moving away from previous-generation hard disk drives and toward all-flash storage to speed up data access, Micron has released several products to support this trend:

245TB 6600 ION SSD: This is the highest-capacity data center drive available, allowing for a massive reduction in the number of server racks needed for storage.

122TB E3.S SSD: This drive offers 67% more server rack density than previous form factors and 37% better energy efficiency than using multiple hard drives.

G9 NAND: Micron’s latest NAND technology provides the high speeds necessary for AI data lakes and vector databases.

One of the growing uses for NAND in AI is in inference.

During the inference process, AI models generate a large amount of temporary data called the KV cache to remember the context of a conversation.

As context windows grow to millions of tokens, this cache can become too large to fit in DRAM. High-speed NAND SSDs are now used to store this cache, which prevents the model from having to recalculate everything from scratch when users ask a question.

This offloading helps improve the efficiency of AI systems and reduces the total cost of ownership for data center operators.

1.4. NOR Memory

NOR memory is another type of non-volatile storage, but it is optimized for high-speed reading of small amounts of code rather than large datasets.

It allows a processor to execute code directly from memory, a feature known as execute-in-place. The main use cases for NOR are storing boot code for computers, firmware for automotive systems, and control software for industrial equipment.

Simply put, while NAND is used for large files, NOR is used for instant-on performance.

When an AI-powered car starts, the safety-critical microcontrollers must boot up in milliseconds to ensure sensors and cameras are active.

Micron’s automotive NOR flash is engineered to meet these demands, providing the durability and speed required for advanced driver assistance systems, sensors, and gateways.

Meanwhile, in the AI data center, NOR memory is used for the fundamental boot-up process of servers and networking switches.

The revenues from this product are reported within the NAND flash segment. While they are not experiencing explosive AI-driven growth, the demand trends still look strong and favorable, thanks to a growing usage in automotive systems.

Furthermore, the market for NOR flash is currently experiencing a supply squeeze.

Because major manufacturers like Micron and Samsung are focusing their factory capacity on more profitable HBM and advanced DRAM, the availability of NOR is tightening. This has led to longer lead times and firmer pricing for NOR products across all end markets, including industrial and medical sectors.

For Micron, this supply-demand imbalance in the broader memory market helps maintain strong profitability even in its smaller product lines.

1.5. Cyclicality

Micron operates in the semiconductor memory industry, which has long been dealing with high capital intensity, rapid technological obsolescence, and a notorious boom-and-bust cycle.

This cycle is driven by the incredibly strong demand elasticity of the memory industry.

When demand is high, prices rise rapidly as users of memory chips race to secure supply. This is exactly what we are seeing now. Memory is an input in the final product, which can’t be shipped without memory.

It takes years and costs $10-20B to build new fabs, so memory makers can’t quickly increase supply, further driving higher prices.

When prices are high, manufacturers look for ways to reduce memory requirements, reducing specs or changing designs.

Let’s not forget that high prices also incentivize suppliers to increase production. So, memory manufacturers all at the same time race to invest in capacity to increase supply. While it takes years for the additional supply to reach the market, it does at the same time.

Supply explodes, and pricing collapses.

The same factors that make increasing supply quickly difficult also make decreasing supply a non-starter. Once built, foundries must operate constantly, as the equipment that they spent billions on degrades while interest costs pile up.

In this industry, raw material input costs are a lower share of total costs than the depreciation of equipment.

Simply put, by shutting down foundries, memory makers will lose more money than by selling each chip at a loss.

Furthermore, Micron’s business is also complicated by the bullwhip effect!

It’s a supply chain phenomenon where small changes in consumer demand for end-products (like smartphones or PCs) result in increasingly larger swings in orders as one moves down the supply chain to the semiconductor manufacturers.

When Walmart runs out of 100 PCs, they make a large order to rebuild their inventory, thinking that strong sales will continue, they order 200 PCs.

When the distributor gets an order for 200 PCs from Walmart, they make an order for 400 PCs with the manufacturer.

The manufacturer receives an order for 400 PCs, so they call their suppliers to order enough chips for 600 PCs.

Chip manufacturers do the same and build capacity to produce chips for 800 PCs.

This growth in orders is seen not only as proof of current demand but as a signal towards future demand.

They do this because each party wants to have enough inventory to meet customer demand, as nobody wants to lose sales due to something “simple” like a lack of inventory.

But then, it takes Walmart much longer than they expected to sell 200 PCs, so they don’t make new orders next time. This creates a cascading series of events, the distributor doesn’t make new orders with the manufacturer, and the manufacturer doesn’t make purchases from the supplier.

The supplier already increased capacity to meet the demand, so they keep manufacturing, as not doing so is worse, supply explodes, and prices collapse. Lower prices increase demand, and the cycle begins again.

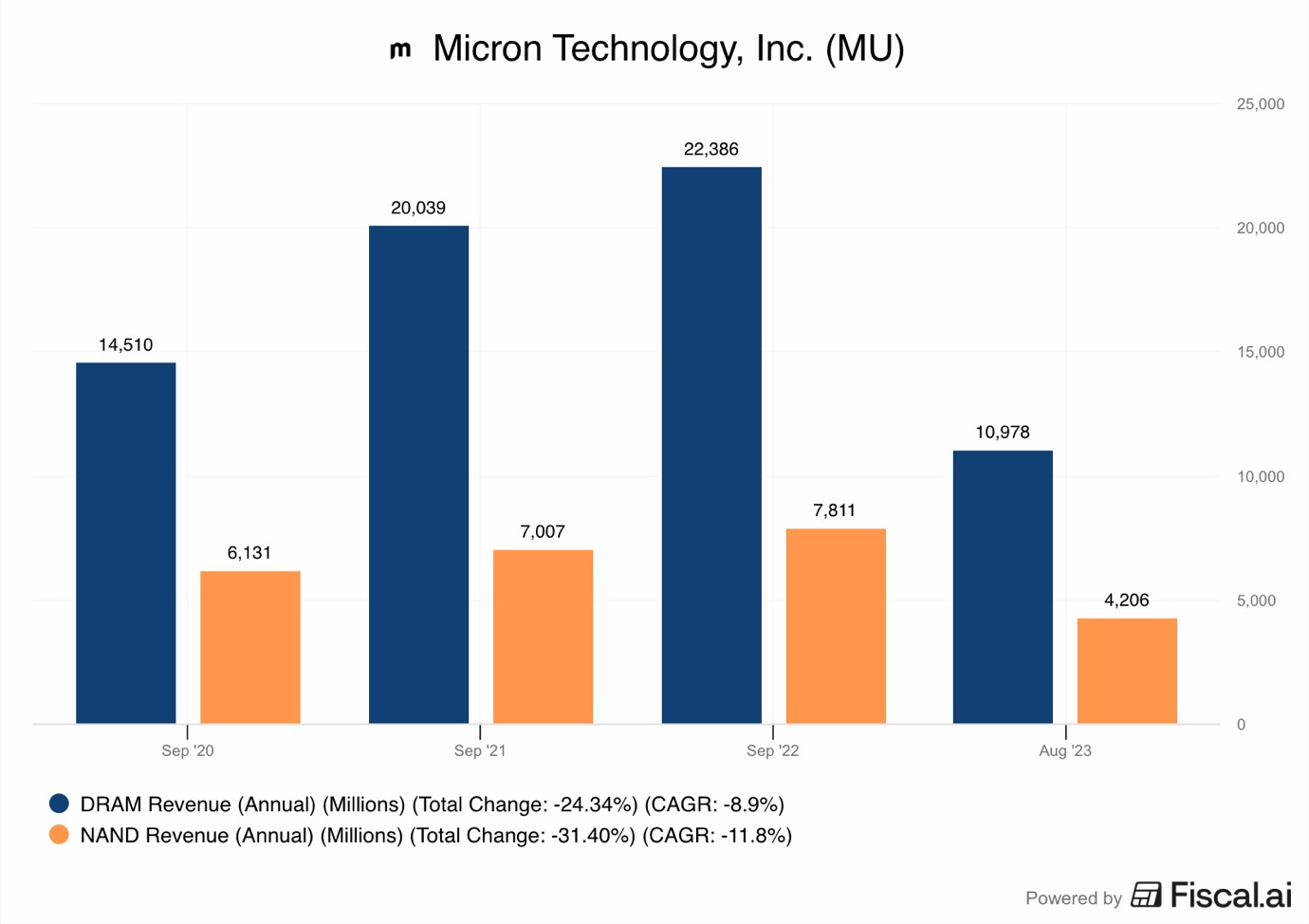

We can see the effects of the cyclicality in the graph below.

From 2020 to 2023, then to 2024:

DRAM revenue grew by 54% and then fell by 51%.

NAND revenue grew by 27% and then fell by 46%.

This happened as demand for smartphones, laptops, and tablets exploded after COVID, but then collapsed.

However, it seems that not only the industry might be exiting the low demand period, but entering a future of much higher structural demand.

Of course, there is a risk that this time is no different and the cycle is just longer and larger, so I will expand on that in the risk section.

2. Manufacturing Strategy

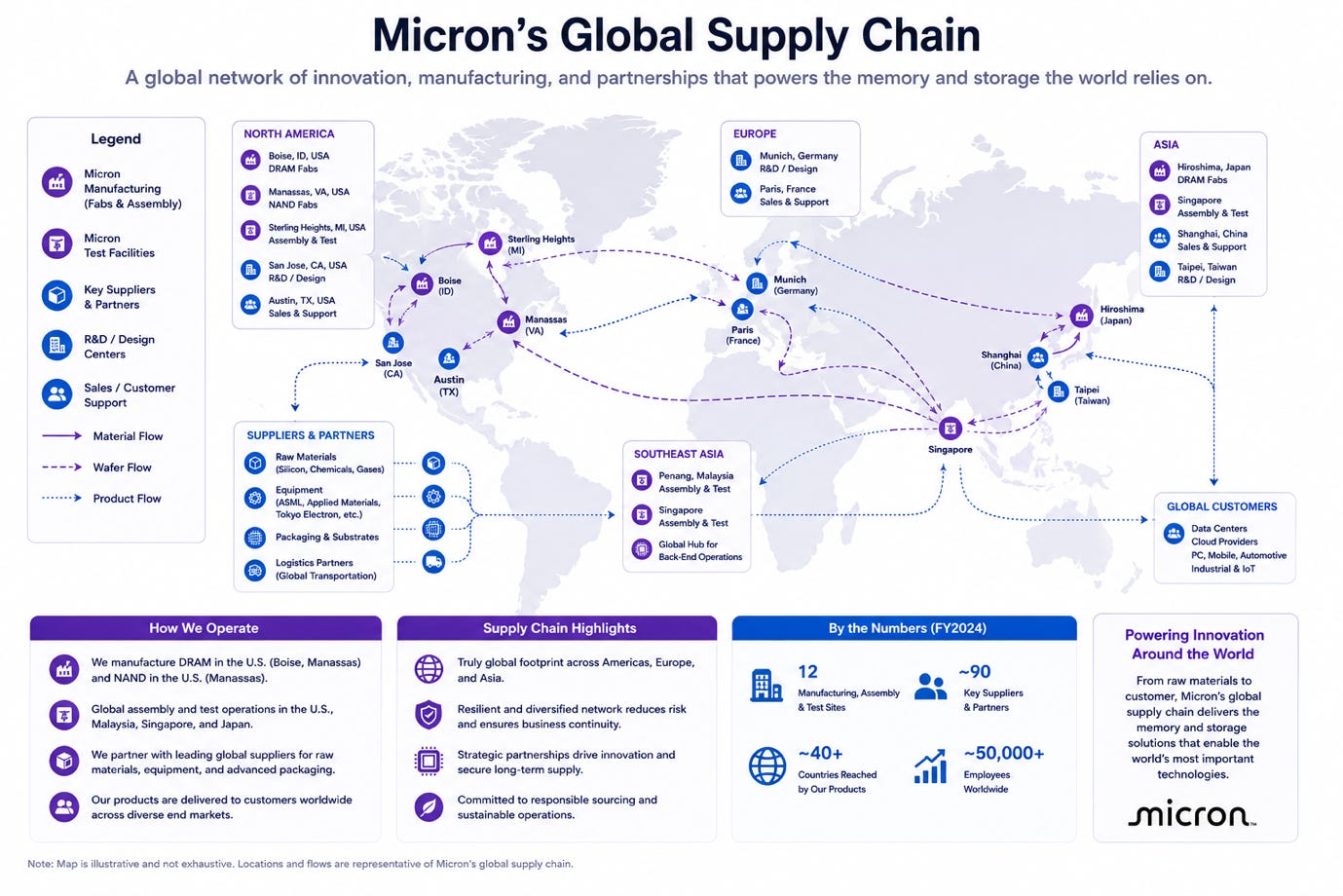

As a global company, Micron operates factories in the United States, Taiwan, Japan, Singapore, and Malaysia.

Micron is currently making the largest investments in its history to expand its manufacturing footprint to meet the massive demand for AI memory.

To understand its manufacturing strategy, we need to look at the:

Foundry Model

Fabless Model

Capex Requirements

2.1. Foundry Model

The foundry model in the semiconductor industry usually refers to a company that builds chips for others.

However, Micron uses an internal foundry model where it builds and operates its own factories to manufacture its memory products.

By owning the entire process, including wafer fabrication, final assembly, and testing, Micron can reduce costs per chip, better manage production ramp up/downs, and ensure that its products meet quality standards.

Micron is currently building several mega-fabs to increase its capacity for advanced DRAM and NAND.

These projects are massive in scale and require tens of billions of dollars in capex.

In the picture above, you can see the Clay, New York project in the US, where Micron has committed to invest $100B over the next 20 years!

It will consist of 4 advanced wafer fabs for DRAM production.

Furthermore, Micron has committed to spending $15B on its DRAM foundry in Boise, Idaho.

The New York and Idaho projects are supported by $6.1B in direct funding from the CHIPS Act.

Management has stated that these government incentives are necessary to make domestic manufacturing competitive with overseas locations. The Idaho plant is expected to begin production in mid-2027, while the first fab in New York is slated to start wafer production in the second half of 2028.

These long timelines highlight why the company must invest so far in advance to meet future demand.

On the other side of the world, Micron is also investing in Singapore.

$24B to build a new advanced wafer fab for NAND and AI memory, and $7B for a packaging facility dedicated to HBM production.

These should be completed by 2028.

2.2. Fabless Model

A fabless model is one where a company designs its chips but outsources the actual manufacturing to a third-party foundry like TSMC or Samsung.

While Micron is primarily an integrated manufacturer, it does use external foundries for certain parts of its products.

This is most common for logic chips like SSD controllers and application-specific integrated circuits (ASICs).

Logic manufacturing is very different from memory manufacturing. While memory fabs are designed for high-volume production of repetitive patterns, logic fabs are designed for complex routing and multiple layers of metal interconnects.

By using external foundries for controllers, Micron can access the most advanced logic nodes, such as 5nm or 3nm, without having to build those types of factories itself.

This hybrid approach allows Micron to focus its capital on its core strength, memory fabrication, while still delivering high-performance storage solutions that require advanced logic to manage the data.

The reliance on external foundries like TSMC does create some risks. Currently, the most advanced logic processes are at full capacity due to the surge in AI demand. This means that Micron must compete with companies like NVIDIA and Apple for factory space.

To mitigate this risk, there is a trend in the industry toward diversifying foundry partners, and companies are exploring alternatives like Samsung Foundry as a backup to TSMC.

2.3. Capex Requirements

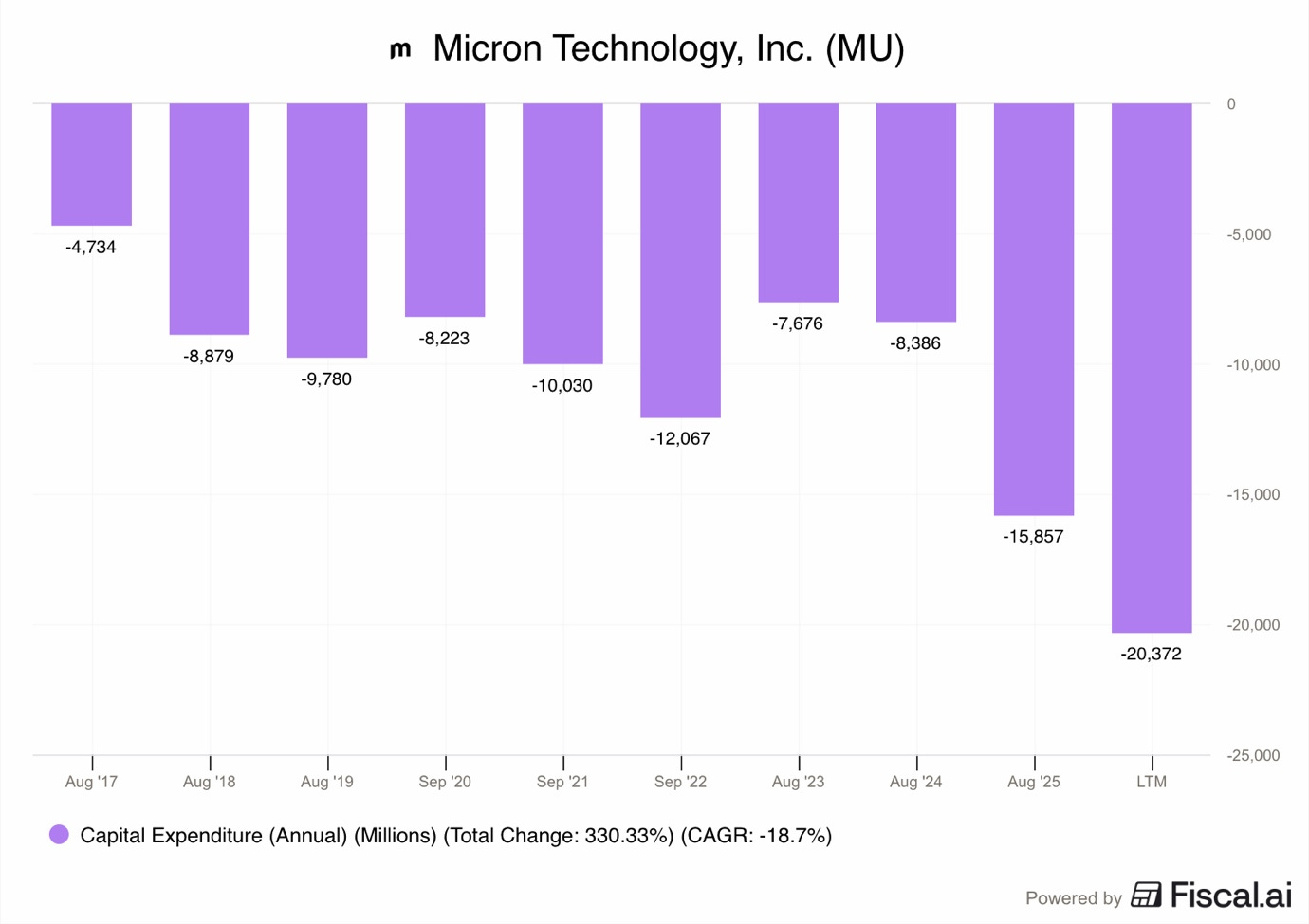

In Micron’s industry, capex is the largest expense because the equipment used to make chips is incredibly expensive.

For example, ASML’s EUV machines, which Micron is using for DRAM, cost $300M each.

As you can see in the chart above, Micron regularly spends about $8-12B on capex each year, spending $78.9B on capex between 2017 and 2025!

Furthermore, Micron has significantly increased its capex guidance to support the AI buildout.

For fiscal year 2026, the company raised its guidance to at least $25B, which is a massive increase from the $15.9B spent in 2025.

The company also forecasted that capex for fiscal year 2027 will increase by another $10B on top of the 2026 levels, reaching about $35B during the New York and Idaho peak construction year.

The market reaction to this high spending has been mixed. When the $25B capex for 2026 was announced, Micron’s stock price fell by about 6% in after-hours trading.

Investors were concerned that excessive spending could lead to oversupply in the future, which has historically caused price crashes in the memory market.

However, management says that they have no choice but to build. Without expanding capacity, Micron cannot increase its order volume to gain market share in the HBM market, where it currently trails its rival SK Hynix.

The 2026-2027 spending is essentially a bet on the long-term growth of AI infrastructure.

3. Customers

Micron’s customer base has moved from a broad group of PC and smartphone makers to a concentrated group of high-value customers.

Because memory supply is so tight, the nature of customer relationships has changed. Instead of buying chips on the open market, large customers are now signing strategic customer agreements that include multi-year commitments for volume and pricing.

These customers are divided into three main categories:

Cloud Hyperscalers

Device manufacturers

Automotive suppliers

The most important customers today are the cloud hyperscalers. These companies operate the massive data centers where AI models are trained and run.

Amazon, Microsoft, Google, Meta, and Oracle are the fastest-growing parts of Micron’s business.

They buy HBM for their AI accelerators, high-capacity memory for their servers, and enterprise SSDs for their storage needs.

Additionally, AI hardware leaders, Nvidia and AMD, are key customers that integrate Micron’s HBM directly into their GPUs.

Micron’s HBM4 is specifically designed for the NVIDIA Vera Rubin platform.

Let’s also not forget that Apple, Samsung, and Xiaomi use Micron’s low-power DRAM and storage for their smartphones.

AI features in phones like the Samsung Galaxy S25 are driving these customers to buy more memory per device, and I will expand on this in the opportunities section of this report.

Meanwhile, companies such as Dell, HP, and Lenovo use Micron products for their laptops and desktops.

Micron’s first-ever 5-year strategic customer agreement was announced in March 2026.

Micron did not publicly disclose the customer name, but industry experts strongly suggest the counterparty is likely a large hyperscaler.

This deal is a sign of how desperate big tech is to secure a stable supply of memory. Unlike typical one-year contracts, these longer deals provide Micron with better visibility into future revenue and help it plan its massive capex projects with more confidence.

4. Risks

As I already mentioned in the cyclicality section of the business model, the memory industry is known for its cycle of boom and bust.

While Micron is currently seeing record profits, it faces several major risks that could impact its long-term stability.

These risks include intense competition from global rivals, difficult geopolitical situations in the Middle East and Asia, the threat of future overcapacity, and the possibility that an AI bubble is forming.

Let’s expand on these risks.

4.1. Competition

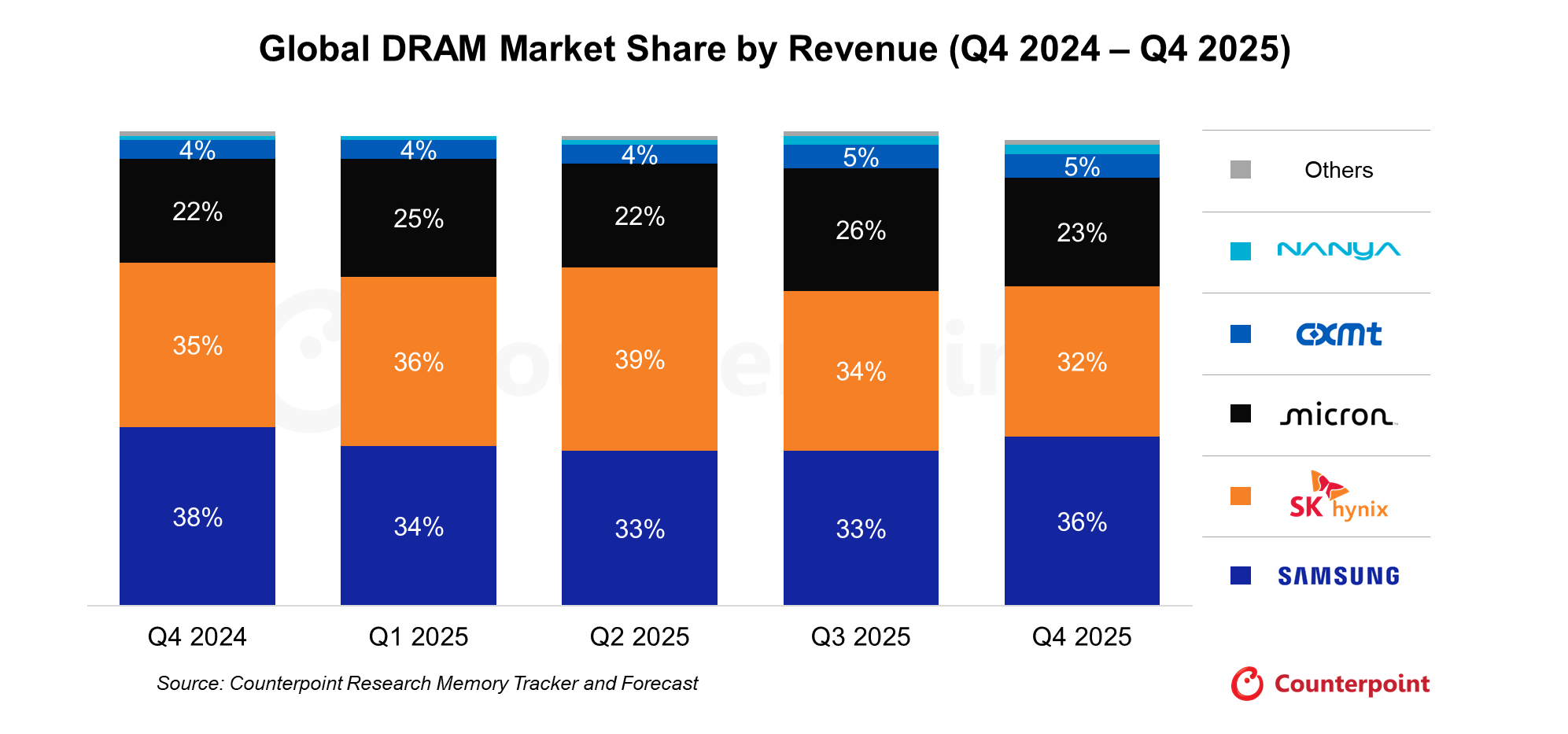

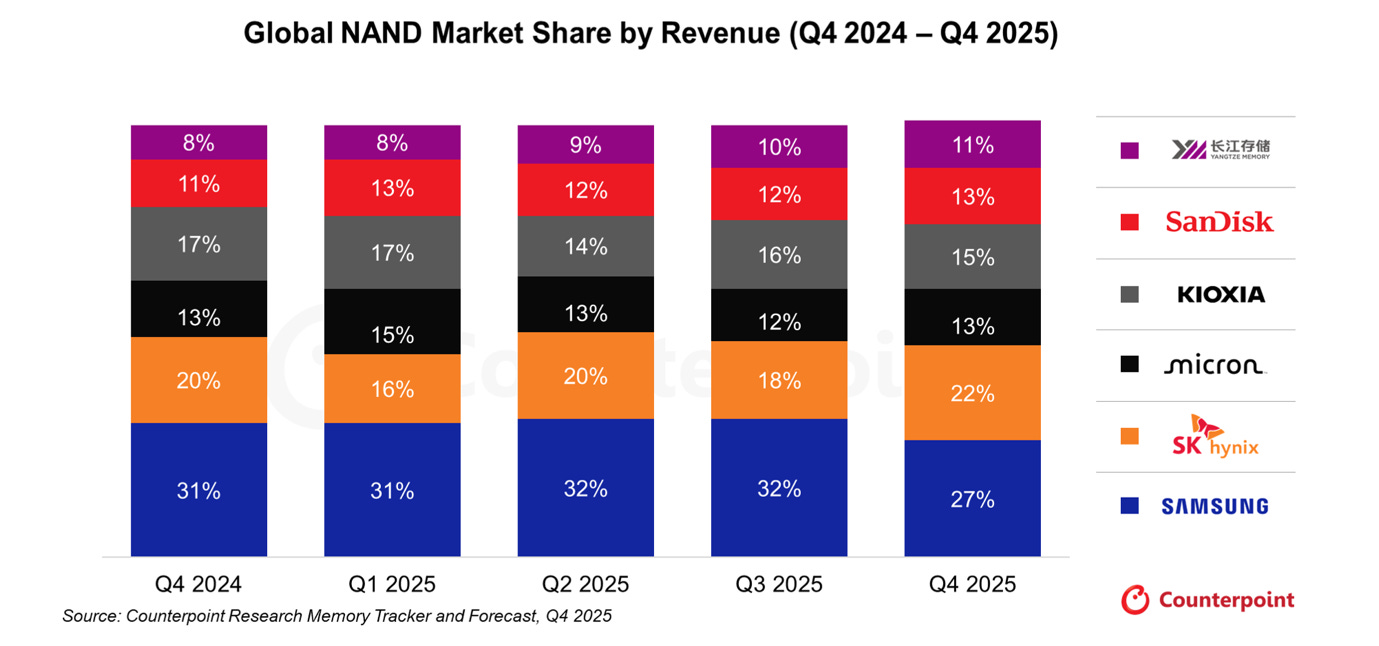

Micron operates in a market that is highly concentrated, as 3 companies control between 90% and 95% of the global DRAM production capacity!

Samsung is the leader with 36% market share.

SK Hynix is second with 32%.

Micron has 23%.

CXMT, the Chinese challenger, has 5%.

SK Hynix currently holds the leading position in HBM and is the main supplier for Nvidia’s flagship GPUs.

Samsung is the largest overall memory maker and is investing heavily to gain more share in the HBM market.

Micron currently sits in third place for HBM market share, but it is working to close the gap.

Micron has been gaining qualifications for its products, but its rivals are moving faster.

A major risk is that Samsung or SK Hynix could accelerate their capacity faster than Micron, which would reduce Micron’s pricing power.

Furthermore, the industry is moving toward HBM4.

SK Hynix and Samsung already hold the majority of the initial supply share for Nvidia’s Vera Rubin platform. Micron had to resubmit its qualification for this platform in Q2 2026.

If the company fails to win a large spot on these next-generation AI platforms, it could miss out on the most profitable part of the market.

Technology transitions also bring yield risks. Each new generation of HBM requires more complex bonding and stacking. If Micron has trouble producing these chips without defects, its rivals will take its market share.

Meanwhile, in the NAND market, the competition is broader, but still dominated by a few large players.

Samsung is first with 27% market share.

SK Hynix is second with 22%.

Kioxia is third with 15%.

Micron and Sandisk both have 13%.

YMTC is 6th with 11%.

Samsung, Micron, and SK Hynix have underinvested in this technology to pursue growth in the more profitable DRAM segment.

They are losing market share to Sandisk, Kioxia, and YMTC.

Sandisk and Kioxia have a partnership where they share manufacturing capacity, and both are investing to increase NAND capacity.

So, it is likely that Micron will lose more market share in 2026 and 2027, at least until its NAND plants in Singapore are upgraded in 2028.

4.2. Geopolitics

Geopolitical risks have become much more severe in 2026.

Micron’s supply chain is global, with manufacturing and packaging facilities in the US, China, Japan, Taiwan, Singapore, and Malaysia.

Any conflict in these regions could significantly increase costs and delay production.

Taiwan, especially, is a major concern.

Most advanced chip packaging happens in Taiwan.

If there is military tension in the Taiwan Strait, the entire global supply of AI chips could be cut off. The US government has pushed for a reduction in this reliance. In January 2026, the US and Taiwan signed a trade agreement that includes $250B in direct investments to build chip production in the US.

However, following military strikes by the US and Israel on Iran, the Iran War began, and with it, a new crisis in the Strait of Hormuz.

This critical waterway was effectively closed. This has caused 3 big problems for chip makers.

First, it disrupted the supply of helium.

Qatar provides about one-third of the world’s helium. Helium is necessary for cooling EUV lithography machines, which are used to make the most advanced chips. South Korea and Taiwan are very dependent on this supply, with South Korea getting nearly 65% of its helium from Qatar.

Second, the closure has disrupted shipping routes for high-precision tools.

Specialized equipment moving from Europe to fabs in Asia is being delayed.

Third, Asian countries that depend on Middle East oil and LNG for energy are forced to conserve fuel and energy and are seeing large price spikes.

Nevertheless, the semiconductor industry is doing a lot to manage this crisis. These companies are loaded with cash thanks to strong profits and enjoy incredible government support due to their importance for the economies of Japan, South Korea, Taiwan, and Malaysia. They have ample avenues to manage the crisis.

However, the effectiveness of these mitigating actions decreases the longer the war goes on.

If Micron is forced to take longer-term measures, it could cost billions and delay production.

Lastly, investors can’t forget about Trump’s tariffs.

The Trump administration has played with the idea of chip tariffs. While some semiconductors were excluded, items like memory modules and SSDs could face some duties.

Micron has stated it will apply a tariff-related surcharge to US customers to cover these costs. This makes Micron products more expensive and could hurt its competitiveness if rivals find ways to avoid the tariffs.

Furthermore, Trump has been extremely unpredictable, with no policy consistency. A new tariff could be announced any day, which could create disruptions or cause billions in additional costs for Micron.

4.3. Overcapacity

The memory industry has a history of building too many factories when prices are high.

This leads to a supply glut, where there are more chips than people want to buy.

When this happens, prices crash, and companies lose money.

Currently, all 3 major memory makers are massively increasing their capex.

Micron expects capex for 2026 to be over $25B.

Samsung and SK Hynix are also building new fabs that will start producing chips in 2027 and 2028.

While the current market has a shortage, this could change.

A unique factor in this cycle is that HBM production consumes much more wafer capacity than standard DRAM. It takes about 3 times as much wafer space to make one bit of HBM compared to one bit of regular DRAM.

This has helped prevent a supply glut so far.

By 2026, HBM is expected to use 25% of all DRAM wafer production. However, if technology improves and makes HBM production more efficient, a large amount of capacity could suddenly become available for standard DRAM, which would crash prices.

If AI demand slows down just as these new factories open, the industry could face another downturn like the one in 2023.

4.4. AI Bubble

There is a risk that the current investment in AI is creating a bubble.

Since 2023, demand for AI hardware has been incredibly high. However, some investors worry that companies are spending too much money before they have found ways to make a profit from AI software.

One specific concern is AI software efficiency, as we saw with Deep Seek.

If new software techniques allow AI models to run on much less memory, the demand for Micron’s most expensive chips could drop.

However, some say that Jevons’ Paradox will come into effect.

It says that as a technology becomes more efficient, the cost of using it falls, which can lead to more total demand.

The concentration of customers also adds risk.

Data centers are expected to use 70% of all DRAM production by the end of 2026. If a few big companies like Microsoft or Meta decide to slow down their hardware buying, Micron will have a hard time finding other customers to take that capacity.

5. Opportunities

Micron has several massive growth opportunities thanks to the rise of AI.

While the company still faces risks from the cyclical nature of the memory market, the current demand environment is unlike anything seen in the past 50 years.

Thus, I see clear opportunities for Micron in:

Automotive

AI Data Centers

AI on Devices

Let me explain.

5.1. Automotive

The automotive market is not an explosive one, yet one of the most stable and attractive opportunities for Micron.

New EVs and even legacy combustion cars are increasingly becoming powerful computers on wheels, requiring a lot of memory for both safety systems and entertainment.

Micron provides a wide range of specialised products that can survive extreme temperatures and vibrations generated by driving.

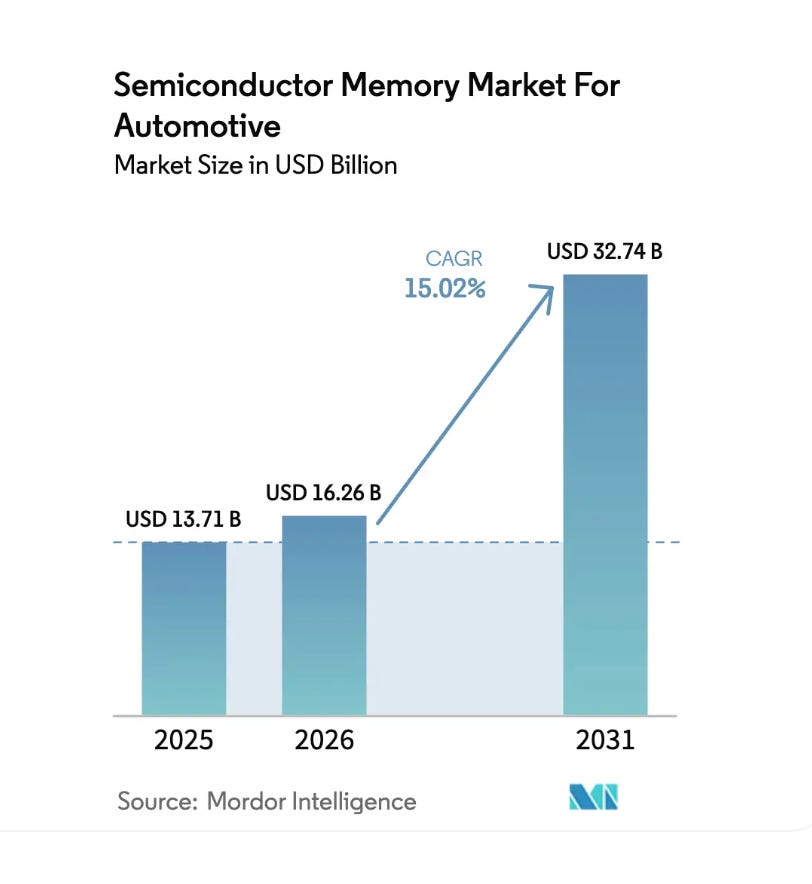

Analysts at Mordor Intelligence forecast the automotive memory market to grow with a 15% CAGR to reach $32.74B in 2031!

There are 4 main drivers of this growth:

Advanced driver-assistance systems

Infotainment

Digital cockpits

Full self-driving

")

Advanced driver-assistance systems use AI to process data from cameras and sensors to help the car stay in its lane and avoid crashes.

This system requires fast DRAM and high-reliability NOR flash to work instantly.

Furthermore, modern cars feature multiple high-resolution displays and AI-based voice assistants. This requires high-speed storage and memory to provide a smooth user experience.

Additionally, Elon Musk has been promising robotaxis for over a decade, but he has vastly underestimated how much on-vehicle memory is required to reach Level 5 self-driving.

Level 5 self-driving cars require massive amounts of memory to store maps and process real-time surroundings. Micron’s memory products are designed to meet the strict functional safety standards needed for these systems.

Lastly, as cars move toward electrification and higher levels of autonomy, the value of the memory in each vehicle is expected to rise. This helps Micron balance its business because automotive contracts are typically longer and less volatile than the consumer PC or smartphone markets.

Compared to regular internal combustion vehicles with basic infotainment and driver assist features, modern EVs need 5-20x more DRAM memory and 10x more NAND storage!

There is a clear opportunity for Micron to steadily grow automotive revenues for a decade+ as the industry transitions.

5.2. AI Data Centers

The buildout of AI infrastructure in data centers is the single largest opportunity in the history of the memory industry.

For the first time in 2026, data center demand is expected to account for more than 50% of the entire memory market. This is because AI workloads are incredibly memory-intensive compared to traditional web search or social media tasks.

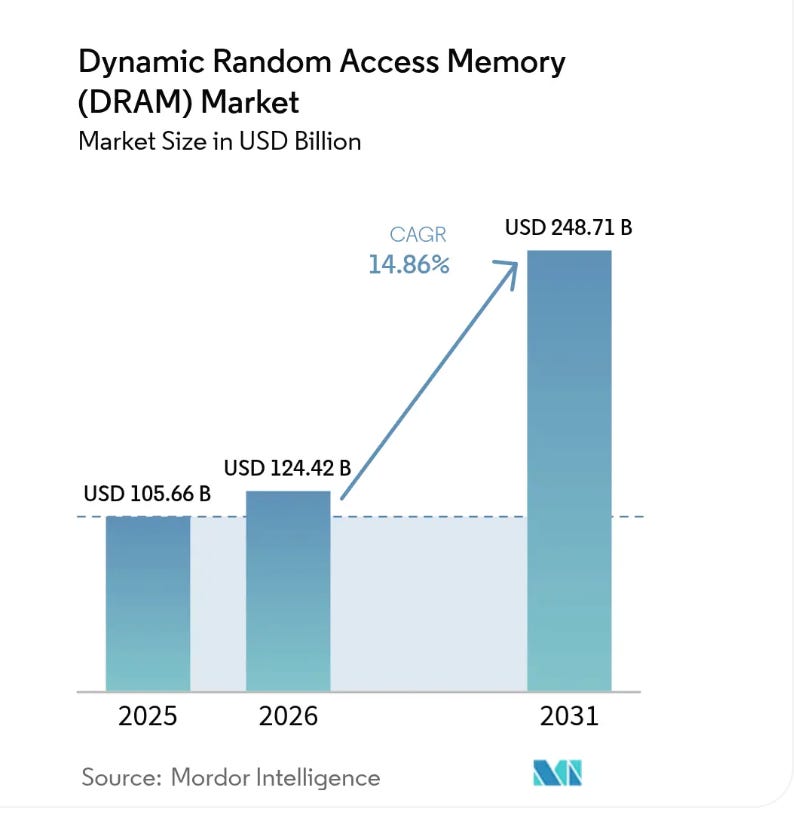

Experts at Mordor Intelligence forecast the DRAM market to grow with a 14.86% CAGR to reach $248.7B in 2031!

AI needs more memory for several reasons, such as:

Growth of LLMs

Memory wall

Long context AI

Agentic AI

Training AI models such as Geminie or Claude requires thousands of GPUs working together.

Each GPU needs its own HBM stack to store parts of the model and the data being processed.

This means that millions more HBM memory chips are needed to satisfy the needs of Nvidia and AMD chips. It is important to take into account that as GPUs get faster, they need more memory bandwidth to keep the processor busy.

If memory speed does not grow as fast as the GPU, the entire system slows down and becomes useless.

When companies spend tens of billions on GPUs, they want to get as much value out of them as possible. The development and manufacturing of memory systems have lagged GPU production, so now we are seeing manufacturers like Micron investing aggressively to catch up with the demand.

But AI development is not standing still while we wait, as models are now capable of remembering millions of words of context. To do this, they must store a massive KV cache in the DRAM or SSD, which increases the total memory capacity needed per user.

Furthermore, Agentic AI applications are growing rapidly, creating new types of AI that can perform tasks on their own. This requires more memory and CPU involvement, which supports demand for general-purpose DRAM in addition to HBM.

Data centers are also shifting toward all-flash storage. Micron’s high-capacity NAND flash products, such as SSDs,

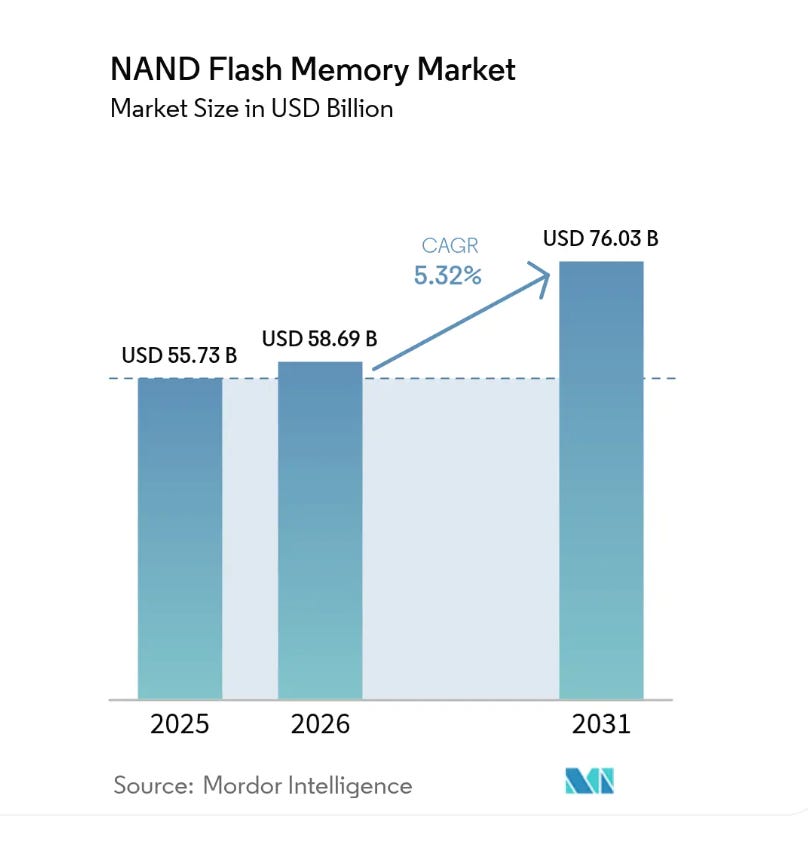

Experts at Mordor Intelligence forecast the NAND flash memory market to grow with a 5.32% CAGR to reach $76B in 2031!

Micron’s 245TB chip is a significant upgrade over the older memory chips, saving a massive amount of electricity and space.

One 245TB SSD can do the work of dozens of traditional hard drives while using 82% fewer server racks. This energy efficiency is a major selling point for hyperscalers that are struggling to find enough power for their growing data centers.

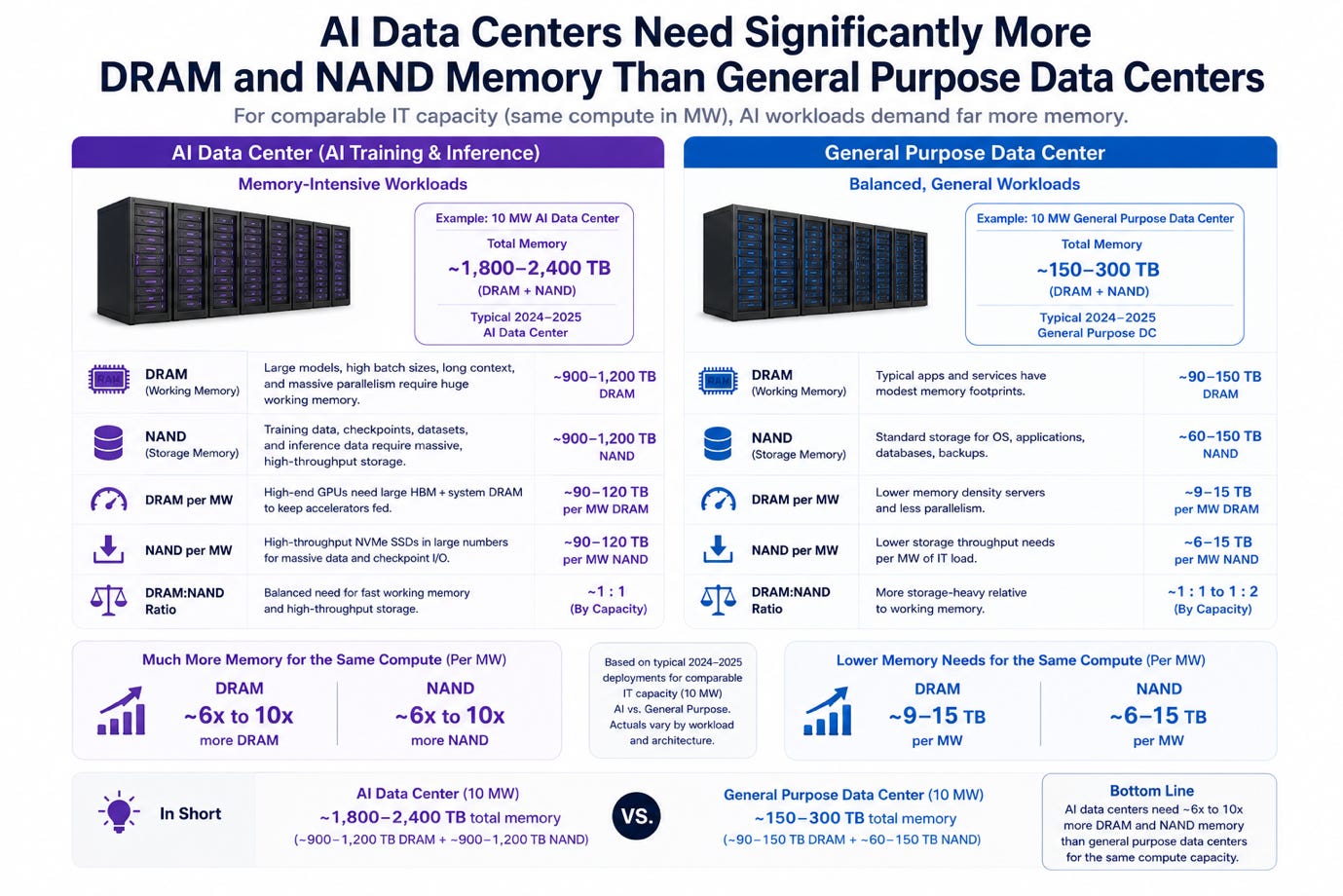

Overall, a comparable MW capacity AI data center needs 6-10x more DRAM and NAND memory!

Considering the current AI data center development trends, this bodes very well for Micron’s future demand.

5.3. AI on Devices

The next wave of growth will come from AI running directly on personal devices like laptops and smartphones.

This is often called Edge AI.

Running AI on the device instead of the cloud is better for privacy, faster, and does not require an internet connection.

However, it requires a significant upgrade to the memory inside the device.

To run a high-quality LLM locally, a device needs much more RAM than is common today.

For instance, an AI model with 1-7B parameters requires about 8-16GB of RAM.

I have an iPhone 16 Pro. When I go to Photos and search for steak, I see all my photos with a steak. This is what we are talking about.

A more advanced model with 13-32B parameters requires about 32GB.

While a model with 70B+ parameters requires above 64GB RAM.

This is significantly above what most laptops and smartphones have today.

Most people today have laptops with 8GB or 16GB of RAM, so to use advanced AI features, they will need to upgrade to 32GB or 64GB.

This doubles or triples the amount of memory Micron sells to PC makers for every laptop.

Micron’s LPCAMM2 is a new type of memory module that is specifically designed for this. It uses LPDDR5X chips to provide 34% faster AI performance and 40% better energy efficiency than the older modules used in most laptops.

In the smartphone market, the same trend is happening.

Flagship phones are now shipping with 12GB to 24GB of DRAM to handle generative AI tasks.

Micron’s LPDDR5X is built for these phones, providing the high speeds needed for AI while using the least amount of battery power. This shift toward AI on devices is expected to drive a massive replacement cycle as users buy new hardware to access the latest AI tools.

6. Financials

I keep repeating myself over and over, Micron’s performance has been very cyclical.

The company’s results can swing from massive losses to record profits in just a few years.

6.1. Revenues

Micron’s revenue has been a roller coaster over the last 5 years.

In 2021 and 2022, the company did well as people bought more electronics during the pandemic, growing revenues by 29% and 11%, reaching $30.8B.

In 2023, revenue fell sharply by 49% to $15.5B because device manufacturers had too many chips in inventory and stopped ordering.

Then came a resurgence, which, as we already discussed, was driven by AI.

High-end servers need much more memory than traditional servers, and Micron was able to sell its new products at high prices.

By fiscal Q2 2026, LTM revenue reached $58.1B, giving us a revenue CAGR of 20% from 2020.

6.2. Margins

From 2020 to 2022, Micron’s margins were decent and improving.

However, margins were very poor in 2023 because it had to sell chips for less than they cost to make.

Gross margin fell to terrible -9% in 2023.

Essentially, it cost Micron $1.09 to manufacture $1 of the end product.

If we include corporate overhead, R&D, taxes, and interest costs, the results were even worse.

Operating margin was -37%, whilst net income margin was -38%.

However, Micron is now seeing a strong recovery.

In fiscal Q2 2026, the gross margin reached a record 74.4%.

This happened because the price of chips went up very quickly due to the shortage. Recently, DRAM contract prices rose by over 60% in just one quarter.

Management expects margins to reach 81% in fiscal Q3 2026.

Meanwhile, operating margin jumped to 67.6% and net income to 58%.

Incredible margins. And the scary thing is that they will get better as the demand and supply imbalance continues.

6.3. Profitability

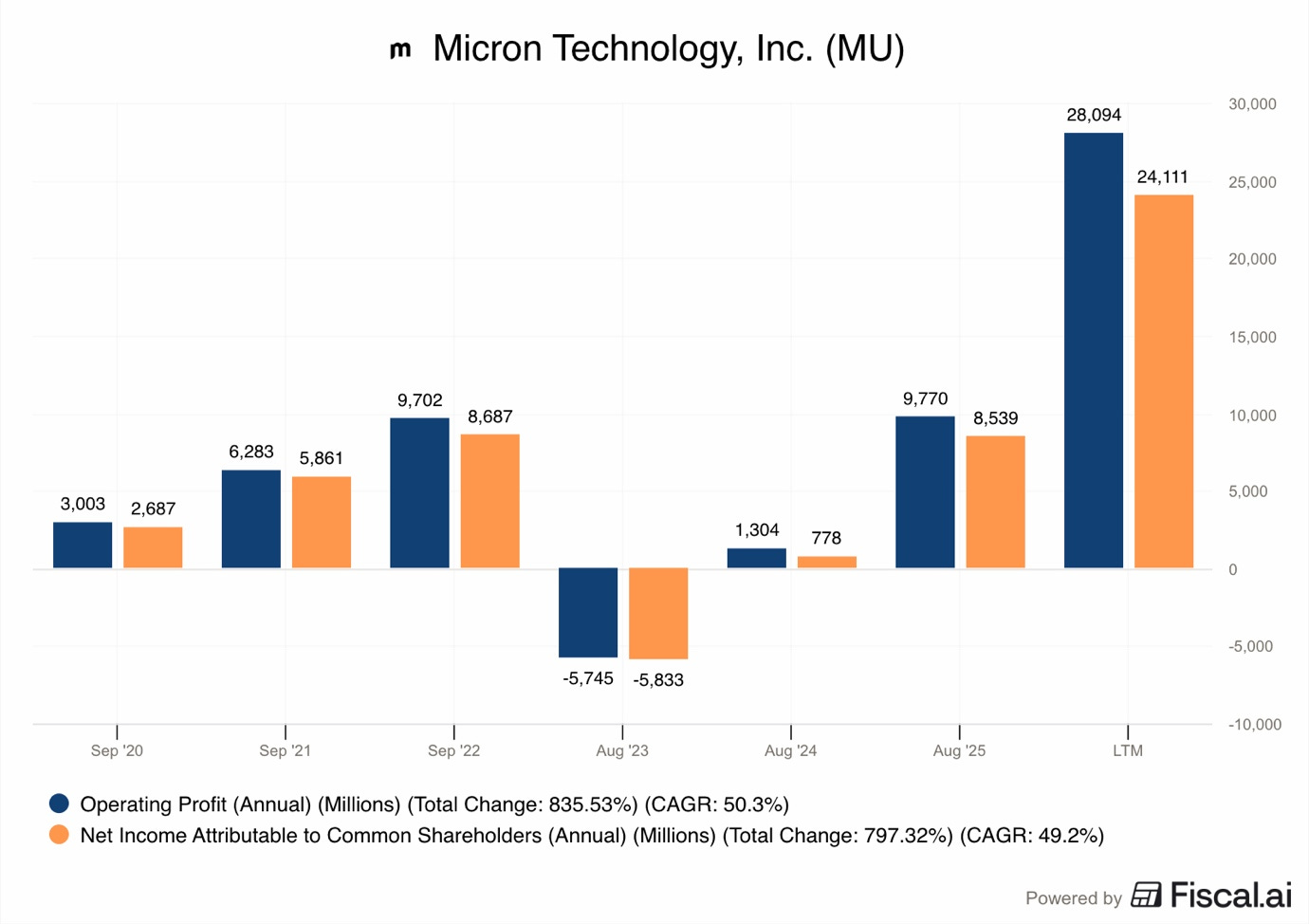

The company lost $5.8B in 2023, but it is now earning record net income.

In the single quarter of fiscal Q2 2026, Micron reported net income of $13.79B.

This is an incredible amount for one quarter and shows how much money memory makers can make when there is a shortage of advanced chips.

In LTM, Micron has earned $28.1B in EBIT and $24.1B in net income.

Simply put, in the last 12 months, Micron has earned more than from 2020 to 2022 combined.

6.4. Cash Flow

In 2023, Micron had a negative FCF of $6.1B

This is because Micron spends a large part of its cash flow on capex to buy new machines and build factories. So 2023 capex was $7.7B, despite the slowdown, as Micron must upgrade its facilities even during slow times, as otherwise they will lose market share to competitors.

Today, thanks to incredible demand, Micron is generating strong cash flow.

In fiscal Q2 2026, OCF was $11.9B, and the company generated $6.9B in FCF.

Over the LTM, Micron made $30.7B in OCF and $10.3B in FCF, despite spending an incredible incredible $20.4B on capex.

Simply put, Micron is able to generate lots of cash, despite being in an aggressive investment period.

6.5. Balance Sheet

Micron has worked to keep its balance sheet healthy so it can survive the times when chip prices fall.

As of fiscal Q2, 2026, the company had $14.6B in cash.

Micron’s total debt has fluctuated over the last few years as it borrowed money to build new fabs.

Total debt was $7.2B in 2021 and grew to $15.3B in 2025.

However, as the company started making more profit in 2026, it began to pay down some of that debt. By the end of fiscal Q2 2026, total debt was back down to around $10.8B.

The balance sheet is stable and gives the company ample room to borrow to fund expansion or buybacks. However, considering the current boom, Micron will likely continue reducing debt.

6.6. Fiscal Q2 2026

The fiscal Q 2026 was a beautiful one for Micron.

Revenue was $23.86B, up 196% from $8B in the same quarter a year ago.

This was driven by explosive demand from all segments:

Cloud Memory (CMBU): Revenue was $7.75B +163%. This unit makes chips for large cloud companies like Google and Microsoft.

Core Data Center (CDBU): 5.69B +211%. This unit handles chips for servers and storage in data centers.

Mobile and Client (MCBU): $7.71B +245%. This unit serves smartphone and PC makers.

Automotive and Embedded (AEBU): $2.71B +162%. This unit makes chips for cars and industrial tools.

This growth significantly increased profitability and cash flow:

Gross profit: $17.8B +499%, reaching a margin of 74%.

Operating profit: $16.1B +810%, a margin of 68%.

Net income: $13.8B +771%, margin of 58%.

OCF: $11.9B +202%, margin of 50%.

FCF: $5.5B vs a loss of $113M, margin of 23%.

Incredible results.

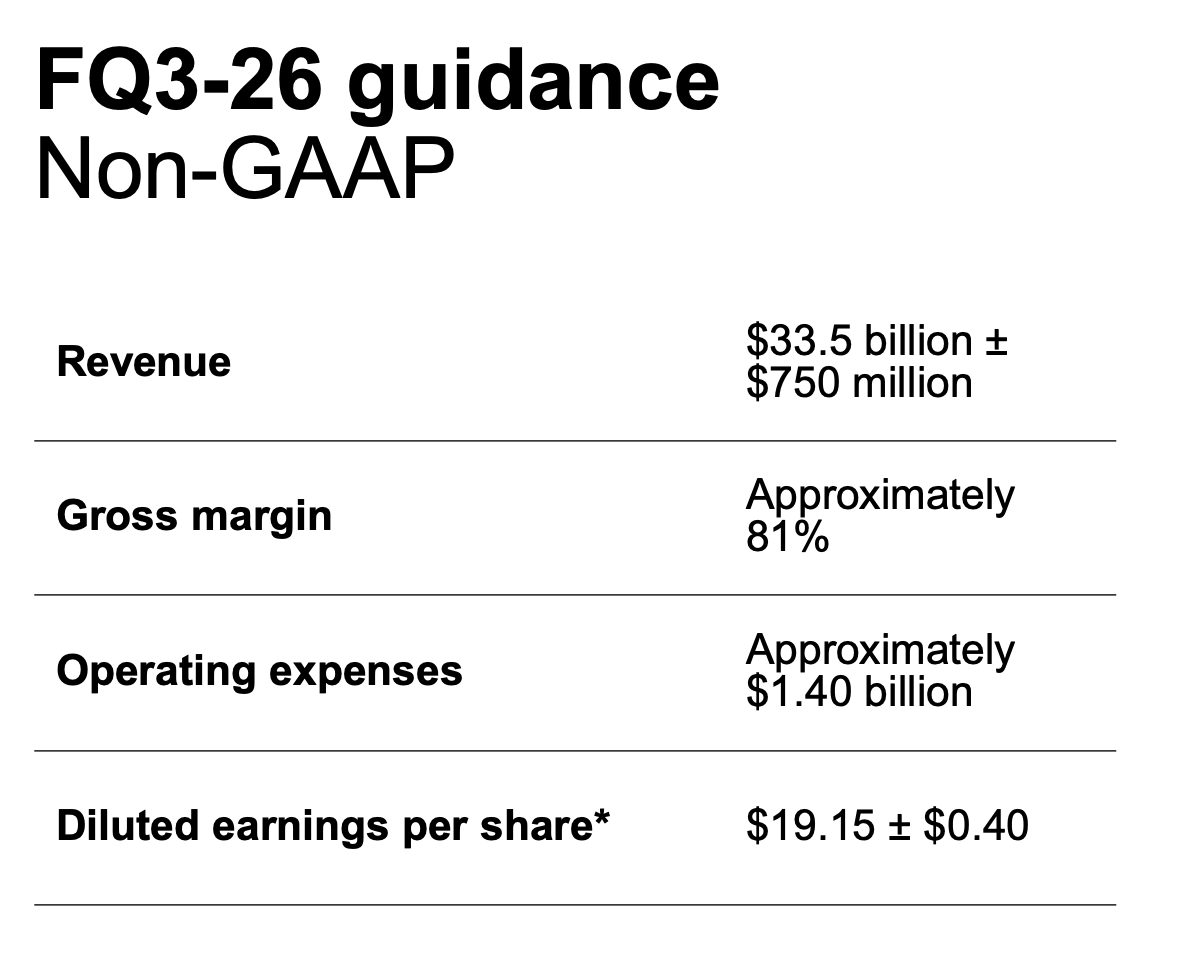

Looking at fiscal Q3 2026 guidance, we see that Micron expects:

Revenue: $33.5B

EPS: $19.15

That would be about 260% revenue growth and over 1,000% EPS growth.

This is Nvidia’s 2024 level growth.

7. Valuation

After rising 179% in the past year, Micron now trades for a $897B market cap!

Even though Micron’s stock price is high, its forward P/E ratio is quite low because its earnings are growing so fast.

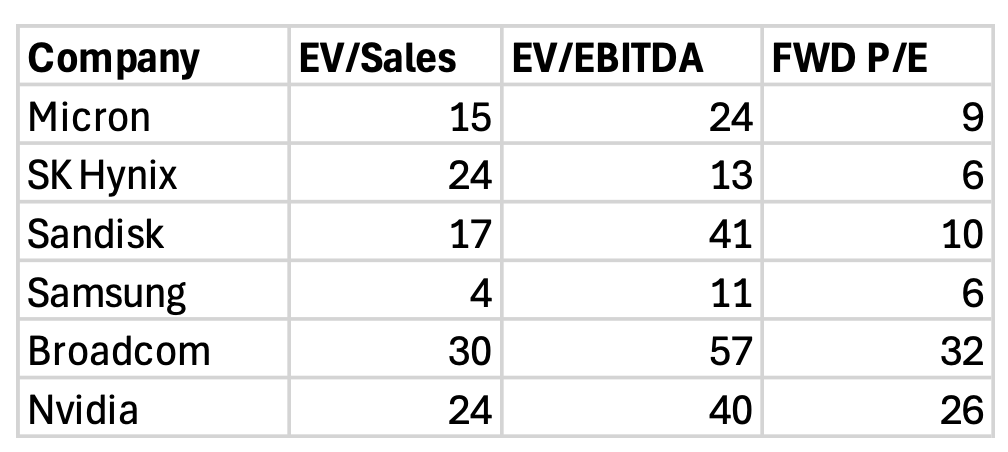

I have placed selected valuation metrics of a few Micron semiconductor industry peers in the table below.

Micron trades for a highly attractive FWD P/E of just 9, as it is expected to grow incredibly quickly.

The low forward P/E for memory companies like Micron, Samsung, and SK Hynix compared to Broadcom and Nvidia shows that investors are worried the current high profits will not last.

This is a cyclical discount.

Investors pay a lower price for these earnings because they believe that there is a high probability that chip prices will eventually fall.

However, recent long-term deals and higher structural demand indicate that this might not be the case, or this cycle is much longer than before.

Analysts expect 2028 revenues to reach $160B, 176% above today.

While EBIT and net income are expected to reach $121B and $90B.

Most importantly, FCF is projected to explode by 606% to $72B as Micron’s capex investments slow down and begin generating strong returns.

Taking this into account, Micron trades for about 9x 2028 earnings and 11x FCF!

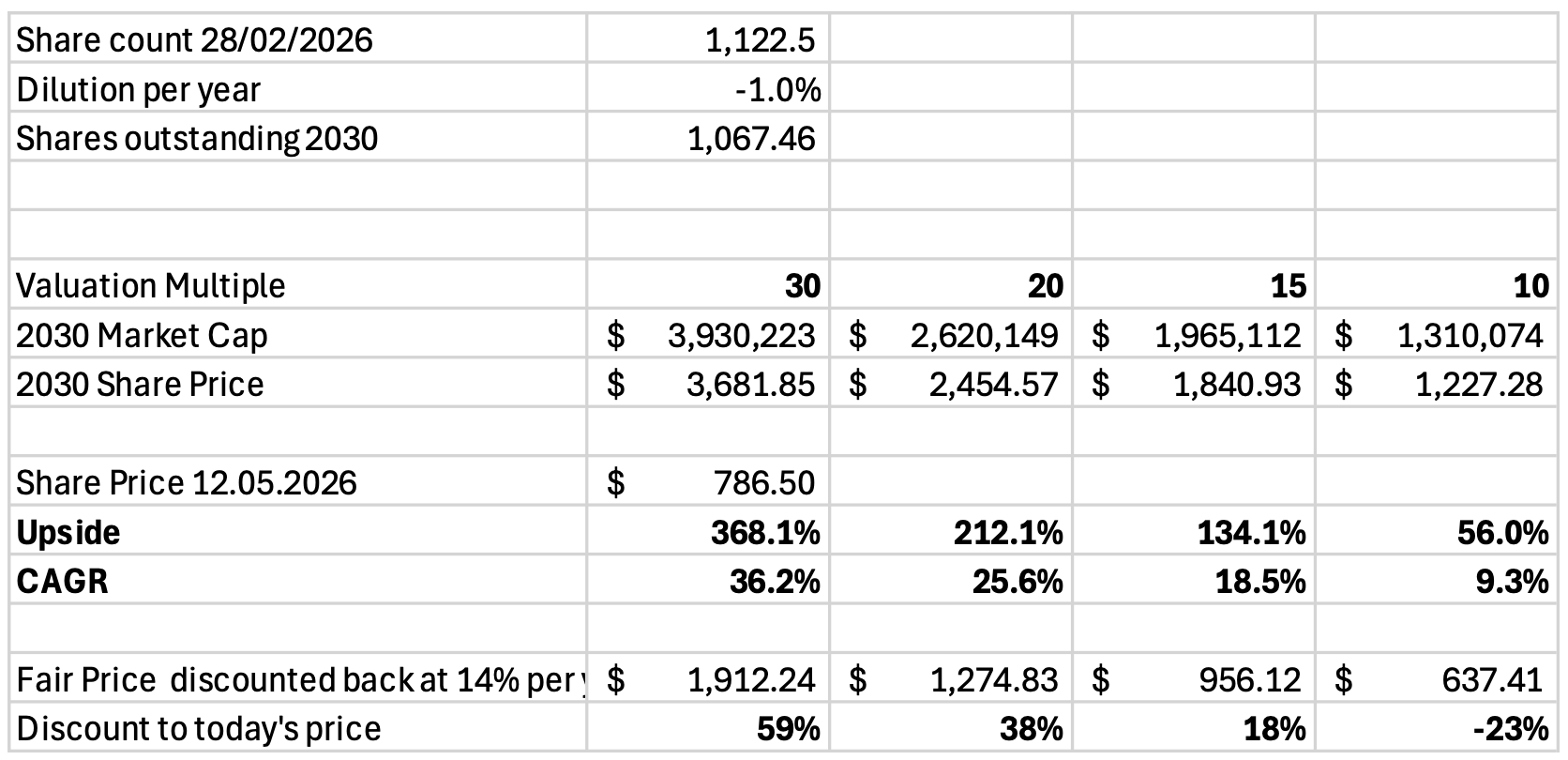

Let’s build a 2030 valuation model to see what could happen in the next 5 years.

8. Valuation Model

Now Micron is experiencing stratospheric revenue growth, but it has to slow down eventually.

So, I model 192% in 2026, 60% in 2027, 25% in 2027 and 10% in 2029 and 2030.

We get 2030 revenues of $264.1B!

Because the demand is so strong, Micron has immense pricing power, resulting in incredible margins.

However, that can’t last forever, so I model it peaking at 80% in 2027 and then falling to 62% in 2030.

Micron will be forced to lower prices to sustain revenue growth and keep market share, resulting in lower margins.

In my opinion, the memory business is still cyclical, so there will be a year when revenue falls by 50%, just as in 2023. Nevertheless, with the way the AI boom is going today, I don’t believe it will happen by 2030, it could be 2032-35.

However, I am not a wizard, so I can’t say that with absolute certainty, as it is incredibly difficult to predict. Not many industry experts predicted the 2023 memory glut, and even fewer predicted this AI boom, and I am not an industry expert.

Such assumptions would result in a 2030 operating income of $163.8B!

Tax and net interest cost of 20%.

We get net income of $131B!

Next, dilution of -1% per year, as Micron buys back some shares with its massive profits.

Exit multiple of 15-20x.

We get a target share price of $1,840-2,454!

That would be an upside of 134-212% by 2030.

Discounting that back at 14% per year, we get a fair value per share of about $956-1,275.

That would imply that at today’s share price, Micron trades at an 18-38% discount to its fair value.

That seems decent upside, considering the current AI boom. However, this valuation assumes that memory trends don’t change. As I mentioned in the risk section, there are some scenarios in which that doesn’t happen.

Conversely, considering all the opportunities for growth in the automotive industry, the requirements for memory for on-device AI, and the massive growth of AI data centers, this model might also end up being conservative.

9. Conclusion

In summary, Micron is positioned at the center of one of the most important growth waves in human history.

By investing heavily in its factories and pushing the boundaries of memory technology, the company has turned itself into a critical provider of AI infrastructure. While the high costs of building new fabs and the risks of the semiconductor cycle remain, the sheer scale of demand from data centers and AI devices indicates that Micron could have entered a period of stable growth.

The company’s record results in 2026 are likely just the beginning of a long-term shift in how memory is used.

There are real long-term opportunities to grow, and the valuation remains affordable, with an FWD P/E of just 9.

As the valuation model showed, with continuous growth, a slight reduction in margins, and buybacks, Micron could deliver 134-212% upside by 2030.

However, the road to 2030 is full of risks.

The closure of the Strait of Hormuz in March 2026 has shown how fragile the supply chain is for helium and high-tech equipment. Competition from Samsung, SK Hynix, and Chinese government-backed companies remains fierce, and Micron must continue to invest billions of dollars in new factories to keep up.

Thank you for reading Global Equity Briefing!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.