Nebius Q1 2026: Upgraded 2030 Valuation Model.

671% ARR Growth, showing incredible execution from Arkady and the Nebius team.

Nebius continues to execute on a level that even the biggest bulls couldn’t foresee.

This was yet another stellar quarter from Arkady and the Nebius team:

Capacity guidance increased from 3GW to 4GW.

New 1.2GW site in Pennsylvania.

AI Cloud revenues up 841% Y/Y.

40% ADJ EBITDA margin target for 2026.

3 major acquisitions to strengthen the AI Cloud offering.

A month ago, I published my Nebius 2030 valuation model, which by now seems already outdated.

As such, I have decided to create a new one, with improved assumptions.

But before that, let me look at a few of the most important things announced in this earnings release.

1. Q1 2026

Revenue: $399M +625%, vs $389M estimate.

ADJ EBITDA: $130M +306%, vs $91M.

ADJ EPS: -$0.39 vs -$0.78.

In short, Nebius grew faster than expected and demonstrated significantly better profitability.

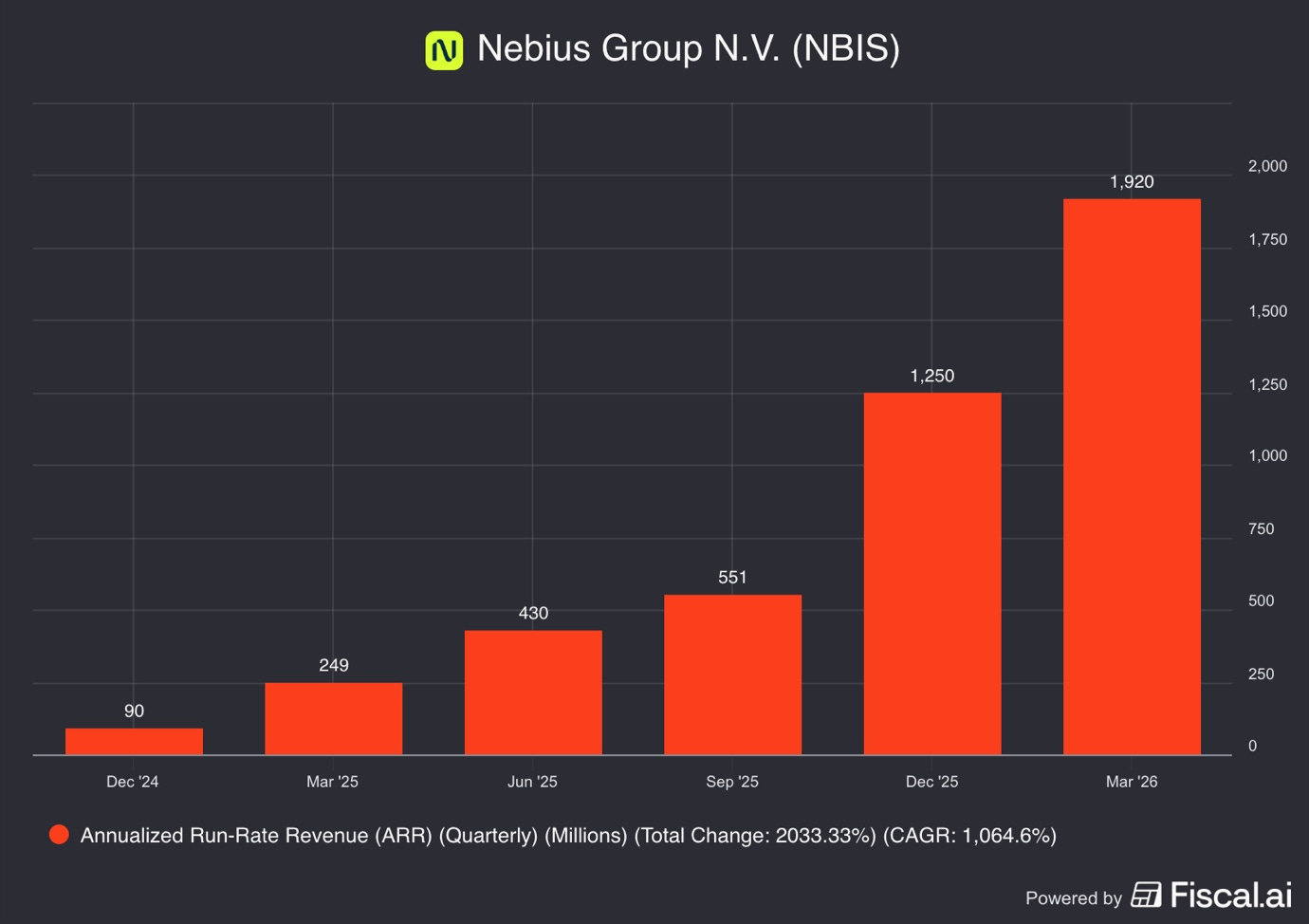

1.1. ARR

ARR grew by 671% Y/Y, 54% Q/Q to $1.92B!

Simply put, Nebius’ March revenues were $160M, compared to $104 in December 2025.

The company reiterated its end-of-year 2026 ARR guidance of $7-9B!

This implies December 2026 revenues of $583-$750M. So, the company expects to grow its monthly revenue by 264-369% in just 9 months. Incredible.

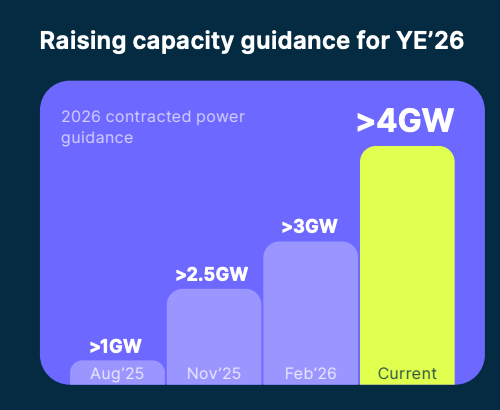

1.2. Capacity Guidance

Most importantly, Nebius increased its end-of-year 2026 contracted capacity guidance from 3GW to 4GW!

This is a 4x increase in guidance since August 2025!

The increase comes from Nebius announcing a new greenfield, fully owned 1.2GW data center project in Pennsylvania.

“Today, we announced a new site in Pennsylvania to support 1.2 GW of power once fully lit live. This is our second owned gigawatt scale site in the United States. Our platform is most efficient when we own the full stack, and we are building towards that. Our owned contracted capacity now accounts for more than 75% of our total power.” Arkady Volozh, Nebius CEO

In this statement, Arkady revealed an important piece of information concerning a criticism often directed at Nebius. Owned data centers account for 75% of their contracted capacity.

Previously, some analysts criticised the company for relying too heavily on rented colocation facilities. It is much faster and cheaper upfront to develop a colocation data center, but it’s more expensive in the long term, as Nebius needs to pay rent and the landlord has to make a margin.

But colocation is just 25% of contracted capacity!

Much lower than many analysts estimated.

However, let’s remember that contracted power is the energy that the utility has agreed to deliver to Nebius, but a lot of the equipment still needs to be built and installed.

Meanwhile, connected power is what is already connected and ready to draw from the grid.

Active power is the power currently being consumed by Nebius clients for AI workloads, and this is what ultimately generates the company’s revenues. So contracted power guidance is great, but only as long as the GPUs actually start running.

Notice that Nebius didn’t give an active power guidance, because there is a lot of uncertainty about when exactly the company could have the facility built, GPUs delivered, and energy connected for active data center activities.

It will be a few years before the 4GW mentioned will be fully active!

Nevertheless, the pace at which this guidance increases clearly suggests that my earlier 3GW active power target for 2030 was too low.

If your head is spinning from this 4x increase in contracted power target, then you are not the only one. This is an absolutely insane target, and very ambitious. Understandably, this means that Nebius will have to invest significantly more to meet this target.

1.3. Capex

Thus, they increase their 2026 capex guidance from $16-20B to $20-25B!

“That is what is driving us to build more and to raise our 2026 CapEx guidance to between $20 billion and $25 billion, which is up from our prior range of $16 billion- $20 billion. This increase reflects investments in our 2027 capacity that will come online early next year. We expect these investments to contribute positi vely to revenue in the first half of 2027, where we already have customer and commitments in place. Meta is one such customer. We need to invest to fully realize it. This requires capital, which is our fourth dimension. We’re doing a very good job in tapping the market at scale.” Arkady Volozh, Nebius CEO

You can’t increase capacity without increasing capex, so this was expected and is totally normal.

I wouldn’t be surprised if capex guidance increases further.

As just $2.5B were spent in Q1, more than $20B will be spent in the next 9 months.

Where will this cash come from?

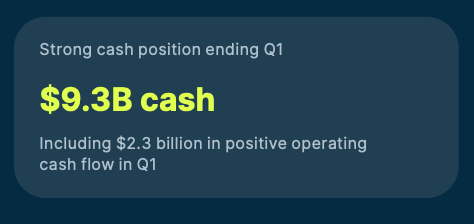

1.4. Cash Situation

Nebius finished Q1 2026 with an incredible $9.3B cash balance!

This already covers almost half of the needs, and a massive increase from $3.7B in Q4 2025. Nebius was able to raise funding from:

$2B from the Nvidia investment.

$4.3B from convertible note issuance.

$3.2B in customer pre-payments.

The $2B Nvidia investment and $4.3B from convertible notes were already known by the market, the $3.2B customer pre-payments were not.

Do you like the chart above?

FiscalAI makes managing investments smarter, faster, and stress-free.

Visualizations

AI-powered insights

Financial data

Earnings transcripts

Portfolio analytics

All in one place. Instead of wasting hours digging through filings and spreadsheets, Fiscal.ai helps you get to the important information in minutes.

Save time, stay organized, and let Fiscal.ai handle the heavy lifting so you can focus on growth.

Join with my link below.

In fact, as of Q1 2026, Nebius has collected $4.8B in customer pre-payments!

This is extremely impressive and again destroys a bear argument. As there were no detailed announcements regarding pre-payments from specific customers, some bears claimed that Nebius won’t be getting any. This clearly disproves that.

Most importantly, only $686M of the deferred revenue liability is current and to be recognized in the next 12 months as revenue.

So Nebius has already received $4.1B in pre-payments from customers for services that will be delivered in 2027 and 2028. Again, this is extremely impressive and demonstrates how strong the demand is for their services.

Which company collects payments from customers more than a year before delivering the services?

Most of the time, in the corporate world, it is the opposite, with clients paying suppliers 60, 90, and even 180 days after receiving the service.

1.5. Acquisitions.

2026 has been busy for Nebius on the M&A front, as they did 3 important acquisitions:

Tavily

Eigen AI

Clarifai

Tavily is an Agentic AI search business. Essentially, Tavily helps companies find the right data and format it in a way that AI Agents can easily understand and process it. Basically, Google Search for AI Agents.

Eigen AI is an inference and model optimization platform that specializes in making AI deployment faster and cheaper.

Clarifai is a deep learning and computer vision company that strengthens Nebius’ managed inference and orchestration offering.

All 3 of these acquired companies will be integrated into Nebius AI Cloud, offering to build a full suite of services that could rival Hyperscalers!

This is how Nebius plans to reach its ADJ EBITDA target!

1.6. ADJ EBITDA Target

Nebius just revealed an 40% ADJ EBITDA target for 2026!

This is a massive improvement from the 10% ADJ EBITDA margin Nebius has in Q2 2025.

The company is achieving scale and operating leverage, thanks to its AI cloud and bare metal offerings.

Despite 684% revenue growth in Q1 2026:

Cost of sales grew only 320%

SG&A expenses grew 136%

R&D grew 85%

SBC grew 102%

Depreciation grew 332%

As it integrates the acquired capabilities and develops new ones, its AI cloud value proposition will only get better and better, supporting margin improvements.

2. Valuation

After rising 148% in 2026, Nebius now trades for a market cap of $53B!