AI Infrastructure play growing ARR by 684%!

Nebius Investment Case!

We are currently in the midst of an AI boom that OpenAI started after stunning the world with the release of ChatGPT.

Many predict that this AI boom will have a bigger impact on the economy and the stock market than the internet!

Nvidia has been the poster child of this new AI revolution, as AI start-ups and cloud hyperscalers are spending hundreds of billions of dollars on GPUs that run AI workloads. This unprecedented demand sent Nvidia’s market cap to $3.5T, making it the second largest company in the world, only behind Microsoft.

While Nvidia became rich by selling AI picks and shovels, Nebius aims to become rich by being an AI refinery and processor.

In gold mining, after miners have used picks and shovels, before gold can be of any use, it must be refined and processed.

Similarly, raw GPU power (picks and shovels) is not enough. To deliver great AI services, companies need to refine AI models to make them better, more efficient, and cheaper.

This is what Nebius does.

In a sense, Nebius is hoping to become the “AWS of AI”!

1. Brief History

2. Business Model

3. Subsidiaries

4. The Opportunity

5. Unit Economics

6. Financials

7. Valuation

8. Conclusion

: Future Prospects and Stock Price Outlook - MiFsee")

1. Brief History

Yandex is one of Europe’s largest internet technology companies. It was founded in Russia in the 1990s and became extremely popular, and is essentially Russia’s answer to Google.

In the 2010s, the company began expanding outside Russia and built various internet businesses in Europe and the US.

However, if you haven’t lived under a rock, you know that in 2022, Russia invaded Ukraine.

Yandex founder and CEO, Arkady Volozh, didn’t agree with this decision and openly spoke out against the invasion. Despite that, his company, Yandex Group, was put on the sanction list by the US, and thus it was delisted from the Nasdaq.

Shortly after, in part due to pressure and in part from his own desire, he sold all Yandex’s Russian assets and kept the foreign assets.

He renamed the remaining company Nebius and announced an ambitious goal to create a large AI infrastructure company.

After the split was completed, Nebius was removed from the sanction list and listed back on the Nasdaq.

2. Business Model

In the simplest of terms, Nebius is a data center business, similar to Amazon Web Services, Google Cloud, and Microsoft Azure. The company makes money by renting access to its data centers.

However, unlike the cloud hyperscalers, which mostly handle general computing, Nebius data centers specialize in handling AI workloads!

Nebius has tailored everything in its data centers to the very specific requirements that AI workloads have.

What is the difference between AI workloads and general Cloud computing?

Well, AI workloads demand extremely high performance, efficiency, and scalability, which Nebius delivers in a few key ways:

Purpose-built AI servers

Customized networking gear

Proprietary server racks

Innovative liquid cooling

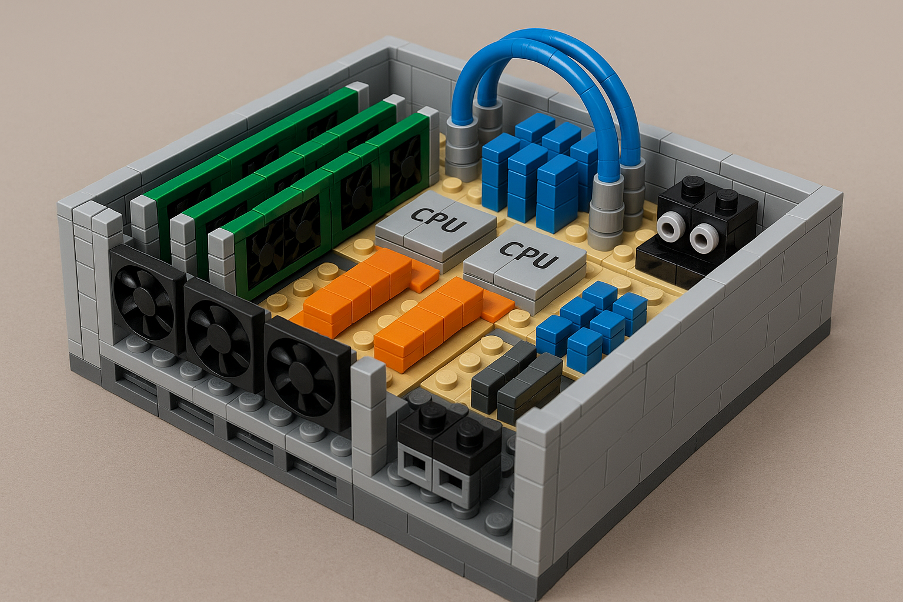

Instead of buying generic off-the-shelf servers from Supermicro, Nebius designs its own server infrastructure.

An AI server is basically a Lego. It contains GPUs, CPUs, memory chips, networking equipment, cooling systems, and more.