Celsius is a Rockstar!

Taking the Pepsi partnership to the next level!

Celsius just delivered a huge Friday morning announcement that changed my weekend plans. Originally, I was planning to finalize a small-cap investment case, but this news couldn’t wait.

Celsius just signed a new deal with Pepsi, taking their partnership to the next level!

1. Pepsi will take over Alani Nu distribution!

2. Celsius acquires the Rockstar energy drink brand from Pepsi!

3. Pepsi expands its investment in Celsius and now owns 11% of the company!

The market clearly liked the deal, sending the stock up 5%. However, I think the jump should have been much higher.

This is yet another transformative deal that is poisoning Celsius to not only execute a stellar turnaround, but to possibly challenge Monster for the number 2 energy drink company spot. A reminder that Celsius stock was in a huge drawdown at the start of the year, down close to 80% from May 2024 highs.

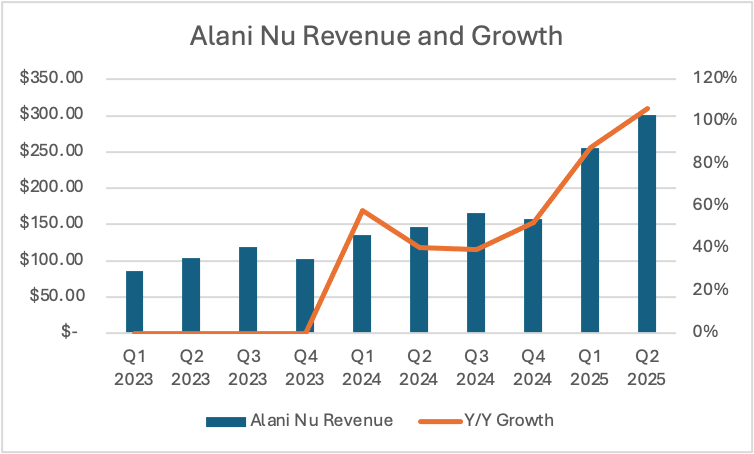

However, so far this year, the stock is up 139%, as organic growth returns to the Celsius brand and the Alani Nu acquisition has proven to be a masterstroke!

In this article, I will analyze the deal, its implications, and create a new valuation model!

Let’s dive in!

1. Pepsi Alani Nu Distribution

2. Rockstar Energy

3. Pepsi’s Stake in Celsius

4. Valuation and Final Thoughts

1. Pepsi Alani Nu Distribution

Let’s start with the biggest and most important part of the announcement.

Pepsi will now handle Alani Nu distribution in the US and Canada!

When Celsius closed the Alani acquisition, this was the key question on analysts minds. Celsius was vague at the time, likely to not create any issues with current distributors and negotiate better terms with Pepsi.

Before being acquired by Celsius, Alani’s distribution was done through a network of independent distributors, direct-to-consumer sales on Amazon, various direct-to-retailer relationships, and a partnership with Anheuser-Busch.

Despite this scattered distribution strategy, Alani achieved incredible success, growing sales by 88% and 106% in Q1 and Q2 of 2025!

By not rushing into an agreement with Pepsi, Celsius was likely able to get better terms using this success as a negotiating point. Essentially saying to Pepsi, “Hey, we don’t really need you, we are growing sales 106% without you”.

And I think they got a good deal:

Pepsi will contribute funding for distributor buyouts.

Celsius assumes the Pepsi energy drink “Captaincy” role.

The announcement said that Pepsi will contribute funding for distributor buyouts. Often, distributors sign long-term, regional exclusivity agreements with beverage companies. In situations when a distribution agreement is broken early, large and significant compensations have to be paid.

When Celsius moved their sales to Pepsi the first time, the company paid over $200M in termination payments. Pepsi didn’t contribute, so this burden was entirely on Celsius. This time, Celsius negotiated a contribution, however, the announcement was deliberately vague. I suspect this was so distributors would negotiate in good faith and wouldn’t ask excessive amounts just because “Pepsi is paying anyway”. But I expect that this time the termination payments will be larger than $200M, as Alani Nu sales are larger than Celsius when the first Pepsi deal was signed in 2022.

Next, Celsius is now Pepsi US and Canada’s strategic energy drink “Captain”.

“The Captaincy provides Celsius Holdings with strategic control over the allocation of the Celsius Holdings portfolio (CELSIUS®, Alani Nu®, and Rockstar Energy®) energy planograms, SKU prioritization and promotion strategy, including certain priority periods.” CELSIUS AND PEPSICO EXPAND LONG-TERM STRATEGIC PARTNERSHIP Presentation

This is not just a marketing label for a corporate partnership.

In consumer packaged goods, a category captain is the manufacturer or brand that a distributor allows to lead planning and execution for an entire category (in this case, energy drinks). It goes beyond being just another supplier,

the captain provides key input on decisions, such as what goes on the shelf, how much space it gets, how it’s promoted, and when!

Essentially, this means that Celsius will be able to decide how each brand is promoted within Pepsi’s distribution system. Celsius, Alani, and Rockstar each have different brand positionings, so being able to adjust distribution, placement, and promotional strategies will enable Celsius to increase sales. At the same time, the company will use Pepi’s distribution network and logistics to push brands to more stores in a cost-effective way.

Before this deal, Alani’s position was relatively weak in two areas, food service and convenience.

Pepsi will help with both!

As we can see in the picture above, Alani Nu was available in total stores with 87% of ACV.

ACV stands for all-commodity value, and it basically means that Alani is available in stores that generate 87% of the energy drink sales. However, if we look at convenience, we see that this number is only 69%.

Alani is in a great position to close this gap using Pepsi’s distribution network!

I think the convenience segment warrants more explanation, as at first glance it doesn’t seem like such a big difference. This doesn’t mean that Alani generates 69% of potential sales, no, it means that Alani is available in convenience stores that generate 69% of energy drink sales.

This means that very likely that Alani is not available in some of the most important convenience channels!

Energy drinks are often spontaneous purchases that disproportionately happen in convenience stores, gas stations, and fast-food retailers. This trend is driven by people who purchase energy drinks when they are on the move to or from work, school, the airport, or somewhere else.

Closing the 11% and 29% gaps in total retail and convenience distributions could generate a much larger increase in sales than these percentages would suggest!

And this is only from the increased distribution, we haven’t yet touched the marketing aspect.

Having a complete distribution means that promoting the brand gets much easier. Methods that previously would be too expensive and not effective suddenly become financially viable.

When a product is not broadly available, it doesn’t make as much sense to have large national campaigns, as they would promote the product to people who can’t buy it. Once fully distributed, Celsius will be able to use large and national campaigns to promote Alani Nu to millions of people. TV ads, expensive influencer partnerships, event sponsorship, and possibly even a Super Bowl ad.

Alani Nu has unprecedented appeal to young women who previously shunned the overly masculine and macho energy drink category!

Celsius was able to grow this brand by 106% in Q2 2025 without Pepsi. I think sales could absolutely explode in the next few years.

This is a completely new category, and there is ZERO competition from Red Bull and Monster in this “girl” brand energy drink space. As the Red Bull example shows, being the first could position you to dominate a category for decades.

2. Rockstar Energy

As part of this expanded partnership, Celsius is acquiring Rockstar Energy’s US and Canada business from Pepsi for $585M.

Rockstar is your classic 2000s energy drink brand that uses the same design and marketing elements as Monster and Red Bull.

Founded in 2001, the brand has often been associated with partying, extreme sports, and music festivals, with “Party like a Rockstar” being its famous tagline.

While sales were relatively good, they were nowhere close to the leaders, Red Bull and Monster. And after the strong success of the Monster and Coca-Cola partnership, the gap between the leaders and Rockstart only grew. Thus, in 2020, Pepsi acquired the brand for $3.85B in hopes of challenging Monster and Coca-Cola in the energy drink space.

Rather than elevating the brand, Pepsi essentially destroyed it!

The company attempted a rebrand to make Rockstar more appealing to a mass audience, but instead, it made a weird Frankenstein brand that appealed to nobody.

A new logo

Can design was simplified

Flavors were changed

Marketing campaigns altered

Instead of a memorable and distinct brand message that said “Party like a Rockstar”, the brand became generic and “corporate”, with using 3 new failing tag lines in quick succession “Life is your Stage”, “Press Play”, and “You Can Own Any Moment”.

Commentators on Reddit say that it “doesn’t taste the same,” and thus sales have suffered.

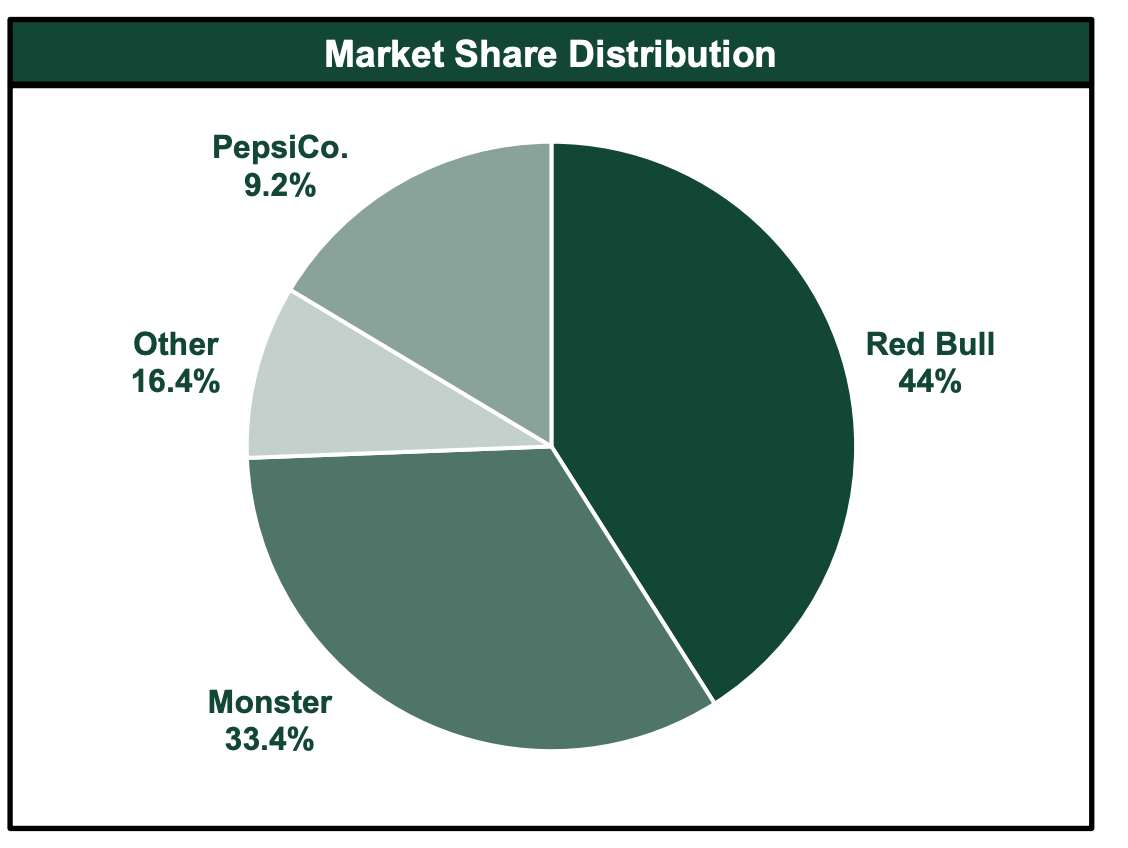

The above pie chart shows the 2020 US energy drink market share distribution from Oregon Consulting Group. According to them, Pepsi had an estimated 9.2% market share, primarily stemming from Rockstar.

Today, they have around a 2% market share, with retail sales of just $643M!

I couldn’t find the exact retail sales number at the time of the acquisition, but it was likely much higher than that. As a result of weak sales, Pepsi was forced to write down $1.78B as a goodwill impairment loss.

Thus, it is not a surprise that Pepsi is happy to get rid of Rockstar, as they clearly have no idea what they are doing.

But why would Celsius want a failing brand?

1. Because they are getting it for a bargain price.

2. It doesn’t cannibalize existing brands.

3. Improves scale and operational synergies.

4. Increases their marketing power.

5. Strengthens their negotiating position with Pepsi.

This management team has a great track record of growing and integrating brands. Pepsi mismanaged Rockstar by trying to make it everyone’s brand. Celsius clearly understands how important brand segmentation is, so I think it is likely that they will refocus Rocsktar towards its early roots of party, festival, extreme sports, male-targeted audience.

While this puts them on a frontal collision course with Monster and Red Bull, I think Celsius is in a great position to take market share. Also, for Celsius, by simply returning Rocskstar to pre-Pepsi market share would already be a great success, whereas for Pepsi, that would have been a failure.

My hope is that they copy what the Coca-Cola company is doing and partner with a spirits brand.

The products in the left picture above are real, Jack&Coke and Absolut Sprite, and according to the CEO of Brown-Forman, they are selling incredibly well. In the right picture are product concepts I made with Google’s AI image generator (they look great, right?) Rockstar Smirnoff and Rockstar Captain Morgan. I am sure products such as these would fly off the shelves.

The ready-to-drink alchocol cocktail segment is growing, and mixing energy drinks with alchocol has been popular for decades. Celsius could never do this with Celsius and Alani brands, as spirits don’t fit their brand image, but there are no such issues with Rockstar.

This is just a single idea, there are many ways in which Celsius could revitalise this struggling brand!

3. Pepsi’s Stake in Celsius

As part of the deal, Celsius issued $585M of 5% preferred equity shares to Pepsi. These preferred shares carry a guaranteed 5% dividend for 7 years if the stock stays above $51.75, around $41M per year, which would be $287M over 7 years.

So, essentially, the real final price of Rockstar Energy is $872M. During the investor update call with analysts, the company guided for annual sales of around $250M after integrations and skew optimizations (some beverages that might compete with Celsius or Alani Nu will be eliminated).

This implies a valuation multiple of around 3.5 times optimized sales!

I think this is a really good price. With a modest turnaround, this could be $1B a year brand, generating $100-200M in earnings.

Now, on a fully converted basis, Pepsi owns around 11% of Celsius!

Additionally, the company will nominate another board member, and now controls 2 out of 10 board members. However, if I understand the filing correctly, Pepsi has the right to force Celsius to buy back the preferred shares under certain conditions. So if Celsius underperforms, they might be forced to buy back the shares.

Furthermore, Pepsi has agreed not to increase its stake in Celsius for 7 years. This is to guarantee that Pepsi doesn’t increase its ownership in Celsius behind Celsius management’s back.

For those wondering whether Pepsi could be looking to acquire Celsius, don’t bother.

It is very unlikely that Pepsi has any intentions to acquire Celsius, as simply put, they can’t afford it!

Celsius trades for a market cap of $16B, a 50% buyout premium offer would mean a purchase price of $24B. Pepsi simply doesn’t have that kind of money, and they also can’t raise that much debt.

The company only has $8.6B in cash, yet they have $48.5B in debt and pay out more than 100% of its FCF as dividends and share buybacks.

Of course, they could attempt an all-equity deal, but that would require huge dilution, and their shareholder base would revolt. Especially considering their last energy drink acquisition didn’t go so well, so I doubt they would triple down on the energy category.

4. Final Thoughts and Valuation

A new valuation model and my final thoughts on Celsius are available for Global Equity Briefing Premium members.

Thank you for reading Global Equity Briefing!

Global Equity Briefing is an investing newsletter with a focus on analysing global companies. I have written highly detailed Deep Dives on Nu Bank, Ferrari, Palantir, Grab, Celsius, Mercado Libre and Hello Fresh!

Additionally, I have written Investment Cases on Meta, Amazon and Google! and comparisons of Visa vs Mastercard and Eli Lilly vs Novo Nordisk!

My goal for 2025 is to write around 4-6 articles per month!

Subscribe to get all my articles as soon as they are released!

Support my work by becoming a paid subscriber!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.