Is Hims a buy?

Hims and Hers. Equity Research! Part 3/3

Hello Global Investors!

Welcome to the 3rd and final part of my Hims and Hers Deep Dive.

In Part 1, we explored their business model, GLP1 shortage, and subscriber statistics!

Meanwhile, in Part 2, we looked Hims and Hers management, competitors, and risks.

I recommend people give them a read before continuing further!

Today we will look at Hims and Hers opportunities, valuation, and financials!

Let’s go!

1. Opportunities

2. Financial Analysis

3. Valuation

4. Conclusion

1. Opportunities

Let’s look at the biggest opportunities for Hims to grow the business!

Obesity

As the world went through the Industrial Revolution, its ability to produce affordable food exploded. Cheap food significantly reduced the number of starving and malnourished people. However, it also created a new issue, obesity.

The US is the fattest country in the world, with more than 40% of adults considered overweight or obese.

For decades, diet and exercise were the only effective remedies for this issue. While it remains the most effective solution, many people lack the willpower for it.

In some sense, Obesity has become a neurological and mental condition!

But as a result of the GLP1 revolution, for the first time in our history, these food addicts have an effective pharmaceutical solution!

GLP1s are hormonal medications that work by essentially tricking a patient’s brain into not being as hungry and not enjoying food as much.

As you can see in the chart above, researchers at Grand View Research forecast the US obesity treatment market to grow with a 24.2% CAGR to reach $48.5B by 2030!

The majority of this market will go to large pharmaceutical companies such as Novo Nordisk and Eli Lilly. However, the market is so massive that even capturing 5% of it could generate $2.4B in revenue for Hims.

Ozempic, possibly the most famous GLP1 drug, has patent protections in the US till 2031. Hims will be able to offer generic versions of it through its digital platform.

Before 2031, there will be other earlier and less effective GLP1 drugs that will lose patent protection, such as Liraglutide, whose patent protection expired last year, and Hims expects to start offering it this year.

Why would someone use a less effective drug?

Generic drugs tend to be 80% cheaper than brand names and can be purchased more easily. Additionally, Hims can personalize them with compounding to reduce side effects.

An aspect often overlooked about obesity in the context of Hims is that obese people often suffer from other medical conditions. Poor diet is a huge contributing factor to diabetes, skin conditions, hair loss, mental health issues, ED, poor reproductive health, and more. This makes obesity treatment a gateway for other treatments. Hims could acquire obese customers who want to lose weight and cross-sell them treatment for other conditions.

Chronic Conditions

Chronic conditions that require constant care and observation are perfect targets for Hims.

A patient who has been prescribed an effective medication to treat or alleviate the symptoms of a particular condition is less likely to cancel the subscription!

Hims targets common chronic conditions with long treatment times and high potential for earnings. Some areas of focus include testosterone therapy, menopause care, sleep disorders, PTSD, fertility, diabetes, and more.

Menopause care is a $6B market in the US, testosterone therapy is $1B, the sleep disorder aid market is valued at $29B, PTSD is $1.8B, fertility a $8.4B, and diabetes is $49B.

And these are just some of the conditions, the total addressable market is truly massive!

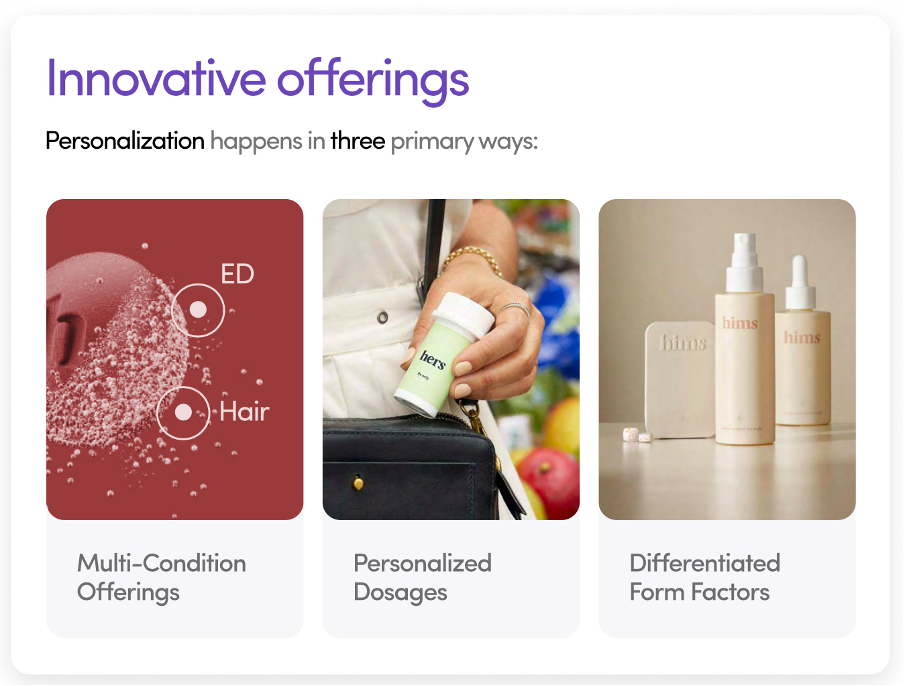

Personalised Treatments and AI

Too often, in the hectic and expensive US healthcare system, people feel like cattle.

Doctor appointments take forever, the bureaucracy is exhausting, and treatments are repeatedly ineffective.

Hims is building a platform that aims to provide more personalized treatments!

Each medical condition is unique, and the way patients react to medicine varies. Some conditions and their treatments interfere with the treatment of other conditions. The faster the doctor and the patient can recognize such cases, the faster the right solution can be identified.

Hims wants to make that easier by building a platform that improves the data flow from the diagnosis to the doctor to the pharmacist. Faster and more accurate decision-making has the potential to improve patient outcomes.

Drug doses can be adjusted, treatment delivery mechanisms can be changed (pill to liquid, etc.), unique blends can be created, test results digitally viewed, analyzed, and changes tracked, and AI-supported chatbots for simple questions.

For many conditions, laboratory tests are crucial for diagnosis and observation. So, to offer truly customized and personalized treatments, lab tests are a must.

In an ideal scenario, customers would take constant lab tests to track their vitals. If the results indicate that a change in treatment is necessary, they could be quickly informed, and a new treatment mailed, saving time.

Recently, Hims acquired an at-home lab testing business, clearly positioning itself to expand into this highly promising area!

Hims will mail patients a blood lancet device to extract a small amount of blood, which will then be mailed back for analysis.

Compared to lab-drawn blood tests, these kits can test fewer markers and could have lower accuracy. However, they are great for monitoring certain health markers such as hormone levels, cardiac risk, stress indicators, cholesterol, liver and thyroid functions, and prostate health.

In the future, I find it likely that Hims will offer personalized supplement vitamin kits based on one’s blood tests. That would be another market with a multi-billion-dollar TAM.

According to Hims, 55% of their subscribers use a personalized product. Personalized medicines increase customer switching costs, thus reducing churn.

This is a big differentiating factor that helps Hims attract and keep customers!

To improve their ability to create personalized treatment plans, Hims is building various AI tools. MedMatch is their key AI tool that facilitates data-driven decision making.

This software analyzes a vast amount of anonymized data collected from millions of customers. Historical clinical visits, demographics, the administered treatments, and the resulting patient outcomes are all sent to MedMatch for AI analysis.

By processing this large dataset, MedMatch can generate data-driven insights and recommendations. This could enable doctors to make more informed decisions, improving outcomes.

With their 2M subscribers, Hims has the potential to generate a lot of high-quality data to improve the capabilities of their AI systems!

Partnerships

While Hims doesn’t work directly with health insurance companies, there is still potential to generate revenue and gain more customers through various other partnerships.

Corporate deals that offer employer-subsidized Hims plans to employees could help the company gain customers.

Hospital partnerships for patient monitoring and after-surgery care.

Private clinics could offer their patients special Hims bundles for certain conditions in return for Hims referring their subscribers to clinics for in-person procedures.

Pharmaceutical manufacturers could partner with Hims to use their data and insights during trials and research for better drug development.

Most excitingly, in the future, there could be a SaaS aspect to Hims, as the company could provide access to its digital platform and all its capabilities to hospitals and clinics.

Digital patient record keeping, AI tools, doctor notes, voice notes, video notes, digital consultations, drug prescriptions, fulfillment, lab testing, and monitoring.

Instead of patients paying Hims, clinics or hospitals would pay Hims a subscription fee.

There is potential for billions in high-margin, recurring software revenue!

2. Financial Analysis

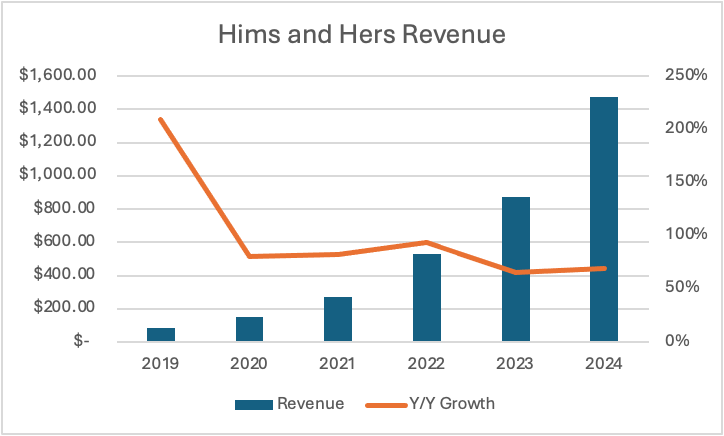

In 2024, Hims reported revenues of $1.48B, up 69% Y/Y, net income of $126M, up 636%, and FCF of $209M, up 272%!

Let’s look at Hims finances in more detail!

Revenue

Driven by strong adoption of their GLP1 offerings, revenue reached a new record of just shy of $1.5B, an increase of 69% Y/Y.

In the graph above, we see how revenue growth reaccelerated in 2024, from 65% growth in 2023.

In just the last 5 years, revenue has grown more than 3 times, a CAGR of 78%!

This revenue growth was largely due to the strong subscriber numbers. Since 2020, subscribers have grown 633%, whilst monthly ARPU only grew 28%.

The company makes some revenue from wholesale sales of certain Hims and Hers branded merchandise, but it is immaterial, just $39M in 2024.

Marketing Expenses

As a D2C company, Hims spends ungodly sums on marketing to acquire and retain customers.

In the chart above, we see that Hims spent $679M on marketing in 2024, 46% of their revenues!

This is a slight improvement from 46% Hims spent on marketing in 2023.

It is way below the 2019 level of 70%, and in the last 4 years has stabilized at around 50%.

While their marketing expenditures are significant, they have been quite effective, and per Hims investor presentation, the effectiveness is improving.

In Q1 of 2019, Hims spent $12M to acquire customers and generated $19M in gross profit during the year. That means Hims generated a 58.3% gross profit return on ad spend.

By Q1 2024, Hims cost to acquire customers increased to $113M, however, they generated $457M in gross profit, a 304% return on ad spend.

From Q1 2019, marketing costs grew by 842%, but the gross profit generated grew by 23,053%!

That is a huge improvement in unit economics and marketing efficiency! The payback period now sits at less than 6 months!

Other Costs

As mentioned, in 2024, marketing was the largest expense category for Hims, 46% of revenue and 48% of all expenses.

In the pie chart above, we see the operating expense structure and how it has changed since 2020.

Technology costs have remained relatively constant, but marketing expenses have exploded.

This is because Hims has already built a platform, so today it has to spend more on acquiring customers than on running the platform!

Meanwhile, the cost of revenues has decreased as Hims unit economics have improved.

Lastly, operating, general, and administrative costs take a much smaller share of overall expenses as thanks to increased economies of scale Hims can operate the business more efficiently.

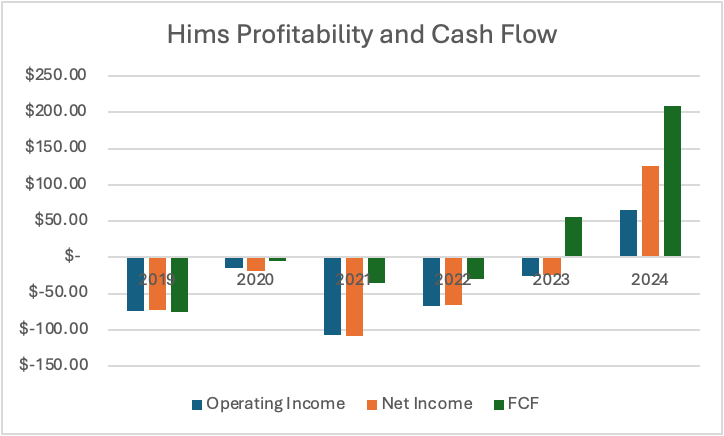

Profitability and Cash Flow

In 2024, Hims had an operating income of $66M, up 354% Y/Y, net income of $126M, up 636%, and FCF of $209M, up 272%. Net income was higher than operating income, largely because of a $54M net tax benefit.

2024 was the first year that Hims showed stable profitability and cash flow. This was largely driven by the GLP1s. I think it is quite likely that if there had been no GLP1 shortage in 2024, Hims would not have been profitable. GLP1s accelerated Hims sales and profitability paths.

Taking into account the one-time tax benefit in 2024 and depending on the volume of their GLP1 sales in 2025 and the ability to offset any lost GLP1 sales with new offerings, there is a possibility of Hims profitability decreasing in 2025 and 2026.

However, in my opinion, the availability of GLP1s does not affect Hims long-term investment case!

GLP1 is just one area of a company, and they have many promising business lines.

In the above graph, I have placed Hims margins from 2019 to 2024. We can see that they were improving even before the GLP1s.

Gross margin stands at a strong 80%, indicating quite favorable unit economics, leaving plenty of margin to reinvest in marketing and building the platform.

Operating and net income margins have jumped from negative 90% to 4.5% and 8.5%, respectively. Hims has reached a scale at which they require fewer expenses for each additional dollar of revenue.

FCF margin of 14% shows that the company doesn’t only posts paper profits but also generates a healthy cash flow. The difference between net income and FCF can largely be explained by the non-cash SBC expense being 6.3% of revenue.

Balance Sheet

In the graph below, we can clearly see that Hims has a strong and stable balance sheet. The company has $300M in cash, whilst Debt stands only at around $11M.

Cash flow to debt ratio of 20 means that Hims can pay off all its debt 20 times with just a year’s worth of cash flow.

3. Valuation

As of April 2025, Hims has a market cap of $6B, and the stock is up 178% since the IPO.

In the graph above, we can observe an incredible rally in Hims stock in 2024 and early 2025. In the first 2 months of 2025, Hims was up a whopping 173%, driven by strong Q4 2024 earnings and 2025 guidance. However, since the peak, the stock has collapsed 60% as the FDA ended the GLP1 shortage.

In the above table, I have placed some of Hims key valuation metrics.

The company now trades for a P/E of 51 and a P/FCF of 29, implying investors price in significant growth.

Analysts expect Hims to grow revenue by 58% in 2025, and by 127% by 2027. Additionally, significant improvements in operating profits are expected, with EBIT set to grow 149% this year and 385% over the next 3 years!

Meanwhile, FCF generation is expected to remain strong, growing by 139% in the next 3 years.

However, as the 2024 net income was propped up by the tax benefit, EPS is set to grow slower than revenue, but still a notable 108%.

Taking into account these estimates, the 2027 P/E is 23, P/FCF is 12, and FCF yield is 8.3%!

Let’s analyze what kind of operational performance is priced in and if there is still some potential upside left.

Valuation Model

I have built a simple valuation model that tries to estimate the 2030 stock price based on certain operational metrics.

Let’s say that by 2030, Hims has around 5M subscribers, and monthly revenue per subscriber will grow with a stable 3% CAGR from 2024 to reach around $67.

Marketing costs fall from 46% of revenue to 40%, and other costs from 50% to 47%, enabling the operating margin to reach 13% and net income margin 10% by 2030.

In such a scenario, we get to revenue of $4.17B, operating profit of $542M, and $417M in net income!

Assuming 4% yearly dilution and an exit P/E of 30, we get to a market cap of $12.5B and price per share of $27.35!

That is just an upside of 67.5%, a CAGR of 9%, not very exciting!

So, let’s improve the assumptions!

Subscribers reach 10M, not 5M. Monthly revenue per subscriber grows with a 5% CAGR rather than 3%, whilst margins are a few percentage points higher than in the earlier model.

We get to 2030 revenues of $8.96B, operating profit of $1.5B, and net income of $1.17B!

Keeping the same 4% yearly dilution and 30 P/E exit multiple, we get to a market cap of $35B and price per share of $128!

So in such a scenario, Hims would return 368%, a CAGR of 29%!

Essentially, this means that the market currently is pricing in 5M subscribers, a low digit percent yearly ARPU growth, and a 10% net income margin.

However, if by 2030 Hims has more than 5M subscribers, ARPU CAGR is in mid-single digits, and profit margin is in the mid-teens, then there is a huge upside!

4. Conclusion

Hims and Hers is working to bring a much-needed dose of innovation, digitization, and personalization to the stale and slow US healthcare industry!

During the last few years, the company went from a small start-up to a multi-billion-dollar technology-driven healthcare company. While the hyper-mega growth stage is over, Hims is well-positioned for fast, steady growth.

The company is operating in many promising healthcare segments with many billion-dollar TAMs, such as men’s and women’s sexual health, mental health, hair loss, dermatology, obesity, and more!

Moreover, Hims is constantly innovating and investing in the platform to expand the breadth of the offering and improve customer experience!

The company has so far avoided huge acquisitions and instead focuses on small bolt-on deals. It is expanding its capacity to offer unique and personalized treatments with investments in laboratories, pharmacies, fulfilment, drug compounding, and AI.

However, the competitive dynamics are likely to intensify, as well-funded start-ups such as Ro and Teladoc invest to compete with Hims. Whilst the shadow of the mega gorilla, Amazon, looms over the whole telehealth industry!

At the same time, serious risks as lawsuits, regulatory issues, and customer churn threaten to slow down the company.

Hims execution in the last few years has been excellent, and Andrew Dudum has demonstrated his ability to outsmart competitors to deliver unprecedented growth and strong profitability.

Whilst Hims valuation is not crazy, the valuation model shows that it is quite demanding.

If by 2030 Hims, has over 5M subscribers, over 5% ARPU CAGR, and 10%+ profit margins, the stock could do quite well, however, if the growth slows down, the stock will underperform!

Thank you for reading Global Equity Briefing!

Global Equity Briefing is an investing newsletter with a focus on analysing global companies. I have written highly detailed Deep Dives on Nu Bank, Ferrari, Palantir, Grab, Celsius, Mercado Libre and Hello Fresh!

Additionally, I have written Investment Cases on Meta, Amazon and Google! and comparisons of Visa vs Mastercard and Eli Lilly vs Novo Nordisk!

My goal for 2025 is to write around 4-6 articles per month!

Subscribe to get all my articles as soon as they are released!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.