Is Sea Limited a buy?

Sea Limited. Equity Research! Part 3/3

Welcome to the final Part of the Sea Limited Deep Dive!

In Part 1, I explored how Sea came to be and how this fast-growing technology company from Singapore makes money!

In Part 2, I looked at Sea’s competition and explored the risks the company must manage while operating a fintech and e-commerce business in Southeast Asia!

Today, I will tell you what the opportunities are, how do the finances look like, and most importantly, I will look at the valuation!

Let’s finish the Deep Dive!

1. Opportunities

2. Financial Analysis

3. Valuation

4. Conclusion

1. Opportunities

Sea has built a business model that stands to deliver strong growth in the next decade and beyond.

There are many beneficial trends behind this growth, but the key opportunities come from:

Regional Economic Development

Geographic Expansion

Financial Services

Advertising

Video Games

Regional Economic Development

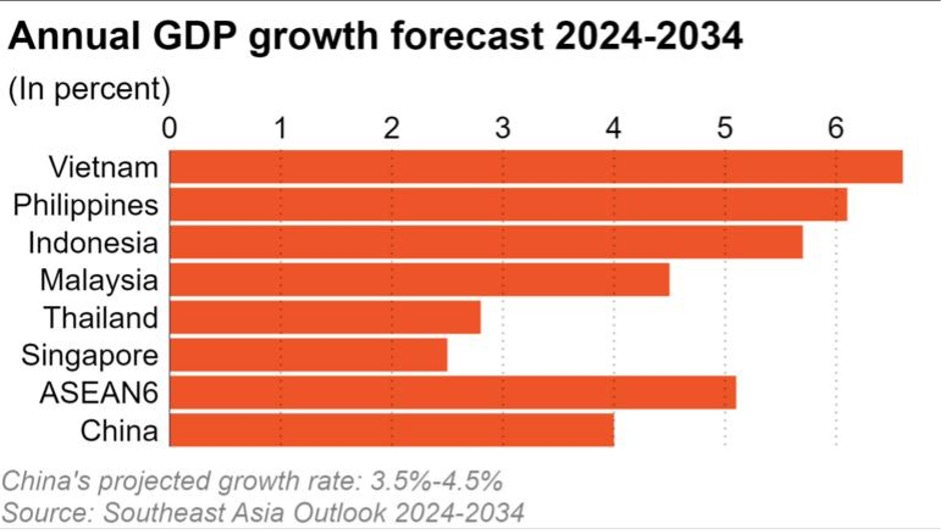

According to the IMF, Southeast Asian economies are the fastest-growing in the world, expanding by 4.1% in 2024. This is a stark contrast to Europe, which essentially is not growing, whilst North American GDP expanded by 1.6% in 2024.

Over the next decade, experts predict that Southeast Asia will grow with an annual rate of 5.1%!

Vietnam and the Philippines are set to lead the pack with a growth rate of over 6%!

Key industries driving this growth are natural resource extraction, tourism, manufacturing, and services.

According to ASEAN, economic growth will lead to an estimated 200M joining the middle class!

This new middle class will have higher disposable incomes, driving huge GMV growth for Shopee, higher loan and transaction volumes for Monee, and more in-game purchases for Garena.

Furthermore, in addition to having some of the fastest-growing economies, the region exhibits many other trends that are beneficial to Sea.

Governments are increasing investments in digital and physical infrastructure, connecting regions, thus making them attractive to expand into. Simply put, roads are getting better, and the internet is becoming more widely available even for lower-income households.

Increased urbanization will drive millions to cities, expanding Shopee’s user and seller bases.

High mobile penetration is enabling Monee to onboard millions of underbanked people.

Growth of local manufacturing will put goods closer to end users, improving supply chains and driving synergies in logistics.

Geographic Expansion

Shopee currently operates only in 7 countries in Asia and Brazil, leaving the field wide open for future expansion!

The company previously attempted to expand in France, Spain, India, Mexico, Chile, Colombia, and other countries, but quickly exited them.

Sea expanded aggressively during the pandemic boom, but changing market conditions quickly made that untenable.

Garena’s revenue collapsed, causing the overall revenue growth to slow down, sending the stock into the dirt.

These new markets are much more competitive than Shopee’s core markets, with key players such as Amazon and Mercado Libre dominating. This meant that Shopee would have had to raise billions of dollars of additional capital to compete.

A collapsing stock price meant that stock issuance was off the table.

At the same time, raising interest rates made debt issuance expensive, whilst a 2.6% 2023 EBIT margin made it financially irresponsible.

Sea simply didn’t have enough capital to bear the losses in these new markets, so the company made the prudent choice to exit!

However, today the situation is different.

Sea is in a much better financial situation to fund the expansion.

They have $8.4B in cash, $1B in TTM EBIT, and their core markets are demonstrating strong growth.

I find it quite likely that Shopee will expand to new geographies in the next few years.

Financial Services

Unfortunately, access to affordable and easy-to-use financial services is still lacking in Southeast Asia. It is estimated that 70% of the region’s workforce is employed informally, without a contract, and gets their salary in cash.

According to the 2023 ASEAN Monitoring Progress report, 44% of adults, around 265M people, don’t have a bank account.

Additionally, many small businesses struggle to access basic banking services, such as bank accounts, credit, and insurance.

For instance, in Malaysia, only 29% of small businesses have a loan of any kind, while in the Philippines, only 30% have a dedicated business bank account. Even when credit is available, without government support, small enterprises have to pay an exorbitant interest rate, with the interest rate spread between what large enterprises and small businesses pay being between 6.5% and 11.5%.

This presents Monee with a generational opportunity to become one of the largest financial services companies in the region!

In 2022, when Monee last disclosed MAU, they had 52.7M users.

I think it is entirely possible for Monee to gain 100M new users in the next decade!

Gaining millions of new users would be quite impressive, but let’s remember that Monee doesn’t operate independently, it’s part of the emerging Sea ecosystem, creating a growth flywheel.

Running a financial services business next to an e-commerce business is a great way to turbocharge both businesses.

Lending to both sides of the transaction creates a self-reinforcing growth cycle. Merchants use loans to sell more on Shopee, whilst customers use loans to buy more.

Sea collects interest from both, a great marketplace business model!

In Q1 2025, Monee loan active users increased by 50% Y/Y to reach 28M, whilst the total loan principal outstanding reached $5.8B, an increase of 13.7% Q/Q and 75.8% Y/Y.

In the graph above, we can see how impressive their loan origination has been.

In Q1 2023, the loan principal as a % of Q1 GMV stood at 10.8%, but by Q1 2025, it had grown to 20%. This metric measures lending penetration into the Shopee ecosystem and demonstrates a strong adoption of their financial services.

There is huge potential for this ratio to grow even past 100%, because a $1 of GMV could theoretically generate $2 of loan principal, because, as we just discussed, Monee can fund both sides. Also, loan terms are often longer than one quarter.

Additionally, loans could be extended outside the Sea ecosystem.

Advertising

Having hundreds of millions of eyeballs that spend over $100B a year is an extremely valuable asset that could end up generating the company billions in advertising revenue.

In the above graph, we see the development of Amazon’s advertising business.

In 2019, Amazon generated $12.6B from advertising, around 4.5% of total revenue. In just 5 years, they grew this business more than fourfold to $58B, and now it constitutes 9% of total revenue.

This is a clear-cut example of the power of having a large and monetizable customer base. Garena has 662M active customers. There is potential to offer ad spots to Shopee sellers to advertise various gaming-related accessories.

Monee has over 50M customers, generating billions in transaction volumes. Monee partners would pay a pretty penny for better visibility.

Shopee Food is early in its monetization, and offering better visibility for restaurants could generate significant income, as Uber has demonstrated.

Most importantly, sponsored search results in the Shopee marketplace will become paramount for merchants eager to stand out from the crowd.

There is a huge potential for advertising to become a similar contributor to Sea’s overall business as it is to Amazon’s!

Video Games

As already mentioned, an estimated 200M people are set to join the Southeast Asian middle class. This newly created middle class will want to entertain themselves, and gaming is one of the best value per hour ways of doing so.

With its strong position in the Southeast Asian mobile gaming market, Garena is in a great position to capture a significant slice of the expanding gaming pie!

Moreover, the video game industry is in the early stages of transitioning from the traditional model of buying a game and running it on one’s device to a subscription and cloud streaming model.

Instead of a freemium model that depends on microtransactions, Garena could offer access to a particular game, for let’s say $1 a month, or a portfolio of games for $5M a month.

A cloud gaming subscription service would significantly increase the long-term value (LTV) of a paying gamer.

With 662M active users, Garena is uniquely situated to be a distribution partner and a cloud gaming host for various video game studios!

2. Financial Analysis

Sea closed 2024 with revenues of $16.8B, +28.8% Y/Y

Operating income of $662M +93%

Net income of $444M +194.8%

Free Cash Flow doesn’t matter because the financial services business completely distorts it, making it useless to gauge the overall company performance.

Overall, 2024 was a great year after a disappointing 2023.

Now let’s look at Sea’s finances in more detail.

Revenue

As of Q2 2025, Sea’s revenues are $17.9B, an increase of 30.3% Y/Y. Notice that it is above the 2024 growth rate of 28.8%.

This is because Q1 2025 delivered an exceptionally strong performance in the financial services business, which grew 57.6%, twice as fast as the 28.3% growth in the e-commerce business.

Overall, if we look at the graph above, we see that Sea has grown revenues by 6,037% from a mere $292M in 2015.

This means that Sea achieved a revenue CAGR of 56.1%!

Such strong performance was accomplished thanks to exceptional execution and the management team’s vision to expand beyond video games.

In 2019, Garena was over 1/3 of Sea’s entire business, while Monee was less than 1% of the company.

Today, the gaming segment is only responsible for 11% of the business, whilst Shopee is responsible for 3/4 of Sea’s total revenue.

Most importantly, in just 5 years, Monee went from generating less than 1% of the revenue to 15%. An incredible performance that demonstrates the opportunity the financial services segment has.

This illustrates Sea’s exceptional transition from a small mobile video game company to a regional financial services and e-commerce behemoth!

Let’s remember that there are 265M people without a bank account in the region.

This is still year 1 for Monee!

Segment Profitability

Q4 2024 was the first time that Sea achieved EBIT profitability in all of its segments.

If we look at the segment EBIT graph above, one thing is clear.

Gaming is a cash cow for the company!

From 2016 to 2024, Garena generated $8.34B in EBIT, enabling Sea to aggressively invest in building out the other two divisions.

Profitability peaked in 2021, earning $2.5B in EBIT, an incredible EBIT margin of 58%. Today, Garena’s profitability has fallen 61% from its peak, but $963M EBIT is still a healthy 49.3% EBIT margin. This demonstrates Sea’s ability to control costs if business conditions change.

Moving to the big money guzzler, Shopee.

In 2021, Shopee caused an astonishing $2.8B EBIT loss for the company, an EBIT margin of negative 54%.

However, Shopee has become EBIT positive and is on a path to become a massive profitability machine!

In Q1 2025, the e-commerce segment made $195M in EBIT, an EBIT margin of 5.5%. There is a lot of room for the margin to expand, however, this will be a slow process as Shopee will prioritize market share and revenue growth over profitability, especially as the competition with TikTok Shop intensifies.

There is no need to push e-commerce margins higher when financial services are so profitable.

In 2022, with a negative EBIT margin of 22.7%, Monee lost the company $277M. However, by the next year, Sea had already earned $490M in EBIT from financial services.

In a single year, Monee went from being an unprofitable money-eating division with a negative 22.7% EBIT margin to a highly profitable division with a positive EBIT margin of 27.9%!

Unbelievable results.

Group Profitability

2023 was the first year Sea became profitable on the group level, generating $343M in EBIT and $151M in net income.

This was achieved despite Garena EBIT falling by $800M as Shopee reduced losses by $1.5B, whilst Monee grew EBIT by $767M.

In the graph above, we see how unbelievable the transformation truly was, from losing $1.7B in 2022 to generating $151m of net income in 2023.

This clearly demonstrates their ability to manage costs when a business environment changes!

The company prioritized market share and top-line growth, as the market was rewarding them for it with a high stock price. Once their stock price crashed, it became clear that they wouldn’t be able to raise additional capital to sustain such losses.

Thus, they implemented significant cost-cutting measures to become self-sustaining.

Sales and marketing expenses were reduced by $490M, administrative expenses by $303M, and R&D by $212M.

In total, 2023 operating expenses were cut by more than $1B, without sacrificing top-line growth, as Shopee and Monee still grew 20%+.

Sea has fostered a lot of consumer surplus that the company still hasn’t captured!

Consumer surplus refers to the value that Sea’s services create minus what customers pay for them. Sea provides fast and reliable delivery, a large selection of products, lots of discounts, entertaining games, and convenient financial services for less than what customers are willing to pay for them.

Sea forgoes profits today to increase market share and grow the ecosystem. The plan for the future is to increase prices, reduce promotions, and cut marketing budgets, without losing customers, in essence, capturing back some of that consumer surplus.

This means that there is a huge potential for the company to significantly expand profits and margins in the next decade.

We are seeing some of that play out in 2024, as EBIT and net income grew 93% and 195% respectively!

Margins

Growing profits mean that margins are improving as well.

I have placed gross, EBIT, and net income margins in the graph above, which illustrates a clear trendline of improving business fundamentals.

Gross margin has increased from 27.8% in 2019 to 46.2% in Q1 2025!

Unit economics are improving as Shopee is reaching scale in its logistics operations, reducing shipping costs per unit shipped. Additionally, the company is increasingly following Amazon’s playbook of growing higher-margin 3P seller services revenue, such as advertising. Simultaneously, Monee is starting to generate high-margin transaction fees and lending income.

Gross margin could reach 50% in the next few years.

Meanwhile, EBIT margin has jumped from -41% in 2019 to 9.4% in Q1 2025!

This was achieved thanks to Sea becoming a more efficient company, reducing its administrative overhead, and cutting its marketing budget. Marketing and administrative expenses were 25.6% of revenue in Q1 2025, down from 62% in 2019.

However, one expense category that is important to monitor is the provision for credit losses, which grew 74.3% in Q1 2025, reaching $282M, 36% of Monee’s revenue.

The provision grew 2.2 percentage points slower than the loan principal growth of 76.5%, a good sign. A credit loss provision growing faster than the loan principal would indicate deteriorating loan book quality.

I find it likely that the EBIT margin could reach 20% in the next 5-6 years as the company starts generating more highly profitable lending income.

Balance Sheet

Sea has a healthy and improving balance sheet.

In the graph above, we see that cash levels have improved significantly since 2023, sitting at $5.7B.

Meanwhile, long-term debt and leases have remained flat at around $4B.

Sea could pay off all its LT debt and leases and would have $1.7B left over!

3. Valuation

With a market cap of $98B, Sea currently trades for a TTM P/E of 116. This most certainly seems like a premium multiple, but we have to remember that it is a fast-growing company still early in its growth journey.

Wall Street analysts expect the company to grow revenue by 25% in 2025 and 71.7% over the next 3 years.

Moreover, analysts expect profitability to jump significantly, with EBIT set to triple this year and more than 6X by 2027.

Additionally, EPS is projected to increase by 418% this year and 795% by 2027.

Overall, while analysts are seeing the margin improvement story, I think they are underestimating the top-line potential.

Taking future growth into account 2027 P/E is 24.

Valuation Model

Let’s see what kind of returns investors could see if the company continues to execute.

I model Shopee growing with a 20% CAGR to reach $37B in revenue by 2030.

Monee has just touched the surface of its TAM, so I model it growing faster than Shopee, with a 35% CAGR to reach $14.3B.

Meanwhile, Garena is where there is huge potential for a surprise. As we discussed before, gaming is a volatile, hit-driven industry, making it extremely difficult to model. If the company creates new hits or comes out with new monetization methods (subscriptions), revenue could be multiples higher. For now, I am not certain, so I model it at $3.6B, slightly above today’s level, but remaining relatively flat compared to 2022.

With these assumptions total 2030 revenue would reach $55B, growing with a CAGR of 22%!

In Q1 2025 operating income margin was 9.4%. I find it likely that it will continue increasing, reaching 20% by 2030. Loans are extremely profitable, so they will be the key enabler of higher margins.

Assuming a 21% tax rate, we get to a net income of $8.7B, up 1,856% from 2024, or a CAGR of 64%!

If Sea delivers such a growth, I think it is entirely reasonable and plausible that it will trade between 40 and 50 P/E.

This is because SEA has a massive multi-decade TAM. Southeast Asian e-commerce and financial services development is a decade behind developed markets, and developed markets are not even done growing. Amazon has traded for elevated multiples for decades, so has SEA, and I don’t see a reason for that to reverse.

A P/E of 40-50 would result in a market cap between $348B to $435B.

If dilution doesn’t exceed 3% per year, Sea will trade for $494 to $618 per share.

That is an upside of 198-272%, a CAGR of 20-25%!

4. Conclusion

Sea Limited is a high-quality technology company dominating key growth vectors in a fast-growing and developing region.

Garena is a cash cow with 662M users that generate Sea close to a $1B in EBIT!

Shopee is an e-commerce, food delivery, and logistics disruptor, enabling over $100B of commerce!

Monee is a financial services leader on a path to serve over 100M customers.

As the region develops, 200M people are set to join the middle class. This new cohort will be hungry for services that Sea will be ready to deliver.

In the last 2 years, the company has demonstrated its ability to improve margins, and thanks to great execution and favorable trends, it could be set to become a profit-generating machine.

While today it trades for an elevated P/E of 116, the company is still early in its growth journey.

As the valuation model shows, with growth assumptions that I find reasonable, the company could return between 198-272% to patient investors.

Overall, I find Sea to be a great addition to a growth-minded and patient long-term investor’s portfolio!

Thank you for reading Global Equity Briefing!

Global Equity Briefing is an investing newsletter with a focus on analysing global companies. I have written highly detailed Deep Dives on Nu Bank, Ferrari, Palantir, Grab, Celsius, Mercado Libre and Hello Fresh!

Additionally, I have written Investment Cases on Meta, Amazon and Google! and comparisons of Visa vs Mastercard and Eli Lilly vs Novo Nordisk!

My goal for 2025 is to write around 4-6 articles per month!

Subscribe to get all my articles as soon as they are released!

Support my work by becoming a paid subscriber!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

It might be my phone but I can't see any table in the post

Sorry. The analysis is great until you arrive at making crazy projections and a 50 times pe target. That's insane haha