How did Nu get 114M customers?

Nu. Serving the Underserved! Equity Research! Part 1/3

We are living in the golden age of banking. It has never been faster and cheaper, to receive and spend money. Bank accounts are affordable and easy to use. Rather than taking 3 days, most transactions take mere hours. Credit cards and debit cards are accepted basically everywhere.

Let’s not forget how Apple Pay revolutionized mobile payments, enabling 100s of millions of people to transact using their iPhones.

However, this hasn’t always been the case everywhere!

In 2019, there were over 200 million unbanked people in Latin America, around 45% of the adult population!

The majority of these people are low-income and legacy banks simply didn’t see the profit potential in servicing them. They were satisfied with high profits and had zero intentions of doing anything to reduce the unbanked population.

This is the environment in which Nu Bank was born!

“Our mission is to fight complexity to empower people in their daily lives by providing accessible, affordable, and easy-to-use financial products.” Nu Holdings mission statement 20F 2023

Nu wanted to empower people, and they empowered 114 million of them!

By 2023, in large part thanks to Nu, the number of unbanked people had fallen to 91 million, 21% of the adult population!

In this 3-part Deep Dive, I will tell you why I think Nu is one of the most promising long-term investments in the market!

In Part 1, I will tell you their origin story, and explain Nu’s business model.

Part 2 will tackle challenges and competition.

I will close out this Deep Dive in Part 3 by taking a look at their opportunities, financials, and valuation!

Let’s begin!

1. The Story of Nu

2. Business Model

3. Competitive Advantage

4. Parts 2 and 3

1. The Story of Nu

Nu was founded in 2013 in Sao Paulo, Brazil, by Colombian venture capital executive David Velez.

David moved to the US in 2004 to attend Stanford University and after working for various large investment banks, he ended up at possibly the world’s most famous venture capital firm, Sequoia Capital.

In 2012, Sequoia was looking to expand in emerging markets and picked David to lead their Brazilian office. This is how David recalled the experience years later.

“In mid-2012, I entered the branch of one of Brazil’s largest banks to open my first Brazilian bank account. As I approached the first bulletproof door that was flanked by armed security guards, I sensed this was not going to be easy. During the following four months I spent long hours in queues, calling the call center, and returning to the bank branch with an increasing number of documents, until finally a bank account that would charge hundreds of reais per year in fees was approved in my name. The entire experience was incredibly frustrating. As I tried to reconcile this experience with the immense profitability of Brazilian banks and the low penetration of banking in this country, I realized that this was possibly the entrepreneurship challenge I had been looking for..” The Spark Of Our Foundation: a letter from our founders. Nu Holdings. 9. December 2021.

Motivated by this personal experience, just a year after moving to Brazil, David quit Sequoia Capital to create Nu Bank.

Latin America

To understand Nu Bank’s story fully, we must understand the region in which it operates.

Latin America is generally considered to include all the Spanish and Portuguese-speaking countries of South and North America. With a population of 675M it is a large, natural resource-rich but economically underdeveloped region.

Latin American economies suffer from extreme income inequalities. The region is dominated by large and powerful politically connected families and businesses. These businesses dominate whole industries in a corrupt and inefficient way, leading to high prices and bad service.

This is especially notable in the banking sector.

For instance, in Brazil, there are around 155 banks for a population of 211M. That means that there are 1.36M people per bank. In Colombia, there are 45 banks for 52M people, so 1.15M people per bank. In Mexico, this ratio is 2.70.

Meanwhile, in the US, there are 4,000 banks for a population of 340M, so 85K people per bank. In the EU this ratio is 91K.

The difference is just night and day. In the US and EU, there are 16 times more banks per person!

This creates higher competition. Higher competition leads to lower prices and better service.

Brazilian banks are some of the most profitable in the world! In 2021, their Net Income Margin (NIM) was 4.42%, this is in stark contrast to US and EU banks whose NIM is between 1-2%.

And no, this is not because the Brazilian economy is strong. In fact, the Brazilian economy has struggled in recent years.

High concentration, low competition, exorbitant fees, and bad service are some of the main causes why, in Latin America, there are 91M people without a bank account!

Servicing the Underserved

Since Nu’s founding, they have been obsessively focused on reducing the underbanked population. For millions of customers, Nu’s bank account has been their first bank account ever.

Between 2018 and 2023, Nu issued 21M Brazilians their first-ever credit card!

Latin America unfortunately, suffers from a high level of informal economy. Millions of people work without contracts and receive salary in cash. According to Brazilian labor statistics around 39% of all employees engage in such work. In Mexico and Colombia, the statistics are sadly similar.

Historically, these people didn’t have access to financial services. Nu has changed that by bringing millions of underserved people into the economy.

Even small loans are impossible without a bank account. By providing simple services, Nu is improving the lives of millions of people that have been neglected and underserved for decades.

2. Business Model

While other banks have thousands of inefficient, slow, and bureaucratic branches, Nu serves its customers through its best-in-class mobile banking app.

Nu is a low cost, digital-only, mobile-first provider of financial services!

The company has built a business model that enables them to acquire and service millions of customers at a cost that legacy banks could only dream of.

Let’s take a look.

Technology

While we live in 2025, many banks, especially in emerging markets, still live in the 1980s. Opening a bank account is a long and tedious process that could even take weeks. Getting a loan, credit card or an investment account is no different.

Well, Nu doesn’t have thousands of bank tellers and customer service employees that can spend hours going through paperwork.

Not having bank branches is of course a limitation, but this limitation has forced Nu to adopt smart and clever technological solutions to problems.

Thus, Nu built a technology-first platform that collects, stores, and analyzes customer data quickly and efficiently, speeding up decision making.

This fully cloud-based technology banking platform is called NuCore.

NuCore manages all customer data and allows for real-time monitoring of financial transactions across the entire ecosystem. Having all the data easily accessible in one place enables increased automation of important processes such as compliance, reporting, fraud prevention, credit analysis, and document checks.

NuCore reduces the need for human intervention in routine processes!

Humans often make mistakes, while an automated rules-based system doesn’t.

Most importantly, Nu is a cloud first, technology company!

AWS is their primary technology partner. Scalability is key for a quickly expanding fintech such as Nu. Luckily, AWS is perfect to empower the company to securely and affordably store data and manage their computing needs.

One of Brazil’s biggest banks, Itaú Unibanco, was born in 2008 through the merger of Itaú and Unibanco. Additionally, each bank did many mergers and acquisitions before that.

Most legacy banks are decades and some even hundreds of years old. They are the result of dozens of such mergers and acquisitions that force them to operate a patchwork of different systems.

Nu had the opportunity to build its technology stack from zero, enabling them to build in a way that fits the year we live in.

And now Nu is the best prepared financial institutions in the region for AI deployment. Nu is already using AI in customer support, process automation, and in credit and risk analysis.

Nu is not a financial services company that is good with technology, Nu is a technology company that happens to provide financial services!

Products

Nu offers a full suite of services to its customers.

Traditional Banking

Customers can use Nu’s basic bank account NuConta to receive salary and make payments.

One of their most popular and flagship products is an easy-to-use low-cost credit card.

In a stark contrast to legacy banks, Nu doesn’t charge a monthly or yearly credit card fee. The company makes money by charging interest on the balance, which is often lower than what other banks offer. The app is fully integrated with the credit card, allowing to easily see and adjust credit limits, due dates and switch to instalment payments.

Additionally, they offer a premium Ultraviolet Credit Card, that’s targeted towards affluent customers. It comes with a $R49 monthly fee and higher credit limits. The card has various perks such as special offers from partner merchants, airport lounge access, and travel insurance.

Additionally, customers can deposit cash on their Nu accounts through thousands of retail partners. Enabling people engaged in the informal economy to simply and securely deposit their income to pay bills, taxes, and more.

Investments and Savings

Apart from a savings account, Nu enables its customers to participate in capital markets with low-cost access to popular investment products. Bonds, stocks, ETFs, and Crypto can be purchased for low fees, directly in the app.

Loans

In addition to credit card loans, Nu offers secured and unsecured loans. Customers can create a loan application right in the app and get it confirmed within hours.

Additionally, a popular loan is the payroll deductible loan. Government employees, pensioners, and others who qualify can secure a loan by their salary, with loan repayments automatically withheld from each salary. As these are lower risk, Nu can offer reduced interest rates.

Furthermore, customers can use their investments as collateral to get a loan. This enables them to access short term financing without having to sell the assets, avoiding a taxable event.

Insurance

Depending on the jurisdiction, Nu bank offers car insurance, life insurance, mobile insurance, and others right in their app.

In these insurance transactions Nu acts as an agent, not as the primary. This means that the company doesn’t hold the insurance risk on its balance sheet, that risk is held by their reinsurance partners. The Swiss insurance giant, Chubb, is their primary partner. In return for selling and servicing insurance, Nu takes a commission.

NuPay

NuPay is their payments processing business.

Select retail partners offer a NuPay option at the checkout. This enables customers to pay for purchases directly from their Nu bank account. No need for debit and credit cards. Customers who use NuPay benefit from a simple and fast checkout process, and higher credit limits. Launched in 2022, the service is available in over 160 e-commerce stores. With local Uber competitors, IFood and 99 being the most known companies. Merchants pay a fee for each transaction.

So far, Nu hasn’t signed deals with large global players such as Netflix, Amazon, Uber or Mercado Libre, but considering Nu’s scale of 114M customers, I find it likely that many of these merchants will want to partner with Nu to tap into this customer base.

Low Costs

Time is money. And nowhere is this famous saying more applicable than in banking. The larger the bureaucracy, the higher the administration costs, leading to a lower velocity of money.

As a financial institution, it is to Nu’s benefit to lower bureaucracy, reduce costs, and increase the velocity of money.

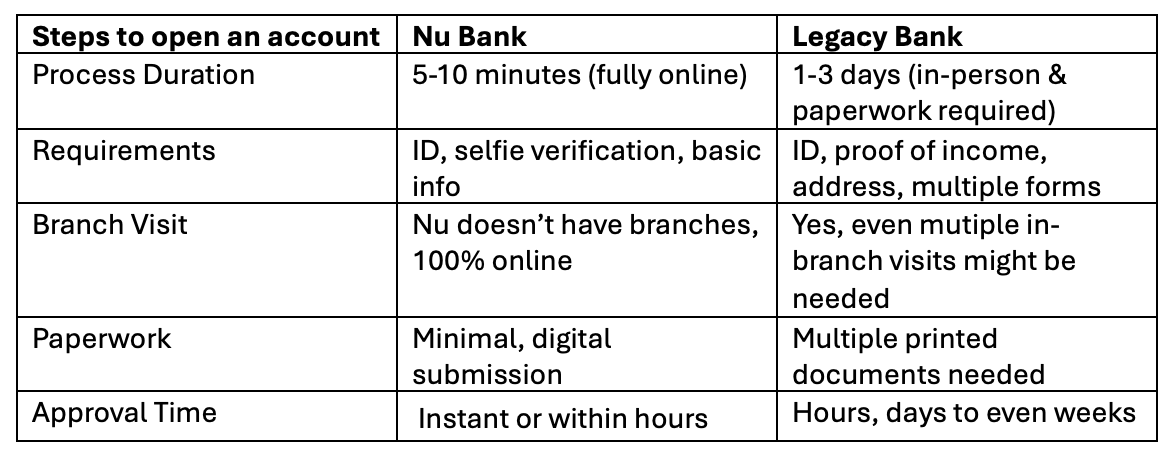

Compared to most legacy banks, opening a bank account, getting a loan or buying an insurance is a much simpler process!

Here is a simplified overview of an account opening process:

Understandably, Nu’s process is not only preferred by customers, but also much cheaper for the company.

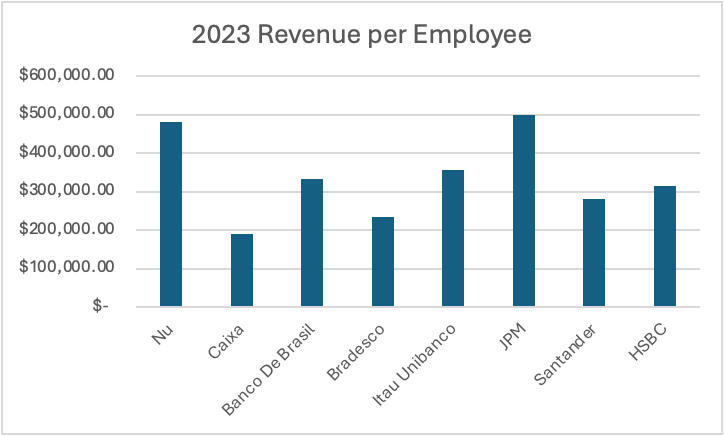

Nu had 7,686 employees on 31. December of 2023. This is an order of magnitude less than legacy banks with a similar number of employees.

In 2023, Nu had 94 million customers, which means that a single employee was able to service over 12 thousand customers. In the graph above, we can see customers per employee of a few select banks and the difference is stark.

Of course, the number of customers is far from being the only metric to measure a bank’s success. These financial institutions manage billions from a few very large customers, whilst Nu mostly has millions of small accounts.

In the above chart, I have placed 2023 revenue per employee, and here we see that the difference is not as stark, however, Nu’s position is still incredibly strong. In 2023, Nu generated $482K per employee, less than the $498K of JPM, but more than $355K of Itau Unibanco and $334 of Banco De Brasil.

As Nu continues its regional expansion and improves its services offering, revenue per employee will only increase.

Customer Statistics

Nu closed 2024 with 114.3 million customers, an increase of 20 million or 21.6%.

In the graph above you can easily see how explosive this growth has been. In 2019, Nu grew by 235%, from 6 to 20M customers.

Since 2017, Nu has grown with a 68% CAGR!

101.8M of these customers are in Brazil, an estimated 58% of Brazil’s adult population use Nu, which is absolutely astonishing. There is still room to grow, and I estimate Nu could reach around 70% in the long term.

Meanwhile, with 10M customers in Mexico, Nu is quickly gaining ground in this 131M people strong Latin American market. Customers grew by 92% Y/Y and just 5 years after launching there, already 10.6% of the adult population use Nu.

Lastly, Nu has 2.4M customers in Colombia, up a mindboggling 167% from the prior year. In 4 years, Nu has attracted 5.8% of the adult population.

Both Colombia and Mexico are growing faster than Brazil did!

This indicates that the company has built a great platform that customers like, and their reputation is spreading quickly. Additionally, Nu has developed a clear system of customer acquisition that now can be “copy and pasted” to new markets.

How Nu Makes Money?

The two primary ways by which banks make money are giving loans and charging various fees.

Loans

To fund loans, banks must attract customer deposits. As of Q4 2024, Nu had attracted $28.9B in deposits from its 114M customers.

In return for keeping their money with Nu rather than another bank, customers are paid interest. In 2024, Nu paid $2.8B in interest to depositors and other lenders. This might seem high for some of you, but let’s remember that the Brazilian Central Bank’s interest rate now sits at 13.25%, compared to the 4.33% US Fed rate and 2.9% ECB eurozone rate.

$11.2B from deposits was lent out to customers, meaning Nu’s loan to deposit ratio is 39%. $6.3B are kept in cash to satisfy and some of the remaining funds are invested in interest-bearing securities such as bonds and treasuries. In total, Nu earned $9.6B in interest income. This means that Nu generated $6.8B in net interest income. (NII) ($9.6B-$2.8B)

Banks measure how effective they are at generating interest income by calculating net interest margin. Net interest margin is calculated by dividing NII of $ 6.8B by the average earning assets of around $36.1B, and we got a NIM of 18.85%.

The unfortunate reality is that not all borrowers pay back their loans. Regulators mandate that banks estimate the amount of bad loans and make a provision for loan losses. This provision is not recognized as an expense, rather it is recognized as a reduction in revenue.

In 2024, Nu made a $3.2B provision for loan losses!

Fees

In 2024, Nu made $1.9B in fee income. This includes all the fees the company charges to its customers and partners.

Every time a credit or debit card is used, depending on the card, the merchant is charged between 1 to 4%. In such a scenario, the issuing bank might keep 0.5 to 1%.

If NuPay is used, the fees might be different. This is why I believe Nu ultimately has very big ambitions for NuPay. As they keep all the transaction fees, they can offer better terms to the merchant than a payment processor might.

All other commission fees are also recorded here, such as insurance fees, late fees, credit card fees, transaction fees, investment fees and more.

3. Competitive Advantage

In my opinion, Nu Bank has 5 key competitive advantages, a low-cost structure, technology-first thinking, strong ecosystem, first mover advantage, and strong customer engagement. Let’s look at each.

Low-cost structure allows Nu to fulfil basic customer needs cheaper. Allowing the company to offer services for lower prices, at comparable margins to legacy banks. Nu said that in 2024 it cost them $0.80 per month to service one customer. Legacy financial institutions incur costs of $5-10. This low-cost structure leaves more capital for expansion and product development.

Technology-first thinking empowers Nu to build their services from the ground up, fully taking into account the customer experience. Whilst, legacy banks think not “what our customers need, but what we can provide”. Nu is not burdened by legacy system limitations. It can easily and quickly integrate new products into its app, while legacy banks might take years even for a simple update.

Strong ecosystem of partners enables the company to offer an unparalleled services offering, all in one app. No other legacy bank has such a comprehensive and easy to use mobile application. Nu started with just a credit card and now has a full portfolio.

First mover advantage in digital financial services has not only positioned Nu well to compete with legacy banks, but also with other fintechs. The many millions of unbanked people Nu has onboarded, are less likely to switch to an alternative low-cost provider.

Strong customer engagement has allowed the company to gain a cult following. The bank has a reputation for great and affordable services, enabling it to gain millions of new users at unprecedented speeds. No other bank could go into Mexico and gain 10 million customers in just 5 years.

4. Parts 2 and 3

Part 2 is coming out next week!

In Part 2 I will tell you how Nu stacks up against its competitors.

Additionally, you will learn what risks the company must deal with! (Hint FX and regulations)

Part 3 is coming out a week after Part 2!

The conclusion of this report will explain Nu’s finances, and valuation!

Moreover, we will look at the opportunities this fintech can execute on to become a generational investment!

Thank you for reading Global Equity Briefing!

Global Equity Briefing is an investing newsletter with a focus on analysing global companies. I have written highly detailed Deep Dives on Ferrari, Palantir, Grab, Celsius, Mercado Libre and Hello Fresh!

Additionally, i have written Investment Cases on Amazon and Google! and comparisons of Visa vs Mastercard and Eli Lilly vs Novo Nordisk!

My goal for 2025 is to write 1 article a week!

Subscribe to get all my articles as soon as they are released!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

Thank you for this write-up.

"$20.7B from deposits was lent out to customers with some of the remainder being invested in interest-bearing securities such as bonds and treasuries."

https://api.mziq.com/mzfilemanager/v2/d/59a081d2-0d63-4bb5-b786-4c07ae26bc74/abb5b993-fc6b-c86d-4a75-fc2cb6236dfc?origin=1

Page 33, their interest earning portfolio is $11.2B and their LDR is 39%.

This is a timely article considering the selloff. Great time to build conviction to add. Looking forward to the other articles.