Fast-growing Fintech set to grow earnings by 363%!

Sofi Investment Case!

JPMorgan Chase, the largest bank in the US, has over 5,000 retail bank branches.

Wells Fargo has over 4,000.

Bank of America has over 3,000.

Meanwhile…..Sofi has 0 bank branches!

The old-style traditional way of doing banking is over.

A grandmother in the 1990s had to make an appointment a week in advance and physically go to the bank to do even the smallest of changes.

Luckily, her granddaughter doesn’t have to go to the bank anymore.

She can open an account, apply for a loan, refinance her student debt, get a mortgage, chat with a customer representative, and invest her savings by simply using the SoFi app on her phone without leaving the house.

Sofi’s entirely digital platform resonates strongly with young people, enabling the company to become a neo-bank leader, especially popular with high-income recent university graduates.

In just 5 years, Sofi 10X’ed their members, from 1M to 10M!

Nowadays, Sofi is constantly releasing new products, increasing cross-sales, and ramping up profitability, with aspirations to become a “One-Stop-Shop” for all financial needs!

In this Sofi Investment Case report, I will tell you why I find Sofi to be an incredibly compelling long-term investment opportunity.

The Sofi Bull Case is driven by student loan refinancing, lending, “One-Stop-Shop” innovation, the Loan Platform Business, and their SaaS “AWS of Banking” software business.

Let’s look at the offering.

1. Student Loan Refinancing

2. Lending

3. One-Stop-Shop Innovation

4. Loan Platform Business

5. AWS of Banking

6. Valuation

7. Conclusion

1. Student Loan Refinancing

The US has become world-famous for the quality of its universities, with prestigious universities such as Harvard, Princeton, MIT, Yale, and others attracting hundreds of thousands of students. Many of the world’s most famous and powerful people in business, government, and science have studied there.

While many applaud these institutions for their academic rigor, others criticize them for abusing their position as gatekeepers of high-income employment to enrich themselves and their faculty.

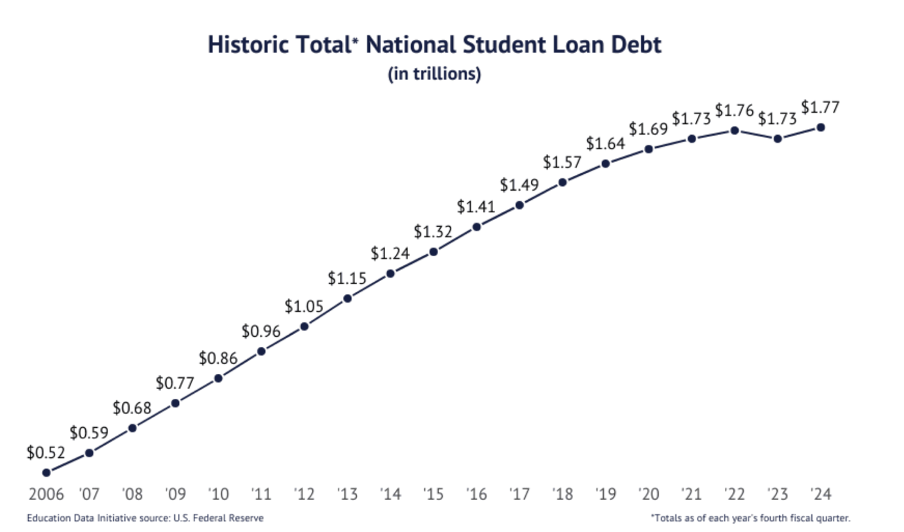

In the past 2 decades, the average tuition fee has risen by 60% from $9,204 per year to $14,688!

This has created a student loan epidemic of gigantic proportions!

As of 2024, the total US student loan debt balance stands at $1.77T!

92.4% of the student loan balance is held by the federal government, with the remaining 7.6% or $135B managed by financial institutions. This presents Sofi and others with a huge opportunity to refinance these loans.

Additionally, in 2023, 9.3M student loans were issued for a total balance of $64.7B. This makes student loans the 3rd largest consumer debt category behind mortgages and car loans.

This is why student loans have historically been Sofi’s bread and butter. They constitute an extremely large market with lots of borrowers looking to save money by refinancing them.

People with higher incomes have lower risk profiles, but often they keep paying the same loan they applied for on the first day of school.

By getting a new lower-interest-rate loan that better matches their risk profile and using those funds to repay the old loan (refinancing), people can save hundreds of dollars a month.

Additionally, by waiving common banking fees such as application, origination, processing, and others, SoFi attracts many financially literate people looking to save money.

Moreover, one of the most popular ways to reduce the monthly payment is by extending the loan term. By offering this feature, Sofi aims to attract people early in their careers who are willing to trade savings today for higher payments in the future. This group is often referred to as HENRYs (High Earners, Not Rich Yet).

Sofi has earned a reputation for being a low-cost and easy-to-use bank to refinance student loans!

While to earn this reputation, Sofi had to forgo a lot of earnings and work for many years, today they are the clear student refinancing leader, originating around 60% of the student loan refinancings in 2023.

An often-overlooked aspect of student loans is their function as a gateway product and a low-cost customer acquisition tool.

By offering affordable student loan options, Sofi acquires customers early in their career journey. As time goes by, these customers will significantly increase their income by getting promoted, switching jobs, or collecting an inheritance.

These customers will likely need other financial services in the future, and now that they are a Sofi customer, they are less likely to seek these services elsewhere.

Sofi student loan originations volumes peaked in 2019 at $6.7B, but have since stagnated.

This is in no way a fault of Sofi, as to support the economy during the pandemic, Federal student loan repayments were paused, and no extra interest was accrued during this pause.

Understandably, student loan refinancing collapsed, as most people didn’t see the point of paying loans if there were no penalties for not doing so.

However, in October 2023, the pause was ended, and recently, in May 2025, the Trump administration announced the resumption of collections of defaulted loans.

The resumption of payments already led to a 44% jump in student loan originations in 2024 and a 59% in Q1 2025.

There is a tsunami of student loan originations coming, and Sofi is uniquely positioned to surf it!

2. Lending

Student loans are just one part of the lending business. Sofi also offers home loans and personal loans.

While student loan originations have struggled, personal loan originations have exploded by 433% to $19.9B in the last 5 years and 69% in Q1 2025.

Additionally, home loan originations have more than doubled to $2B, growing 54% in Q1 2025.

Lending can be extremely profitable for banks as it generates stable income that costs relatively little to service.

Sofi raises capital from investors, creditors, and clients through bank deposits and lends that capital to customers. In this process, Sofi earns a spread, as ideally, they earn much more from the loans than they pay for capital. This spread is called net interest income.

The net interest income of the lending segment has grown by 300% to $1.3B!

Another key measurement is net interest margin (NIM), which measures how much net interest income a bank generates from its interest-earning assets.

NIM for the entire company was 6.01% in Q1 2025, a strong result compared to other banks whose NIM stands in the 3-4% range.

Sofi can achieve strong loan profitability because they have a high-quality clientele with higher average incomes (HENRYs), who are less likely to default, yet are hungry for loans.

Additionally, Sofi can raise cheaper capital from its 11M large customer base through deposits than other fintechs.

Sofi is in a strong position to continue earning high NIM interest income from its growing customer base!

3. One-Stop-Shop Innovation

Sofi’s goal to become a one-stop shop for all customer financial needs is at the core of their business model.

“We’ve proven that we can achieve strong returns and durable growth in a full cycle of market conditions through our relentless focus on innovation. We built personalized financial solutions to meet the changing needs of our members, many of whom are deepening their relationship with us. In 2024, 30% of new products were opened by existing SoFi members, and nearly 40% of new members opened a second product in the first 30 days. Our one-stop-shop model is working for our members because it was built for them.” Anthony Noto, Sofi CEO, Sofi 2024 Annual Report

The business model is based on what the company calls the “Financial Services Productivity Loop”.

First, Sofi gains members by offering a compelling core product. For a large share of customers, it is student loan refinancing as discussed previously. For others, it might be a high-yield savings account, a checking account, or a credit card.

Next, Sofi cross sells other lending or financial services products. This is really where the productivity loop begins. Student lending customers are offered home loans, credit cards, insurance, and investing products. Meanwhile, customers with a checking account are offered student loan refinancing, etc.

Sofi says that 40% of new customers start using a second product within 30 days!

Then, the company drives user engagement and enhances customer experience with an integrated and easy-to-use mobile app. Additionally, Sofi offers various educational, AI-supported, and data-driven financial tools that help with budgeting, credit score monitoring, and more.

Finally, to turbocharge this productivity loop even more, Sofi has a subscription-based loyalty program called Sofi Plus.

Sofi Plus members receive a slightly higher interest rate on their deposits, extra cashbacks on eligible purchases, interest rate discounts, 1% match on investment deposits, and more perks.

One can become a member by paying $10 a month, or for free if they receive a salary in a Sofi account.

Products have consistently grown at a higher clip than members, and today the average member uses around 1.5 products.

Overall, this model lowers customer acquisition costs and increases customer lifetime value!

Many of the extra services customers are cross-sold are less risky and more profitable for the company, as they generate fee income.

When Sofi sells insurance, they act as an agent, not a principal. This means that the company is not liable for paying out the insurance, they just collect a processing and origination fee, with their insurance partner handling the rest.

Furthermore, when a customer uses a Sofi debit card, Sofi gets a cut from the fee the merchant pays for processing the transaction.

As Sofi releases new products, the productivity loop will only get stronger, enabling the company to retain an ever-increasing customer wallet share!

4. Loan Platform Business

Sofi has a problem that many fintechs would wish to have, they have more loan applications than they know what to do with. Other fintechs or financial institutions would lower their lending standards to finance these applications, however, Sofi has very strict risk management policies, and they are not willing to do so.

Nevertheless, Sofi has figured out multiple ways to monetize these requests, without incurring higher risk, whilst simultaneously increasing margins!

Here is how it works:

First, customers fill out a loan application using the SoFi app. After Sofi analyzes applications, it determines which loans will be the most profitable (high income, low probability of default) and keeps them on its balance sheet. Sofi is responsible for losses in the case of defaults.

If the risk profile is a little bit worse, but still acceptable, they originate these loans and then sell them to investors through loan sales or securitizations. Sofi sells loans for a few % more than the principal (6.2% in Q1 2025), generating instant cash flow. Investors collect monthly payments and are responsible for losses in the case of defaults.

But that is not all, Sofi has come out with a new way to monetize loans, called Loan Platform Business (LPB)!

The way LPB works is that Sofi partners with financial institutions and originates loans on their behalf according to a set of criteria. The partner is fully responsible for loan financing and losses.

Sofi collects loan origination, referral, and servicing fees. Essentially, LPB enables the company to earn a high-margin, zero-risk income without spending a dollar of its own capital.

Crucially, LPB loans are managed by Sofi in their own app, enabling Sofi to retain the customer relationship and management, most of the time, customers have no idea that Sofi is not the one issuing the loan.

If a loan application doesn’t meet Sofi’s or LPB partner criteria, the company refers the customer to other partner lenders, earning a referral fee if the customer uses them. In 2024, Sofi made $52M in LPB referral income.

Furthermore, Sofi generated an additional $89.5M in LPB fee income from originating $2.1B in loans, that is a take rate of 4.23%!

Let’s remember that because Sofi doesn’t finance these loans or hold any default risks, the fee income is extremely high margin, likely at 60-80% EBITDA.

As of Q1 2025, Sofi has $8B in new LPB financing commitments from partners!

If the take rate remains the same, Sofi will generate $338M in revenue. At a 70% EBITDA margin, LPB would create $237M in EBITDA.

That would be 12.8% of Sofi’s entire 2024 revenue and 54% of EBITDA!

In Q1 2025, Sofi made $73M in LPB fee income from originating $1.56B, a take rate of 4.68%!

This is a 10% increase in take rate, indicating that partners are satisfied with loan profitability and are not asking for discounts to compensate for higher defaults.

If the origination pace remains the same, Sofi will exhaust the $8B in LPB commitments in 5 quarters.

LPB is set to become a huge profitability driver for Sofi!

5. AWS Of Banking

Amazon revolutionized the internet with Amazon Web Services, its cloud infrastructure and computing platform.

To create and run a digital business, millions of dollars in start-up capital and a large team of developers are no longer necessary. A simple idea can be turned into a business by a one-person with a few hundred dollars and a credit card.

Whilst AWS is the backbone of the internet, Sofi is building a Technology Platform that could become the backbone of the banking and financial services industries!

According to Mordor Intelligence, the Global Banking-as-a-Service (BaaS) software market is projected to grow with a 26.6% CAGR to reach $21.9B by 2030!

This is a huge opportunity for Sofi to earn a high-margin, recurring software revenue, reducing reliance on core banking services such as loans and credit cards.

Sofi’s Technology Platform provides foundational infrastructure services to the broader financial services industry, offering modular, scalable, cloud-based solutions to banks, fintechs, and others.

This division is largely the result of two acquisitions. In 2020, the company acquired Galileo, a payments processing platform, for $1.2B, whilst Technisys, a cloud-based banking platform, was acquired a year later for $1.1B.

For fintechs looking to expand their offerings, the platform provides core banking services such as bank account creation and management, ledger functionality, customer onboarding, identification, and more. Notable clients include Dave and Monzo.

If Fintechs desire to offer cards to clients, Sofi offers virtual and physical card issuing and management tools. Additionally, the platform powers branded card programs, enabling nonfinancial companies to manage loyalty programs, such as Wyndham Hotels.

Meanwhile, smaller regional banks don’t have the resources to build sophisticated tech systems in-house in the same way as giants such as JPMorgan and Wells Fargo. For these clients, Sofi’s technology platform helps modernize their risk, fraud, lending, and customer service infrastructure. Notable clients include Keystone Bank, Metropolitan Commercial Bank, and Bancorp.

Most crucially, Sofi is the most important client of the Technology Platform!

One of the biggest advantages Sofi has over the established banks is being a blank slate. Sofi is building its banking and technology stack from the ground up, so they don’t have to bother with integrating various patchworks of old banking systems.

JP Morgan and all other major and regional banks are the result of hundreds of acquisitions over the decades, with some of them today still using software from the 1970s.

Upgrading and integrating these systems will take years and cost billions of dollars, so many banks are forced to operate on archaic systems.

Running a bank on these systems is expensive, time-consuming, and hinders their ability to deliver a great customer experience.

This gives Sofi a cost and customer experience advantage over many legacy banks!

The main goal of the Technology Platform is to build the best products for Sofi.

While the Technology platform has potential, Sofi hasn’t been able to really capitalize on it, as the growth has been weak.

As of Q1 2025, the platform has 158M accounts, a 6% fall from the 168M it had at the end of 2024. The company said that they lost 10M accounts, due to a large customer moving their banking core systems in-house. Since then, it has been reported that it was the US Fintech Chime.

Understandably, this poor performance has been reflected in the finances of this segment.

Since 2022, when the last acquisition was closed, the revenue of the Technology Platform has grown only by 25%, a CAGR of 12%. This is significantly below investor expectations and internal goals.

For Sofi stock to get a SaaS-like multiple to this part of the company, growth must accelerate.

6. Valuation

Sofi has a market cap of $14.8B, and SOFI 0.00%↑ is up 94% in the past year. Despite this strong performance, the stock is still down 48% from its all-time high in 2021.

This underperformance was largely caused by collapsing student loan originations and changing market dynamics in a high-interest rate environment.

Nevertheless, today, student loan refinancing is accelerating, personal loan originations are exploding, whilst the loan platform business is on a path to completely change Sofi’s profitability profile.

Currently, the company trades for a TTM P/E of 32, a reasonable multiple for a fast-growing company that ramping up profitability.

Wall Street analysts expect Sofi to grow revenue by 23.6% in 2025 and 71% over the next 3 years. In my opinion, analysts are underestimating the flywheel effect of the “financial services productivity loop”. I wouldn’t be surprised if Sofi doubled the revenue in the next 3 years.

In terms of profitability, analysts expect the company to grow EBIT by 81.8% in 2025 and a whopping 362.6% over the next 3 years!

This is a direct result of high-margin LPB referral and origination fee revenue. There is some potential for the margin to be slightly higher, but analysts have largely taken the improving business dynamics into account.

However, in 2024, EPS was artificially higher due to the recognition of a one-time tax benefit of $265M. That is the main reason why EPS is set to decline in 2025 and grow much slower over the next 3 years than revenue and EBIT. Without this benefit, EPS growth would be in line with EBIT growth.

Valuation Model

I built a valuation model to estimate potential future upside.

With a 20% CAGR, 2030 revenue would reach $8B, up 203% from 2024 levels!

Growth in LPB and other fee-based businesses is allowing Sofi to reach higher margins, so I model a 25% operating margin by 2030.

This would allow the operating profit to grow with a 43% CAGR to reach $2B.

However, net income will probably grow more slowly due to being artificially high in 2024 (the tax benefit discussed earlier) and higher taxes in the future.

I model net income growing with a CAGR of 20.9% to $1.56B by 2030!

In Q1 2025, Sofi share count grew by 4.5% Y/Y, and historically, the company has been diluting shareholders by more than 10% per year. Yet, considering they are a profitable enterprise now, I think the dilution won’t be as high anymore, so I model a 4% per year dilution.

With a P/E of 30, we would result in a market cap of $46.8B and a share price of $33.78.

So, this model identifies a 154% upside to today’s share price of $13.30!

7. Conclusion

The banking industry is transitioning into a modern, digital, and mobile-first industry. Sofi, with its tech innovation stemming from its “AWS of banking” Technology Platform, is uniquely positioned to benefit from consumers demanding easy-to-use financial services.

Furthermore, the business is experiencing many beneficial trends:

Student loan refinancing is roaring back from the dead!

Personal and home loan originations grew 69% and 54% in Q1 2025!

Loan Platform Business is delivering high-margin, zero-risk, fee income!

Financial Services Productivity Loop is working, with 30% of new products opened by existing users!

Most importantly, the customers that Sofi acquired in prior years through student loan refinancings are growing into their professions, earning higher salaries and using more of Sofi’s products.

Sofi’s one-stop-shop strategy has positioned the company to grow customer wallet share through strong product innovation and great services.

Lastly, the valuation model shows that Sofi is reasonably priced considering its growth prospects.

A 20% revenue CAGR and improving margins could deliver 154% share price gains by 2030!

I find these assumptions to be reasonable, leaving room for outperformance if the growth is faster, profits are higher or the market assigns a higher multiple.

Thank you for reading Global Equity Briefing!

Global Equity Briefing is an investing newsletter with a focus on analysing global companies. I have written highly detailed Deep Dives on Nu Bank, Ferrari, Palantir, Grab, Celsius, Mercado Libre and Hello Fresh!

Additionally, I have written Investment Cases on Meta, Amazon and Google! and comparisons of Visa vs Mastercard and Eli Lilly vs Novo Nordisk!

My goal for 2025 is to write around 4-6 articles per month!

Subscribe to get all my articles as soon as they are released!

Support my work by becoming a paid subscriber!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the "Global Equity Briefing" newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the "Global Equity Briefing" report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

Golden Pacific Bank has 3 branches. So I guess SOFI technically has 3 branches :)

Great break down, thanks!