Klarna: 5x Opportunity or a Subprime Lender?

Leading BNPL Fintech building a Digital Banking business!

The global financial services industry is currently undergoing a period of rapid change, driven by the intersection of AI, changing consumer preferences, and the rise of digital-first banking.

At the center of this change is Klarna!

Everyone loves shopping, but nobody loves paying, especially Gen Z.

What if you could buy now, but pay later?

If that sounds appealing to you, you are not alone, as Klarna has attracted over 188M customers to its BNPL business.

The company’s primary mission is to provide a fairer and more transparent alternative to traditional credit cards, which often trap consumers in cycles of high-interest debt.

By using advanced technology to lower costs and improve service, Klarna is attempting to rebuild the retail banking experience from the ground up for a new generation of shoppers.

However, the market has grown increasingly pessimistic in its BNPL business, with shares collapsing 69% since the IPO!

The narrative has shifted, with a lot of bears making fun of people paying for their Uber Eats with Klarna and calling the company a subprime lender.

What they miss is that Klarna is transforming into a fully fledged banking fintech!

In this Klarna Investment Thesis report, I will explain its business model, shift to digital banking, finances, growth opportunities, and conclude with an analysis of the valuation and a 2030 valuation model.

Let’s begin.

1. Business Model

2. Finances

3. Growth Opportunity

4. Valuation

5. Valuation Model

6. Conclusion

1. Business Model

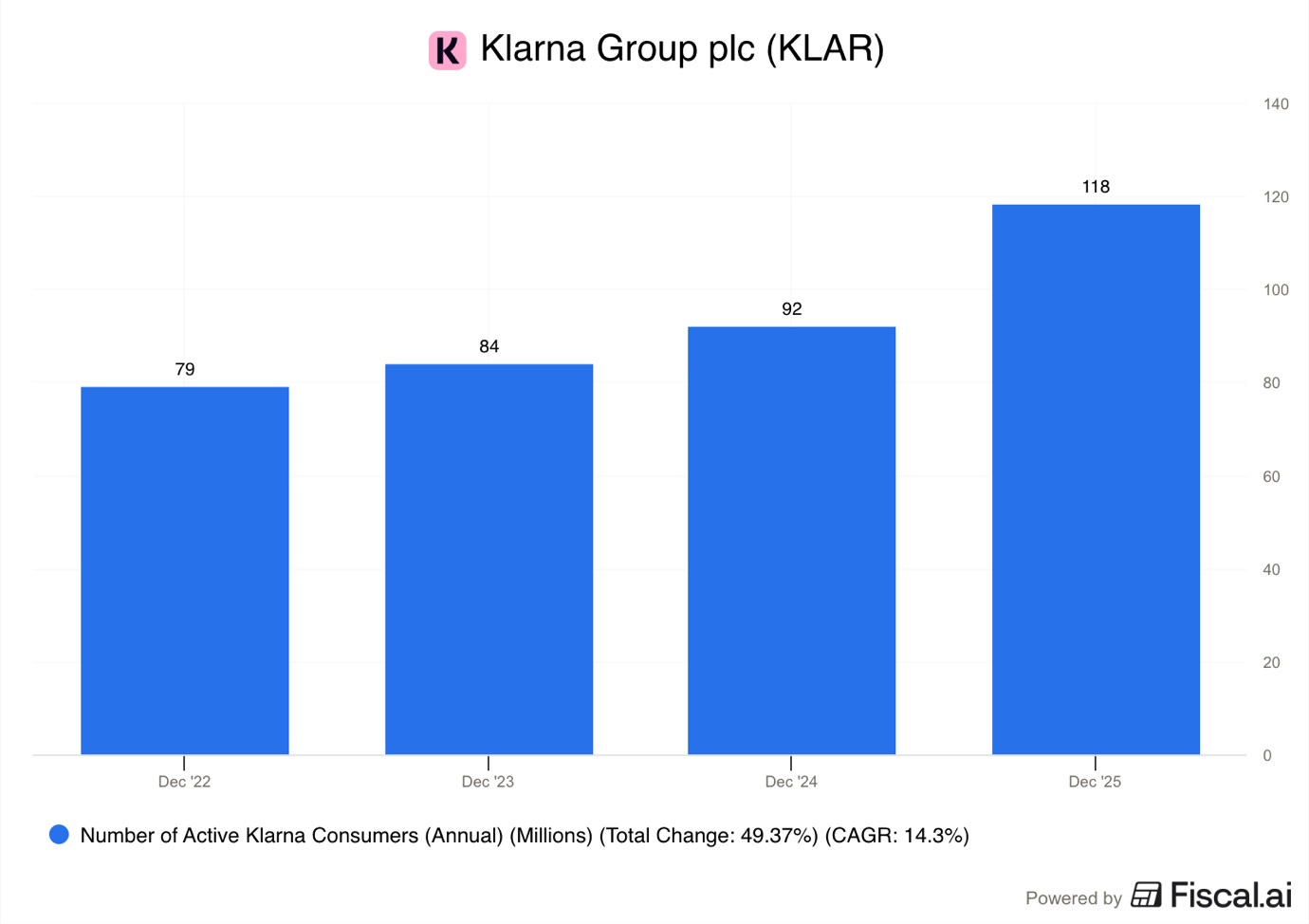

The business model of Klarna is built upon a two-sided network that brings together over 118M active consumers and nearly 1M merchants across 26 countries.

As you can see in the chart above, Klarna is rapidly growing its customer base despite its already massive scale.

This network creates a flywheel effect:

As more shoppers use the app, more stores want to offer Klarna at checkout, which then attracts even more shoppers!

Unlike a traditional bank that might only see a customer when they apply for a loan or visit a branch, Klarna is deeply embedded in the daily shopping habits of its users, processing millions of transactions.

This high frequency of interaction gives the company a massive amount of data, which it uses to make better decisions about who to lend money to and how to help people manage their finances more effectively.

1.1. Buy Now, Pay Later (BNPL)

The foundation of the Klarna experience is the Buy Now, Pay Later, (BNPL) service, which allows people to buy things immediately and pay for them over a short period without paying interest.

The most popular version of this is the Pay in 4 product, where the total cost is split into four equal payments made every two weeks.

This is a major shift away from how old-fashioned credit cards work.

A credit card company usually makes money when a person cannot pay their full bill and has to pay high interest rates, sometimes as high as 25% or 30%. In contrast, Klarna’s basic service is free for the person buying the item as long as they pay on time.

The money that Klarna earns from these transactions primarily comes from the stores themselves. Merchants are willing to pay Klarna a fee, often between 2% and 6% of the sale, because Klarna helps them sell more products, increasing average basket sizes.

When a store offers Klarna, more people finish their checkout, and the amount they spend is higher. Furthermore, Klarna takes on all the risk, the store gets paid the full amount immediately, and Klarna takes over the responsibility of collecting the payments from the customer.

The average company-level revenue-take-rate is now 2.7%, an increase from 2.5% in 2023!

As Klarna grows, it is likely to increase its take-rate as its platform becomes more attractive for partners, increasing Klarna’s ability to monetise transactions.

This relationship has allowed Klarna to partner with some of the biggest names in retail, including Walmart, H&M, Sephora, and Nike.

The company has also introduced a physical Klarna Card and a digital version that can be added to Apple Pay and Google Pay. This allows people to use Klarna’s flexible payment options even when they are shopping in a physical store, not just online.

By early 2026, the company had over 4.2M active card users, and in the United States, about 25% of all Klarna Card spending was happening in-person at brick-and-mortar stores. This shows that the business is moving beyond being just a button on a website to becoming a tool people use for their everyday spending.

Overall, Klarna’s BNPL volumes reached $128B in 2025, an increase of 54% since 2022, a CAGR of 15.6%!

1.2. Funding Strategy

To provide billions of dollars in loans to millions of people, Klarna needs a massive and reliable source of money.

In the early days of financial technology, many companies had to borrow money from big investment banks at high interest rates, which made it hard for them to be profitable. Klarna has taken a different path by becoming a regulated bank in Europe, which allows it to take deposits from regular people.

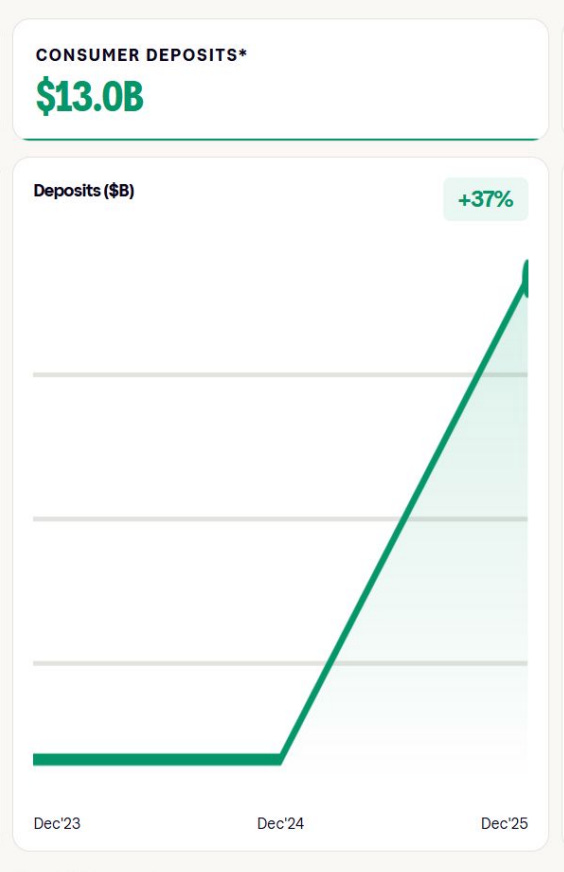

These deposits are a very important part of the company’s strategy because they are usually the cheapest way for a bank to get money.

By the end of 2025, Klarna had reached $13B in consumer deposits, a 37% increase from the year before.

About 90% of the money Klarna uses to fund its loans now comes from these deposits. However, as Klarna grows, especially in the United States, it needs even more capital. To keep its balance sheet light and avoid taking on too much risk, the company uses something called forward-flow agreements.

In these deals, Klarna agrees to sell a portion of the loans it makes to big investment firms. For example, the company signed a major deal to sell $6.5B worth of US loans to Elliott Investment Management. It also has a massive $26B agreement with a firm called Nelnet to fund its Pay in 4 products in America.

This strategy is very clever because it allows Klarna to earn money in two ways.

First, it earns a fee for every loan it starts and manages.

Second, it gets to move the risk of those loans off its own books and onto the books of the investors.

This means Klarna can keep growing its business very fast without needing to raise billions of dollars from selling more of its own stock. In the fourth quarter of 2025 alone, Klarna recognized a $73M gain just from selling these loans. This combination of cheap deposits from Europe and big investment deals in the US gives Klarna a powerful engine to fund its global expansion.

1.3. Transition to Banking

I already mentioned it, but Klarna is moving into banking.

The company refers to this as Phase Two of its evolution.

The idea is simple, once a person trusts Klarna to handle a small $50 purchase, they are much more likely to trust the company with their savings, their daily spending card, or a larger loan for a piece of furniture.

This transition is designed to make the company more profitable and to make its relationship with its customers much deeper.

The data shows that this banking strategy is working very well.

Klarna categorizes its most active users as banking consumers, these are people who use products like the Klarna Card, savings accounts, or Fair Financing.

These banking consumers are worth more than three times as much to the company as a regular user.

While a regular Klarna user might generate about $30 in revenue each year, a banking consumer generates $107. These users also use the app much more often, transacting about 28.5 times per year compared to only 10 times for the average user.

To speed up this change, Klarna is launching new features like instant peer-to-peer (P2P) payments, which allow people to send money to friends and family directly from the Klarna app.

This makes the app a central hub for all things related to money, not just shopping. The company is also using AI to make these banking services more efficient. By using AI assistants to handle customer service questions and manage simple tasks, Klarna can serve millions of banking customers with a much smaller staff than a traditional bank would need. This lower cost of doing business is a key advantage as Klarna competes with older, slower banks.

Essentially, with this feature, Klarna aims to rival Cash App and Venmo!

2. Finances

The financial health of Klarna has been a hot topic among bears of the BNPL industry, especially since it went through a difficult period in 2022 when its private valuation dropped significantly.

However, since that time, the company has undergone a massive transformation, focusing on cutting costs and using technology to become more efficient.

While the company is still dealing with some loan-related losses as it grows its lending business, its underlying numbers show a business that is becoming much more powerful.

2.1. Revenue Growth

Klarna has a long history of very fast revenue growth. Since 2016, the company has consistently increased the amount of money it makes every year.

In 2016, Klarna’s revenue was only $384M, but by 2024, it had grown to over $2.8B. This growth has continued into 2025, with total revenue reaching $3.5B, which is a 25% Y/Y increase.

As you can see in the graph above, the bulk of this growth came from operating revenues, coming from Klarna’s BNPL take-rate. $937M 27% of total revenues came from interest income, and $72M came from selling loans to credit investors.

This growth is driven by several factors.

First, more and more people are choosing to shop online and use flexible payment methods instead of old-fashioned credit cards.

Second, Klarna has successfully expanded into huge markets like the United States and the United Kingdom.

In the US specifically, Klarna’s revenue grew by a massive 58% in the final quarter of 2025 alone.

Finally, as Klarna adds more banking products, it is earning more money from each individual customer, which helps push total revenue even higher.

2.2. Historic Profitability

The story of Klarna’s profitability is one of a company that chose to invest a lot to grow very fast, then had to quickly learn how to be efficient when the economy changed.

For many years, Klarna was profitable, but it started losing money in 2019 as it began a massive push to win customers in the United States.

These losses grew very large in 2021 and 2022, reaching over $1B in 2022 as the company hired thousands of people and spent heavily on marketing.

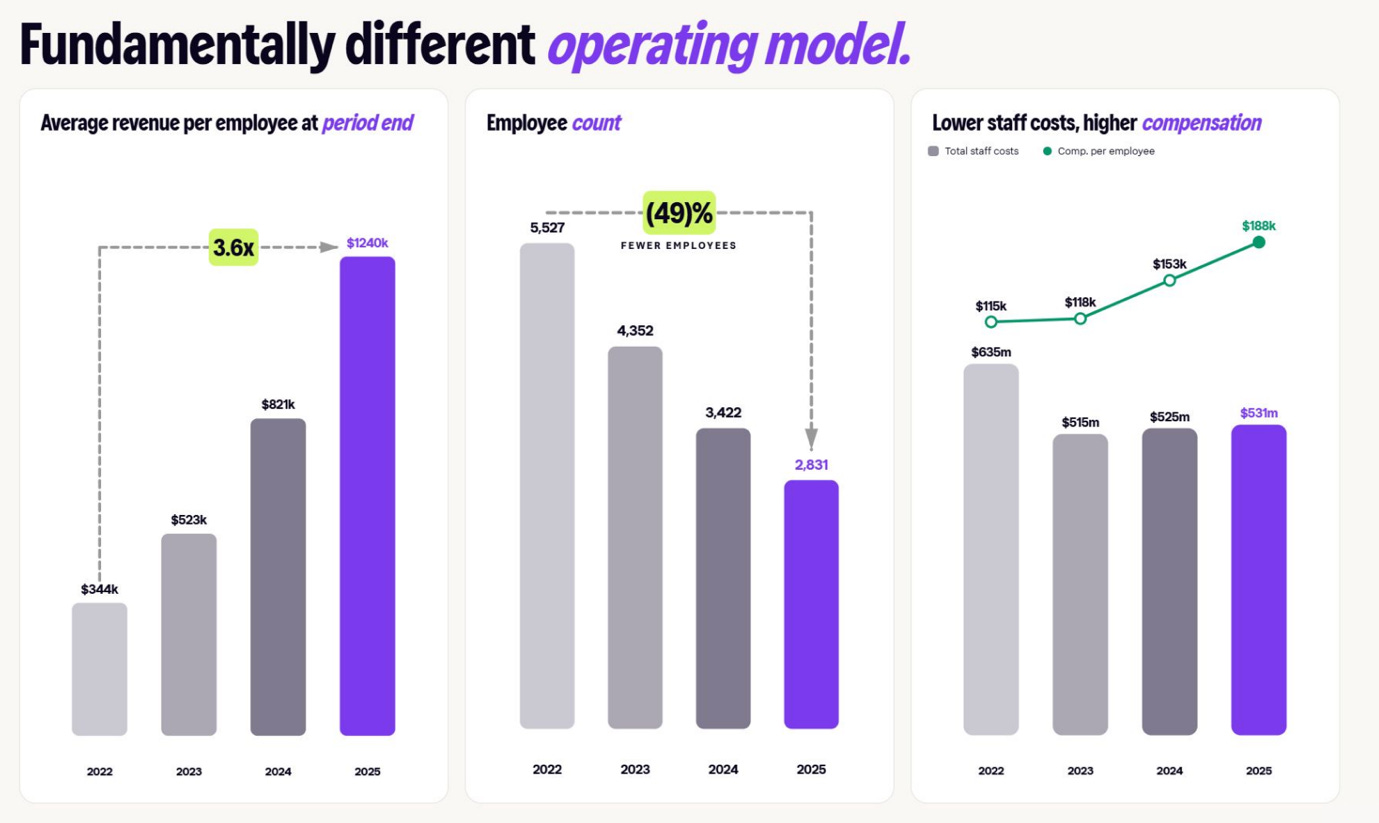

After the tech winter of 2022, Klarna’s leaders realized they needed to change their approach. They began a major effort to cut costs, which included laying off many employees and replacing manual work with automation and AI.

This plan worked incredibly well.

Revenue per employee 3.6x from $344K to $1.24M.

The number of employees fell by 49%, from 5,527 to 2,831.

Total staff costs fell by 16.4%, from $635M to $531M.

The average compensation per employee increased as Klarna automated many of the lower-paid tasks, such as customer service, and hired many higher-paid professionals.

In 2024, the company achieved a major goal by reporting its first annual net profit in five years, earning $21M. This showed investors that the business model could actually work and make money if it was managed carefully.

2.3. Current Profitability

In 2025, the company’s financials became more complex due to its rapid growth in lending.

For the full year of 2025, Klarna reported an adjusted operating profit of $65M, which is a measure of the income it makes from its core operations, excluding share-based compensation.

Despite that, the company also reported a total net loss of $273M for the year!

This might seem confusing, how can a company be profitable in one way but lose money in another? The answer lies in the rules of accounting for banks, specifically something called upfront loan loss provisioning.

When Klarna gives someone a long-term loan (like its Fair Financing product), the rules say it must immediately set aside money to cover the possibility that the person might not pay it back.

This counts as an expense right away.

However, the interest money that Klarna earns from that loan only comes in slowly over many months. Because Klarna’s lending business grew so fast in 2025, especially Fair Financing, which grew 165% in Q4, the company had to set aside a huge amount of money for future losses all at once.

This created a temporary drag on profits that management believes will turn into big gains in 2026 as the interest money starts to get collected.

You can see how this loan losses provision dynamic plays out in an illustrative example below from Klarna’s Q4 2025 earnings presentation.

Klarna shows that while a $1B loan portfolio generates strong lifetime profit (+$35M), a large portion of expected credit losses is recognized upfront, heavily impacting early-period earnings. As a result, the first quarter looks less profitable or even negative, while later periods benefit from revenue without additional provisions, making profitability appear stronger over time.

Simply put, Klarna is saying that its financial results will improve as they collect payments for loans for which it had already recognized losses!

2.4. Q4 2025 Results

Let’s look at Q4 2025 results to see the most up-to-date performance.

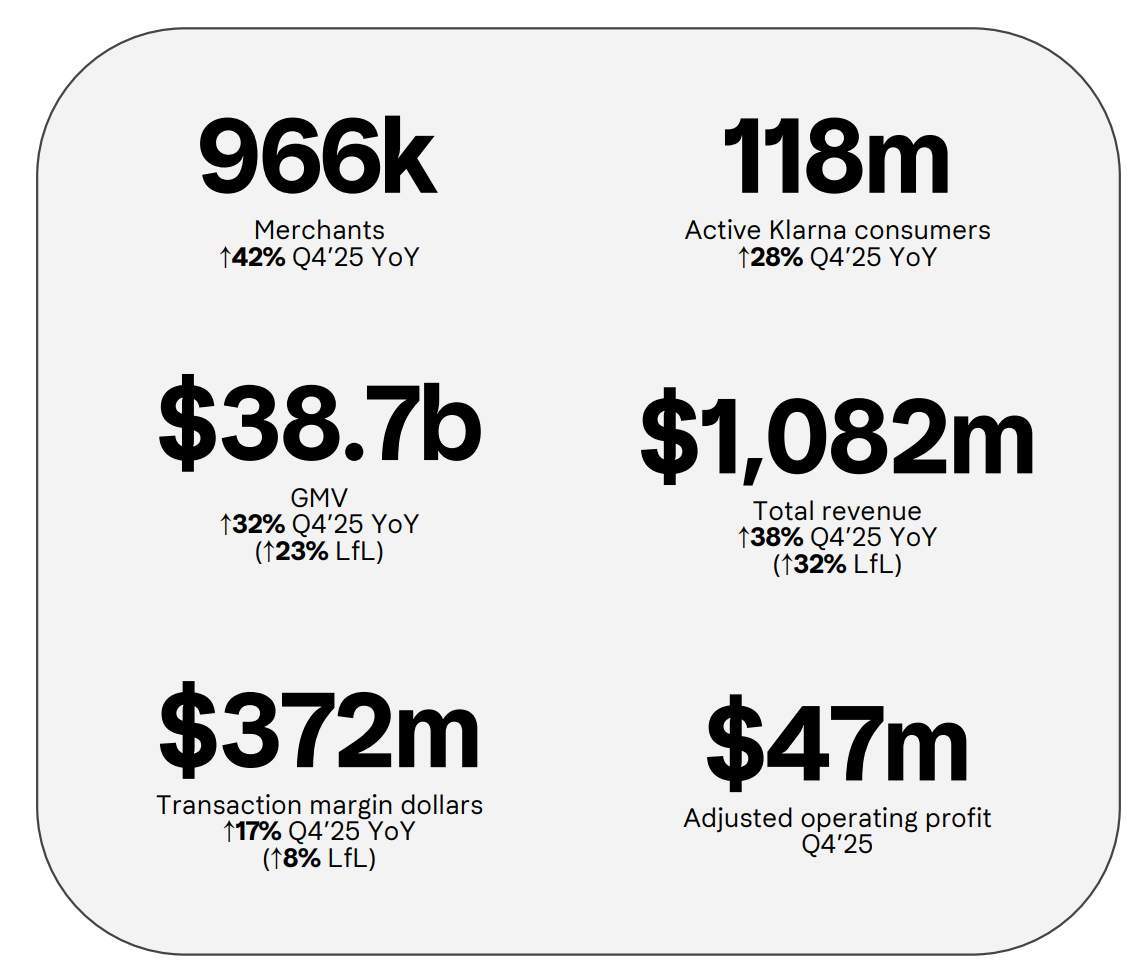

The Q4 2025 was a record-breaking period for Klarna, as it delivered its first-ever billion-dollar revenue quarter.

For the three months ending in December, the company brought in $1.082B in revenue, which was a 38% increase from the same period in 2024.

The total value of all goods sold through Klarna (GMV) reached $38.7B +32% Y/Y, which was also ahead of what the company had predicted.

Despite these record numbers, the stock market was disappointed by the results, and Klarna’s share price fell by about 26% after the news was released.

Investors were focused on a few specific problems:

Net Loss: The company lost $26M in the quarter, compared to a $40M profit in Q4 2024.

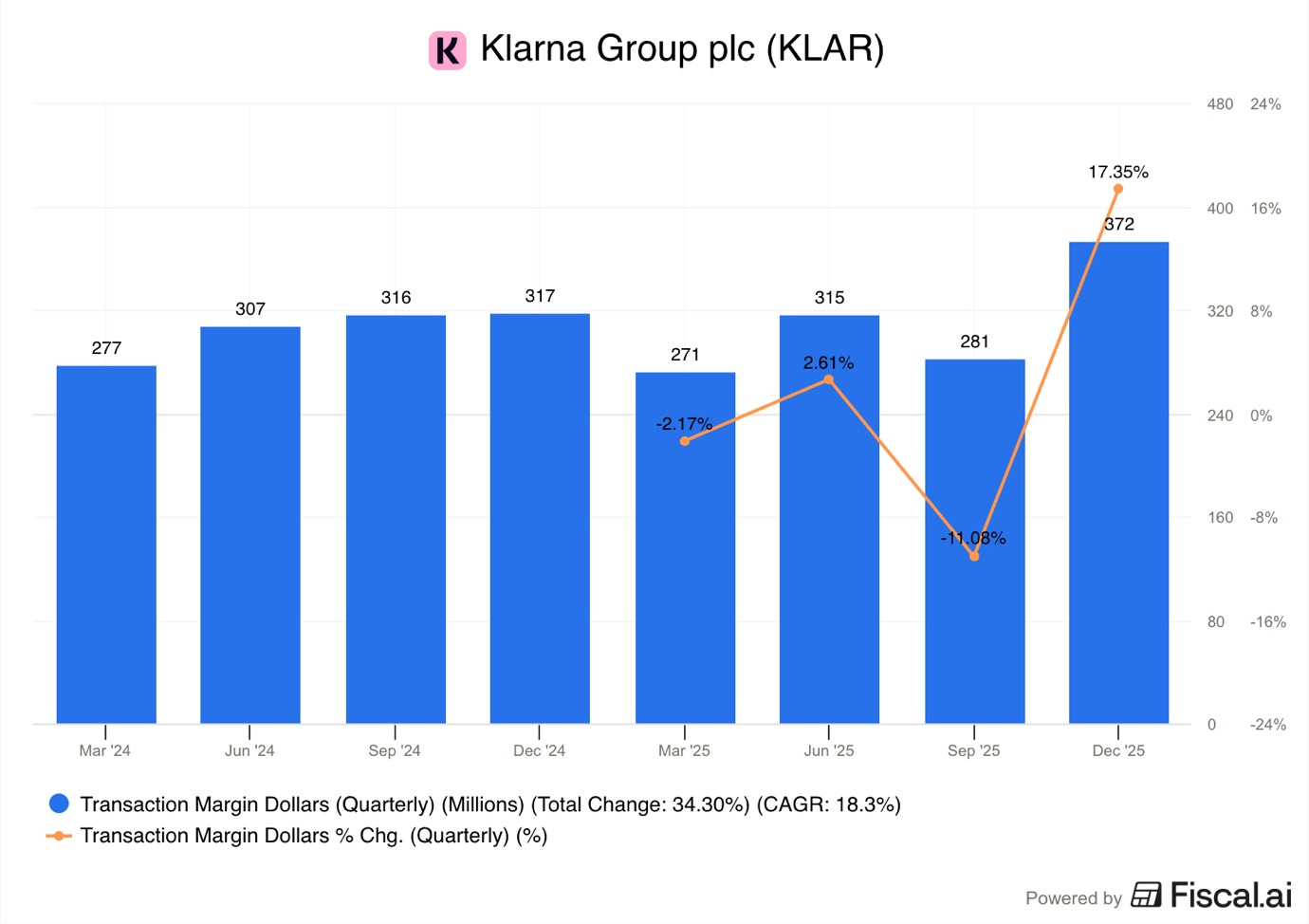

Margin Miss: A key metric, Transaction Margin Dollars came in at $372M, which was below the $390-$400M that the company had told investors to expect.

Guidance: The company’s predictions for the beginning of 2026 were more cautious than analysts had hoped, suggesting that growth might slow down a little bit.

Klarna’s Transaction Margin Dollars measure the profit generated from its transactions after subtracting funding costs, credit losses provisions, and directly associated operating costs. This focuses on unit economics at the transaction level, excluding broader operating expenses like marketing, tech, and overhead.

It grew only 17.35% to $372M, significantly below 38% revenue growth and 32% GMV growth, largely because of the loan loss provisions.

As I mentioned in the profitability section, the lower-than-expected margins were caused by the hypergrowth of their banking products. Because so many people signed up for Klarna Cards and Fair Financing loans in late 2025, the company had to set aside $250M for future credit losses in just three months.

While this hurt the profits for the fourth quarter, it builds a foundation for more interest income in the future.

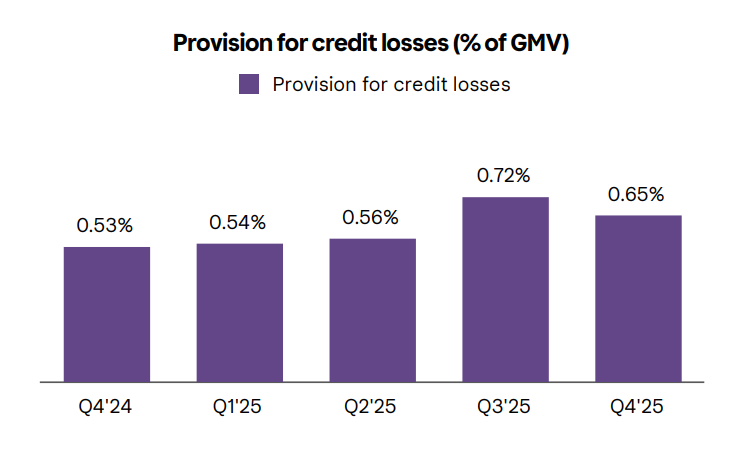

Importantly, the actual rate of people failing to pay their loans is actually going down. Credit loss provisions fell to 0.65% of GMV in Q4, down from 0.72% in Q3. This shows that Klarna’s credit models are getting better at picking the right people to lend money to, even as they lend out more money than ever before.

Lastly, Klarna gave a weaker-than-hoped outlook.

GMV to reach $155B, revenue take rate to increase to 2.8%, and ADJ operating profit of 6.9%.

While Q1 2026 GMV and revenue were expected to grow strongly, the Transaction Margin Dollars growth is expected to be much lower (11–26%), signaling continued margin compression. Klarna is earning less profit per transaction, likely due to higher loan loss provisions.

Even more concerning, adjusted operating profit guidance ($5–$35M) was extremely low relative to nearly $1B in quarterly revenue, implying very thin or volatile profitability.

The wide ranges in 51%–959% for operating profit growth also suggested low visibility and high uncertainty, which investors typically interpret negatively.

Do you like this report?

Become a Paid Premium member to see dozens of exclusive pay-walled equity research reports such as this.

Curious about which stock I own?

Full portfolio with all holdings, cost basis, and unrealised gains is visible to Premium members. I do detailed monthly updates and notify members of all sales and purchases using the pay-walled Substack Chat.

The annual plan is available for 50% of the monthly plan.

3. The Growth Opportunity

Looking ahead, Klarna has two major paths to continue growing its business:

Expanding BNPL

Banking

The company is no longer just competing with other checkout buttons, it is competing with traditional banks, credit card companies, and even fintech giants like Amex, PayPal, Sofi, Revolut, and Square.

3.1. BNPL Opportunity

The market for Buy Now, Pay Later is still growing very fast around the world.

Experts at Market.US project that the global BNPL market will reach over $115B by 2032, a CAGR of 25.3%!

Klarna is a leader in this space and is finding new ways to make its service available everywhere. One of the biggest opportunities is moving into high-value sectors like travel, healthcare, and home improvement. For example, in early 2026, Klarna’s fastest-growing categories were leisure, sport, and wellness products.

Moreover, Klarna is also making it much easier for stores to offer its service by partnering with major payment platforms like Stripe.

This means that instead of Klarna having to go to every store one-by-one, millions of stores that already use Stripe can turn on Klarna with just a few clicks. The company is also working on agentic commerce, where AI assistants will soon be able to shop and pay for things on behalf of consumers.

By integrating with Google and Stripe’s AI systems, Klarna is positioning itself to be the preferred way to pay in this new world of automated shopping.

3.2. Banking Opportunity

However, despite the strong BNPL growth, the biggest financial opportunity for Klarna is the shift into retail banking.

In the past, Klarna made most of its money from small fees on millions of short-term transactions. Now, it is starting to make money in the same way that big banks do, by earning interest on loans and using people’s deposits to fund those loans.

The growth of the Klarna Card is a great example of this. In just four months after its major launch, the card had 4M sign-ups.

This card allows Klarna to be part of a person’s life every single day, whether they are buying a coffee or paying for a gym membership. As more people use the card and keep money in Klarna savings accounts, the company’s relationship with them becomes much more sticky, thus they are less likely to leave for another bank.

Just a short time after lunch, banking customers have reached 15.8M and are growing 101% Y/Y.

The transition to banking also allows Klarna to solve one of the biggest problems with its old business model, the high cost of finding new customers.

A traditional bank might spend hundreds of dollars in advertising just to get one person to open a new account. Klarna could get its customers for less through its shopping app, and then it can slowly offer them more banking services over time. This low-cost acquisition is a huge competitive advantage that should allow Klarna to be as profitable as old-fashioned banks in the long run.

4. Valuation

Since Klarna became a public company in September 2025, its stock price has been very volatile. Investors are currently trying to decide if Klarna should be valued like a high-growth fintech or like a subprime lender.

The stock price is down 69% since the IPO, sitting at a market cap of $5B!

Technology companies usually get valued at a high multiple of their sales, while banks are valued based on their profits and the value of the assets they own. This narrative fight has caused the stock to move up and down based on every new piece of news.

As of mid-March 2026, Klarna’s stock price is trading around $13.39 per share. This is much lower than the $40 per share it was valued at when it first joined the stock market. There are several reasons why the stock has struggled:

The Lock-up Expiry: On March 9, 2026, a rule that prevented many early investors and employees from selling their shares ended. This made about 335M new shares available for trading, which caused the price to fall as some insiders, like the Chief Marketing Officer and the Chief Commercial Officer, decided to sell and take their money out, about $300-400K each.

Sector Pressure: The entire fintech sector has been under pressure because of high interest rates and concerns about whether consumers will keep spending money in light of higher oil prices stemming from the Iran War.

Profitability Lag: As mentioned before, the company’s rapid growth has caused it to report accounting losses, which makes some investors nervous, even if the underlying business is strong.

However, not everyone is selling. In March 2026, the Chairman of Klarna’s board, Michael Moritz, spent $50M of his own money to buy more shares. This could be a signal that the people who know the company best believe the stock is currently too cheap.

Other big investment firms have also started buying the stock at these lower prices.

4.1. Valuation Multiples and Comparison to Peers

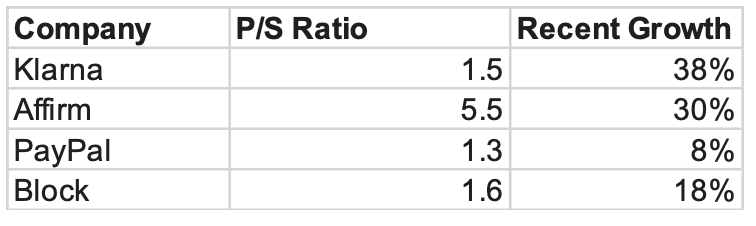

When we compare Klarna to its main competitors, we can see that it is currently valued at a lower multiple than some of its peers. The most direct comparison is Affirm, which is a big BNPL company in the United States. Affirm’s stock is currently valued at about 5.5 times its annual revenue, while Klarna is valued at a much lower multiple, 1.6x.

There is some debate among investors about whether Klarna deserves a higher valuation.

Those who are bullish argue that Klarna is growing faster than PayPal or Block and has a much more efficient business model. They believe that as Klarna starts showing consistent profits in late 2026, its valuation multiple will rise to match or even beat Affirm’s.

Those who are bearish worry that Klarna’s move into longer-term lending is risky and that they don’t have enough history of managing these types of loans through a bad economy.

4.2. Analyst Growth Expectations

Most Wall Street analysts believe Klarna has a bright future, despite the recent drop in the stock price. Out of 14 analysts, 10 rate the stock as a Buy and 4 rate it as a Hold.

Their average 12 month price target is about $27.27, which would be a huge, 104% increase from the current price of around $13.39.

However, 2026 is expected to be transitionary year, where net income remains low due to high loan loss provisions, which are front-loaded due to accounting rules.

The general expectation is that Klarna will become consistently profitable by the year 2027.

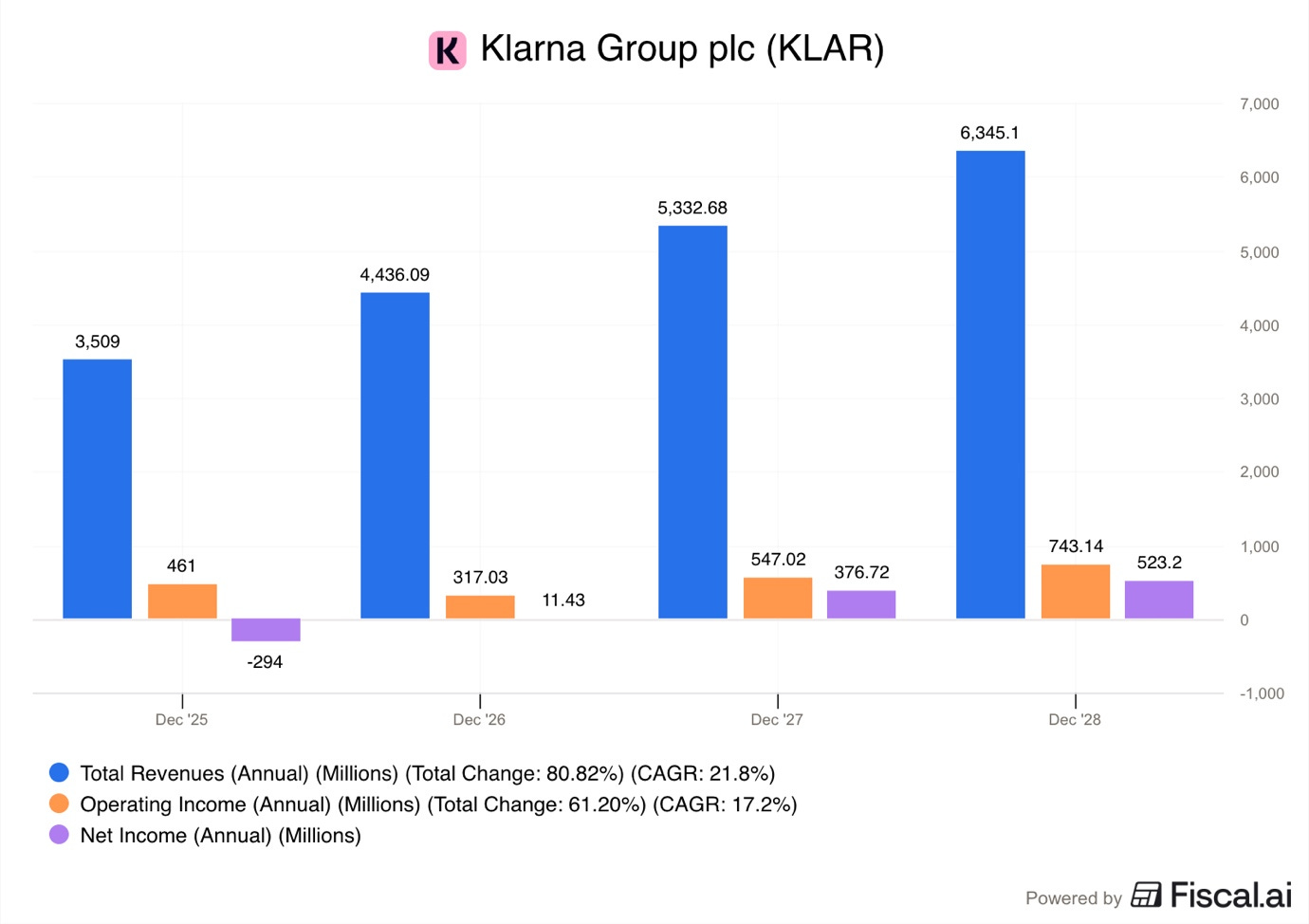

As you can see in the graph above, analysts expect revenue to reach $6.45B in 2028, growing with a CAGR of 21.8%.

This growth, combined with the company’s ability to keep its costs low, could lead to strong profit margins once the initial costs of starting new loans have been paid off.

The 2028 operating income estimate sits at $743M, a margin of 11.7%.

Net income estimate is at $523M, a margin of 8.2%.

Taking these estimates into account, Klarna trades for a 2028 P/E of 11.

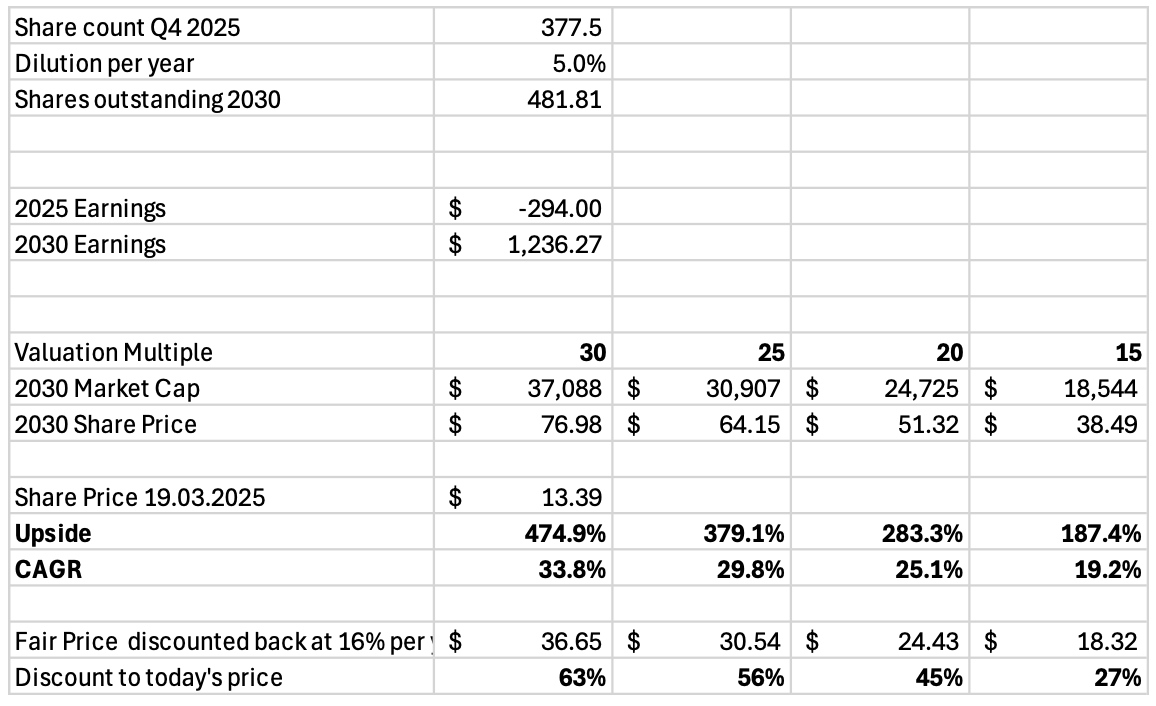

5. 5-Year Valuation Model

To understand what Klarna could be worth in the future, we can build a simple model that looks out five years to the year 2030.

In an optimistic scenario, we assume that Klarna continues to grow its revenue at 20% per year and that it successfully becomes a highly profitable digital bank.

Assumptions:

2025-2030 Revenue CAGR of 19%.

2030 Operating margin of 22%

Tax and other expenses 30% of the operating income in 2030.

We get 2030 Revenues of $8B, an increase of 129% from 2025!

Net income of $1.24B, vs $294M loss in 2025!

Dilution of 5% per year.

Exit multiple of 20, and we get a $51.32 stock.

That would be an upside of 383% from today’s share price of $13.39!

Discounting back 5 years at 16% per year to today, we get a fair value per share of $24.43.

This implies Klarna’s share price of $13.39 is trading for a 45% discount.

6. Conclusion

Klarna is a company that is aiming to fundamentally change how the world thinks about money, shopping, and banking.

By moving away from the old, expensive model of credit cards and building a transparent, AI-driven alternative, the company has won the loyalty of over 118M people.

The transition into a global digital bank is the most important part of its future, as it allows Klarna to earn more money from every customer while providing them with better services like the Klarna Card and high-interest savings accounts.

While the company’s stock price has struggled in the months following its IPO, the underlying business metrics tell a story of incredible strength. Klarna is guiding for 26-30% revenue growth in Q1 2026.

Its banking customers are doubling every year, and it is using technology to become more efficient than almost any other bank on the planet.

The temporary accounting losses caused by its rapid growth in lending are a sign of future value being built, not a sign of failure. For investors who are willing to look past the short-term ups and downs of the stock market, Klarna represents a unique chance to own a piece of the bank of the future.

Klarna seems it could have a place in an growth minded long term portfolio.

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 11 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

Really enjoyed this mate - keep it up!