Lumentum: Nvidia Moment or Hype?

Fast Growing Manufacturer of Lasers Crucial for the AI Revolution!

Is Lumentum experiencing an Nvidia Moment?

When the AI boom really began after the release of ChatGPT, Nvidia saw the demand for its AI GPUs explode.

From 2022 to 2026, Nvidia’s data center business grew 18x in just 4 years, to nearly $200B!

As we are reaching the limits of what current technologies can achieve, Nvidia has invested billions in its suppliers to help them develop technologies critical for making AI better, faster, and cheaper.

$2B went to the company we are covering today, Lumentum!

Lumentum is a technology company that specializes in photonics, a field that is enabling the shift from electrical signals to light-based signals.

For a long time, Lumentum was known for helping companies with lasers that enable 4G and 5G technology, but today it has a much more exciting job.

It provides the digital plumbing that allows AI to function. As AI models become more powerful, they need to move massive amounts of information between chips at literal light speeds.

Lumentum builds products that make this fast data movement possible, and its products are experiencing an increase in demand comparable to Nvidia in 2023.

Revenues are projected to more than 3x by 2028!

As a result, Lulemtum’s stock has risen by over 1,000 in the past year!

This report examines the company’s strategic role in the burgeoning AI data center markets, its business units, financials, and its long-term valuation potential.

As always, the report will conclude with a 2030 Valuation Model.

Let’s begin.

1. Photonics and Nvidia

2. Business Model

3. Finances

4. The Opportunity

5. Valuation

6. Valuation Model

7. Conclusion

1. The Photonics Industry and Nvidia

Before getting to Lumentum and what products the company provides, let’s talk a bit about the Photonics Industry.

Because training and running AI models require an extreme quantity of data, the demand for data processing has reached a level where traditional copper-based electrical systems are no longer sufficient.

In modern data centers, especially those built to support large-scale AI models developed by Anthropic and OpenAI, the sheer volume of data moving between processors creates massive amounts of heat and consumes excessive power.

This physical limitation, often referred to as the interconnect bottleneck, has forced the industry to look toward light as the primary carrier of data.

Photonics, which involves the generation, manipulation, and detection of light particles, or photons, offers a solution that is faster, cooler, and more energy-efficient than copper.

The strategic importance of this technology is best illustrated by the actions of Nvidia!

Recognizing that its future growth depends on the ability to move data between its high-performance chips at incredible speeds, Nvidia has made significant financial commitments to secure its supply chain.

In early 2026, Nvidia announced a $4B investment initiative within the photonics sector. This initiative included $2B each invested into Coherent and Lumentum, two of the largest established players in the optical technology market.

These investments are part of a multi-year strategic partnership intended to enhance the energy efficiency and resilience of AI factories. Nvidia’s commitment includes multi-billion-dollar purchase agreements to ensure it has priority access to advanced laser components and optical interconnect technologies.

This massive capital inflow into the sector validates the entire market.

It signals that the biggest names in technology view optical components as the critical infrastructure of the next decade.

2. Business Model

Lumentum is a key player in this emerging photonics niche.

The company operates a B2B model, where it sells its advanced parts to other giant technology companies that build the world’s internet and computer systems.

Lumentum acts as a picks and shovels provider during the AI gold rush, and often those selling the tools make a steadier income than the gold miners themselves.

In this case, the “gold” is AI, and Lumentum is selling the essential tools needed to make AI more powerful.

The core of this B2B model relies on deep partnerships. Because Lumentum’s parts are so specialized, they cannot just be bought off a shelf. Tech giants like Google, Microsoft, and Nvidia have worked with Lumentum for years to design parts that fit perfectly into their systems.

These relationships are often backed by long-term agreements where customers promise to buy a certain amount of parts years in advance to make sure they do not run out.

This creates a very stable business where Lumentum knows exactly who its customers are and what they need for the next several years.

The company serves three main types of customers in this B2B setup.

First are the hyperscalers that own massive data centers where AI lives.

Second are the telecommunications companies that build the global phone and internet networks.

Third are industrial and consumer electronics companies that use lasers for things like manufacturing or face-ID on phones.

By selling to these different groups, Lumentum makes itself a necessary partner for almost every part of the modern digital world.

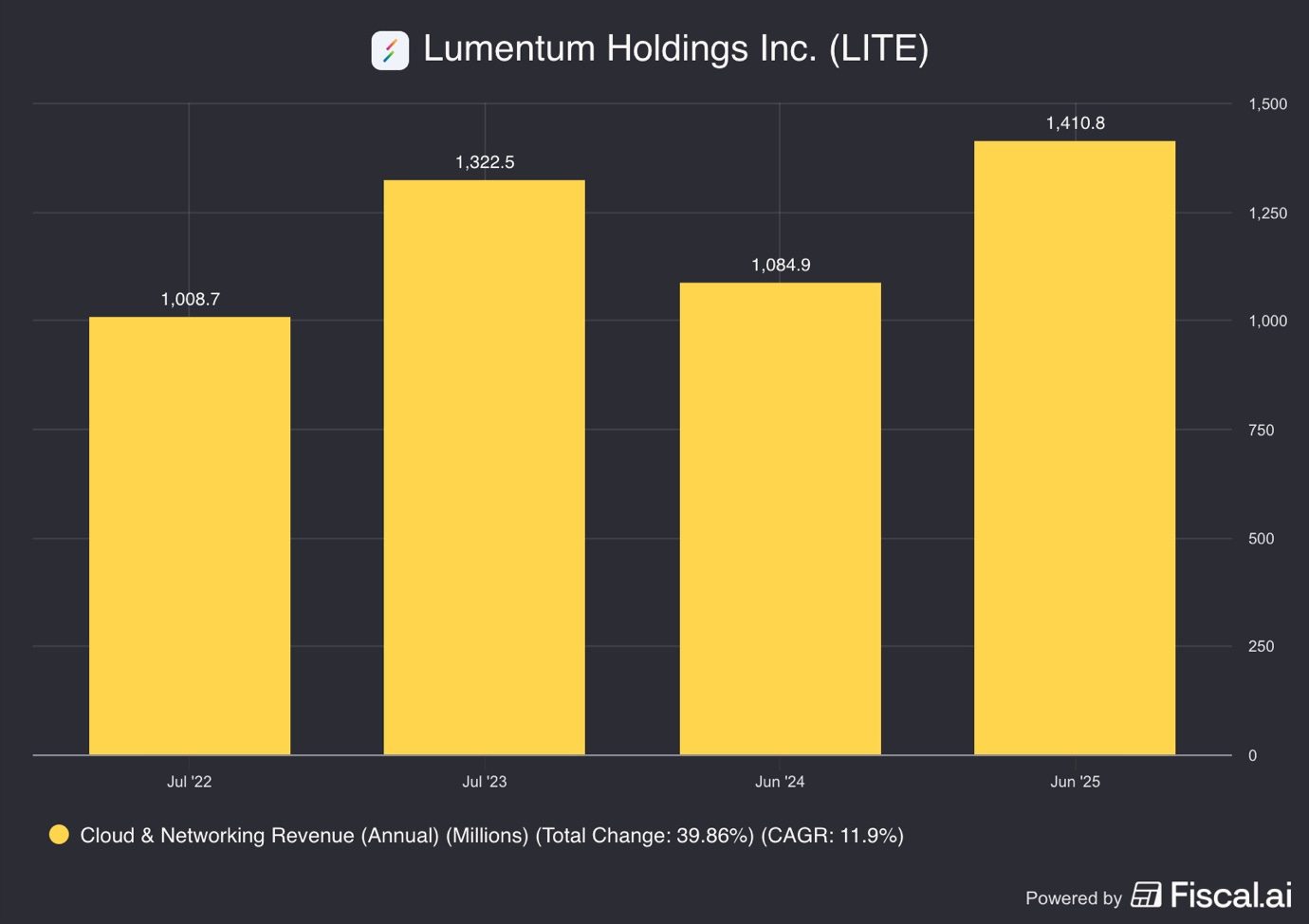

2.1. Cloud & Networking Segment

The Cloud & Networking segment is the primary engine of Lumentum’s business, making up about $1.4B or 86% of 2025 revenues.

This segment focuses on moving data through fiber optic cables using light. In the past, this business mostly sold to companies building 5G networks, but today, the biggest growth comes from AI data centers.

Inside an AI data center, thousands of GPUs must talk to each other to solve complex problems. Moving this much information using copper wires is no longer the best solution because copper gets too hot and cannot move data fast enough.

Lumentum sells the solution, optical transceivers, and the high-speed laser chips that power them. These devices turn electrical signals from the computer into light pulses that travel through glass fibers.

Large tech companies like Nvidia buy the laser chips to put into their own high-end networking gear.

The second group is the hyperscale cloud providers like Google, Amazon, and Meta, who buy complete optical systems to connect their servers.

Because these companies are building the largest computer systems in history, they need millions of Lumentum’s lasers, making this segment a high-volume, high-profit part of the business.

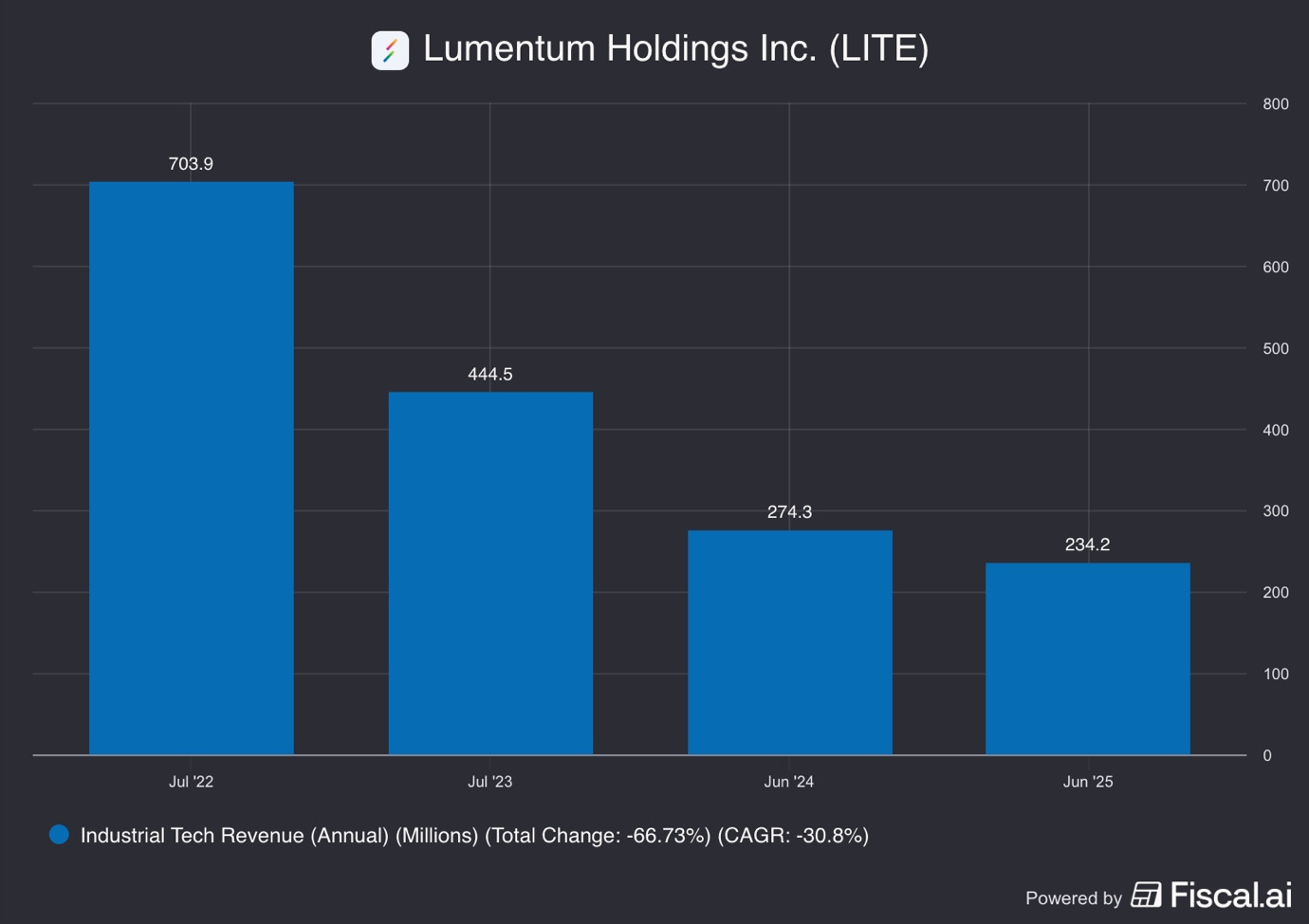

2.2. Industrial & Tech Segment

The Industrial & Tech segment accounts for the remaining 14% of Lumentum’s revenue.

As you can see in the graph above, this segment has been underperforming for a few years!

This part of the business uses the company’s expertise in lasers for applications outside of the internet and data centers. The customers range here is diverse, ranging from car companies to smartphone makers and various other factories.

One of the most famous uses of Lumentum’s technology in this segment is for 3D sensing. The company produces tiny lasers called VCSELs that allow smartphones to scan a user’s face for security, such as Apple’s FaceID.

Meanwhile, in the automotive industry, these lasers are used for lidar, which helps self-driving cars and trucks see their surroundings by bouncing laser light off objects to create a 3D map of the road.

Lumentum also sells high-power lasers used in heavy manufacturing.

These lasers are so precise and powerful that they are used to cut through metal for cars, drill tiny holes in circuit boards, and even help manufacture electric vehicle batteries.

While this segment is smaller than the networking side, it provides Lumentum with a presence in the future of transportation and advanced manufacturing. However, as AI demand has surged, Lumentum has started to focus more on its higher-profit networking parts, sometimes moving workers and factory space away from these industrial products to meet the massive demand for AI infrastructure.

As the Lumentum technology and its use cases have been converging, the company has decided to stop separating its business into these 2 Cloud and Industrials categories.

Instead, the company will separate revenues based on Systems and Components.

2.3. Components & Systems

Lumentum has been actively focusing on vertical integration.

This means that instead of just designing a part and asking another company to make it, Lumentum controls almost every step of the process.

Components – $444M last quarter, high-margin specialized chips and lasers.

Systems – $222M last quarter, complete modules and switches sold to end-users.

The value chain strategy follows three clear steps:

Designs Chips: Lumentum’s engineers design specialized semiconductor chips made of a material called Indium Phosphide. These chips are the most difficult part to make and act as the brain of the laser.

Manufactures Lasers: Lumentum owns its fabs, where it makes the materials and builds its own lasers. The Electro-absorption Modulated Laser (EML) is the most advanced in the world for moving data and is seeing strong demand.

Integrates into Systems: With the acquisition of Cloud Light in 2023, Lumentum can now take its own lasers and build them into complete systems like transceivers or optical switches. This allows the company to sell a finished product directly to cloud providers, which lets them have better margins.

By owning the whole process, Lumentum ensures that its products are more reliable than those made by companies that outsource their manufacturing. In the world of AI, where a single broken laser can stop a million-dollar calculation, this reliability is a major reason why companies like Nvidia and Google choose Lumentum.

Do you like this report?

Become a Paid Premium member to see dozens of exclusive pay-walled equity research reports such as this.

Curious about which stock I own?

Full portfolio with all holdings, cost basis, and unrealised gains is visible to Premium members. I do weekly updates and detailed monthly reviews. Premium members are also notified of all sales and purchases using the pay-walled Substack Chat.

The annual plan is available for 50% cheaper per month than the monthly plan.

3. Finances

Lumentum’s financial health has changed dramatically over the last few years. For a long time, the company was a steady but slow-growing provider of parts for wireless communications networks.

However, the sudden need for AI infrastructure has turned it into a fast-growing company with incredible sales growth.

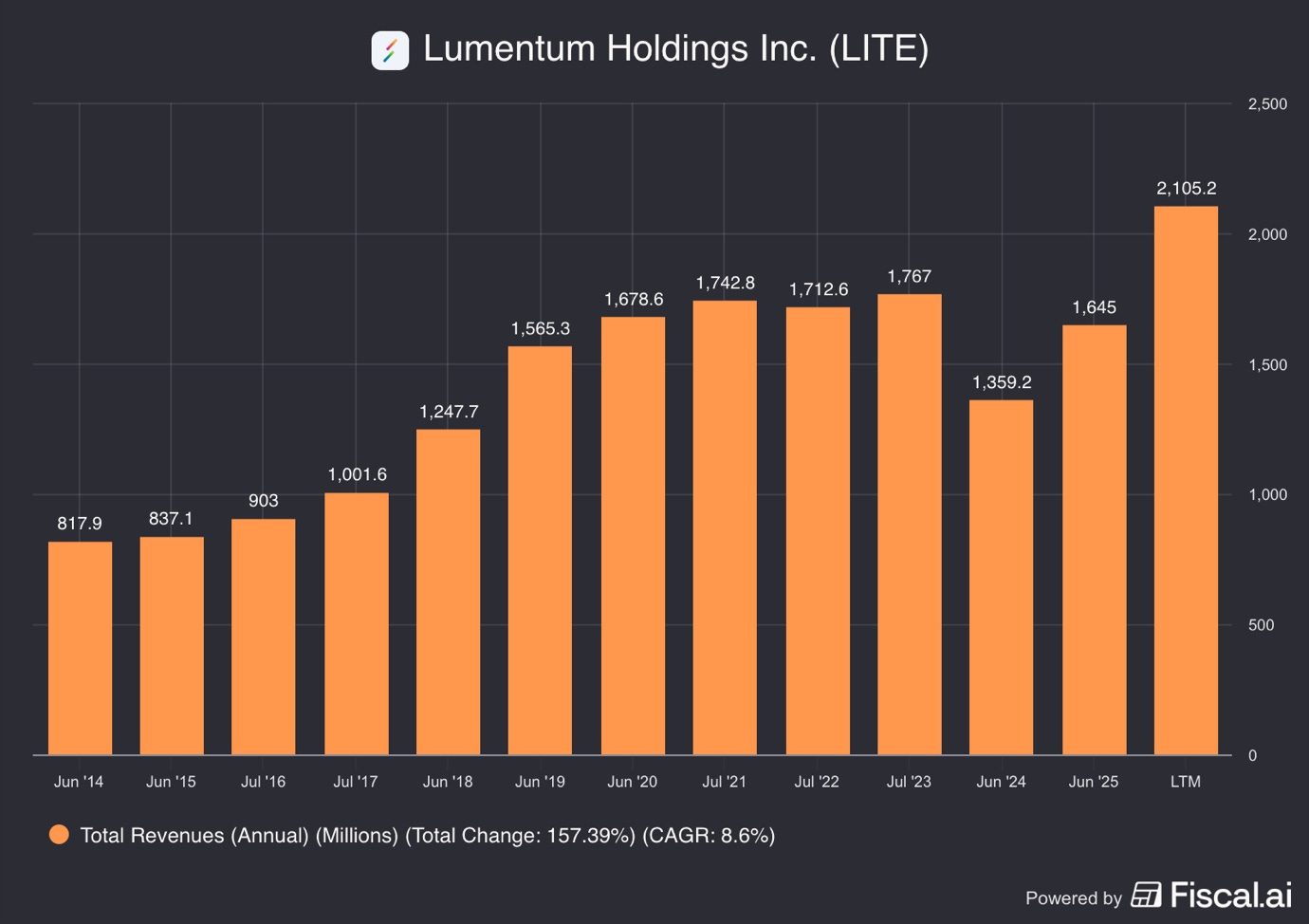

3.1. Historic Revenue Growth

Historically, Lumentum’s revenue growth was modest.

In the years leading up to 2024, it grew at a slow CAGR of about 5.2%, reaching $1.4B!

As we can see in the graph above, in 2024, the company actually saw its revenue decline meaningfully as carriers slowed down their capex spending on new 5G networks.

However, fortunately for Lumentum, the AI supercycle began to show up in the numbers in late 2025.

The company’s total revenue grew from $1.36B in mid-2024 to $2.1 billion in LTM as of February 2026, representing 55% growth.

This growth was driven almost entirely by the demand for high-speed lasers used in AI data centers.

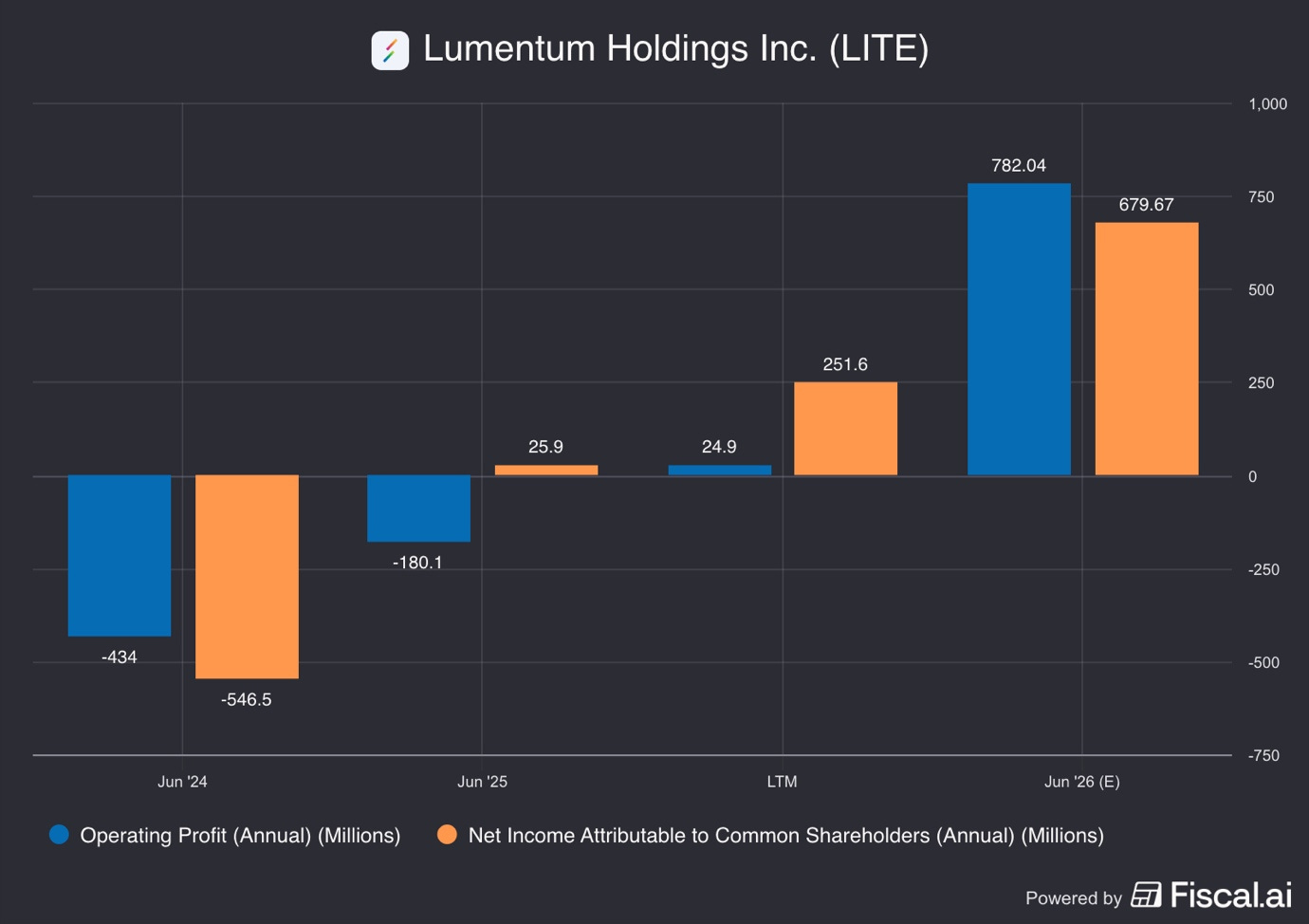

3.2. Historic Profitability

Profitability has been difficult and patchy for Lumentum.

2020-2022 were quite strong, with operating income and net income peaking at $527M and $397M.

However, from 2023-2024, the company reported net losses, peaking at $546.5M in 2024.

This was because it was spending a lot of money to build new factories to prepare for future growth.

3.3. Current Profitability

By 2026, Lumentum’s profitability has seen a massive turnaround.

As it started selling more expensive, high-speed parts, its profit margins began to expand.

In 2025, the company reduced operating losses to $180M and showed a positive net income of $26M thanks to a $200M tax benefit.

In the LTM, we can see that operating income is now at a positive $25M, ending losses. Meanwhile, net income is now at $251.6M, excluding the tax benefit, the company would have made $51M in net profit.

Looking at 2026 estimates, we see that Lumentum is expected to return to strong profitability, with operating income jumping to $782M and net income to $680M!

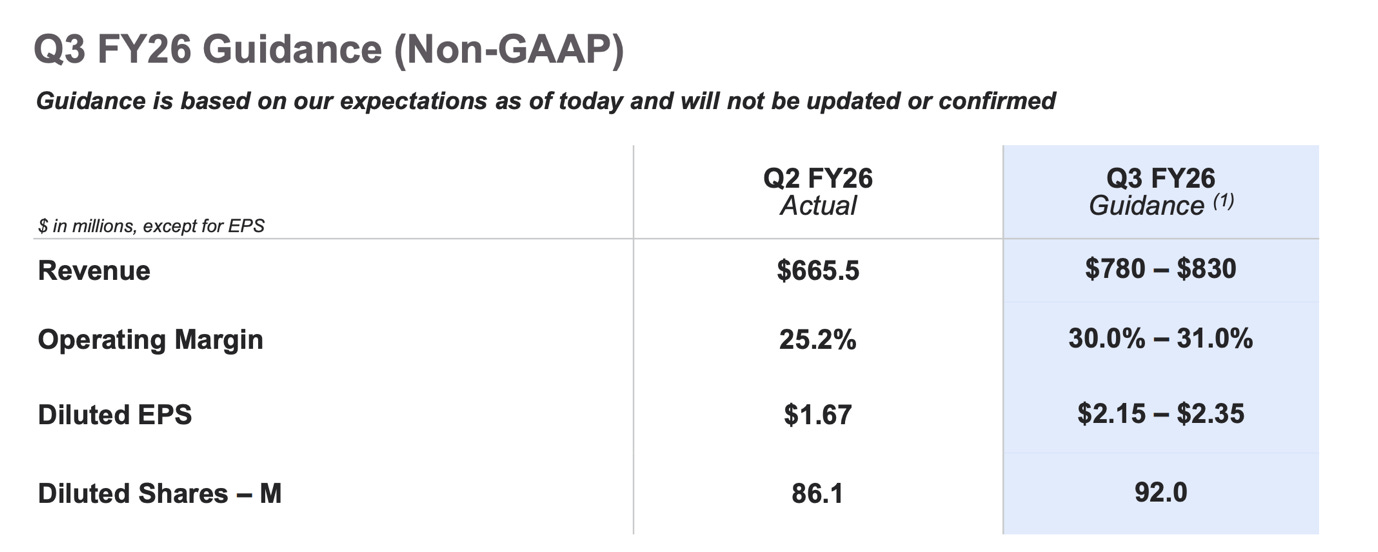

3.4. Financial Year Q2 2026 Results

The FY Q2 2026 was the best quarter in the company’s history.

Lumentum reported revenue of $665.5M, +65.5% Y/Y, beating analyst expectations of $650M.

The most impressive part of the report was the profitability expansion. The company’s GAAP EPS hit $0.89, compared to the $0.88 loss last year.

Management attributed this to the fact that they are now selling many more 200G laser chips, which are high-speed parts that sell for a lot of money and have high profit margins.

Additionally, we see that operating expenses as a % of revenue have fallen from 37.6% in Q2 2025 to 26.4% today. This is a clear sign that operating leverage is being achieved, as expenses don’t grow in tandem with revenues.

Most importantly, the company gave very optimistic guidance for the third quarter of 2026.

Lumentum expects revenue to grow even faster, reaching about $780-830M, implying 83-95% Y/Y growth!

Furthermore, they also expect their operating margins to continue climbing toward 30% or higher as they scale up their production of AI-related products.

This quarter proved that Lumentum is no longer just a steady company but is now a high-growth leader in the AI hardware market, experiencing an Nvidia-like growth.

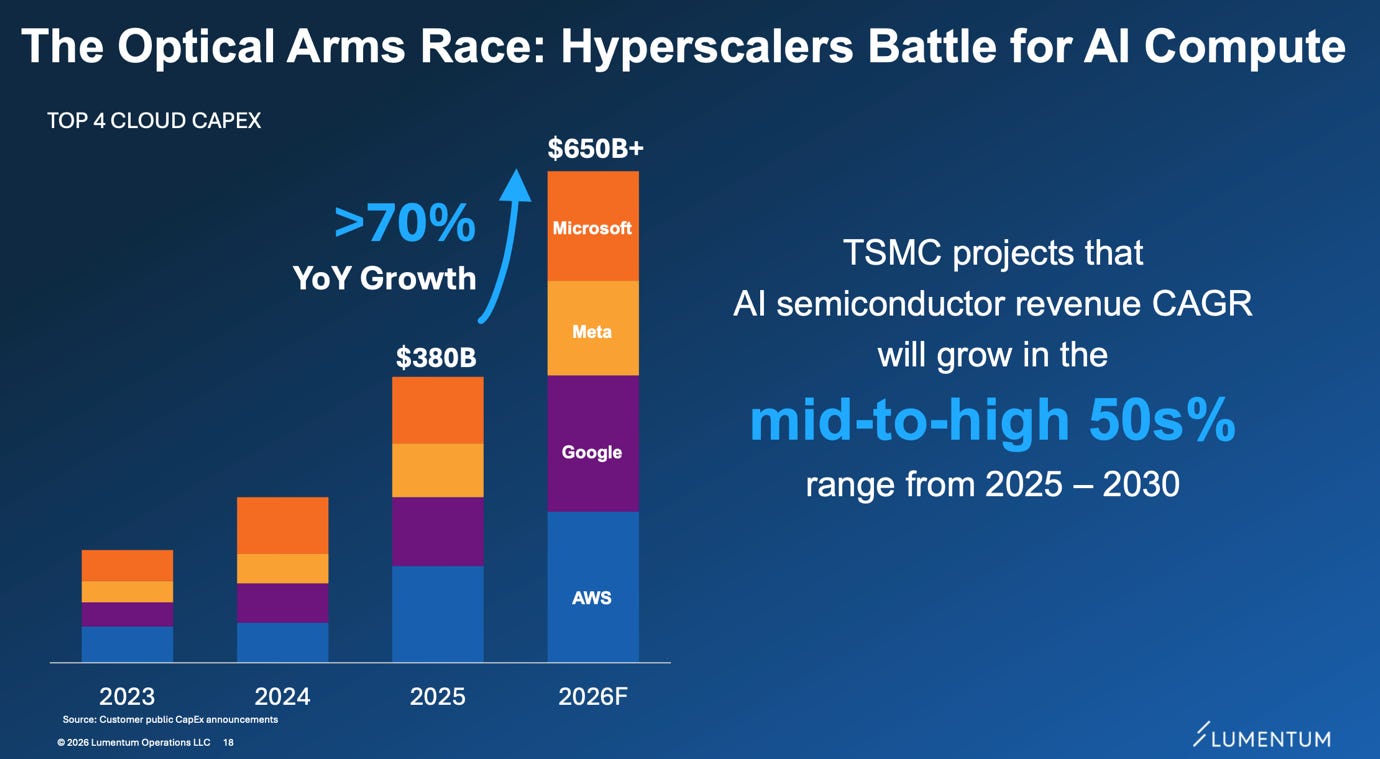

4. The Growth Opportunity

Hyperscales are set to spend $650B in 2026 on capex in 2026, an increase of 70% Y/Y!

Increasingly, this money is being spent across the AI ecosystem to deliver improved cost efficiency, elevating new winners.

Lumentum is standing at the center of a massive change in how AI servers are built.

This change is driven by the need to move huge amounts of data quickly to train AI models. Because traditional electrical wires cannot keep up, the world is moving toward Lumentum’s optical solutions.

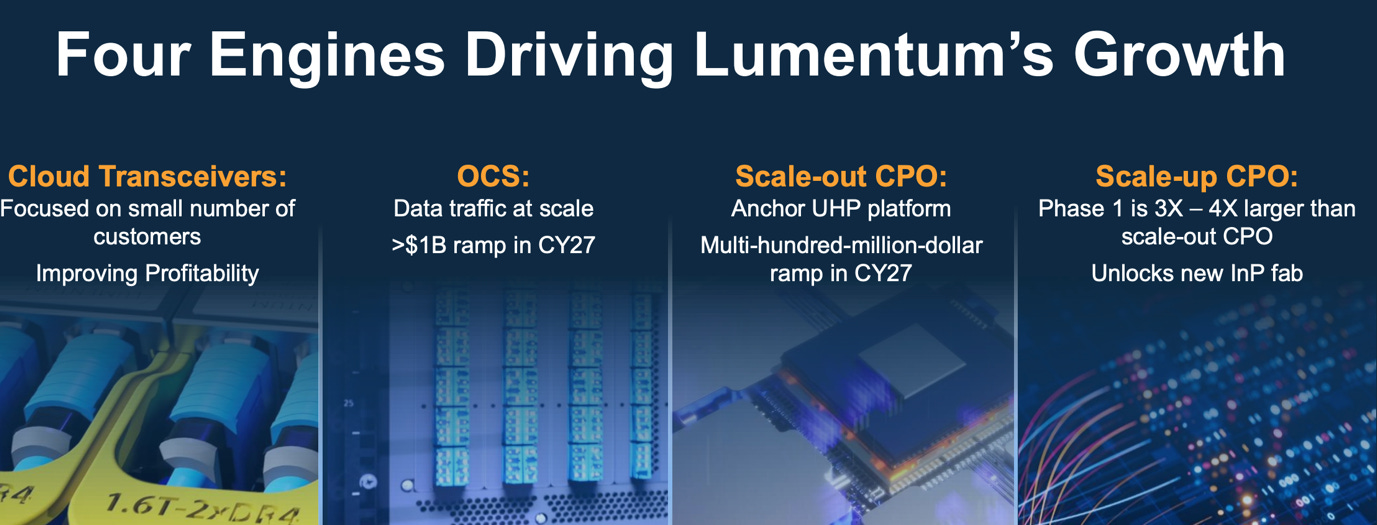

This shift is creating three major growth opportunities for Lumentum in:

Cloud Transceivers

Optical Circuit Switches (OCS)

Co-Packaged Optics (CPO)

4.1. Cloud Transceivers

Cloud transceivers are the devices that connect servers and switches in a data center.

They are like the ports that allow information to flow. Right now, the industry is moving from 800GB speed to 1.6TB (1.6 Terabits per second), which is twice as fast.

To make a 1.6T transceiver, a company needs very advanced laser chips.

Lumentum has a huge advantage here because it is the world leader in 200G-per-lane EML laser chips. You need eight of these chips to make one 1.6T transceiver.

Lumentum currently controls about 50% to 60% of the entire world market for these advanced lasers.

Analysts at Mordor Intelligence forecast that the Optical Transceiver market will grow with a 13.67% CAGR to reach $29.3B in 2031!

Because demand for these chips is much higher than the supply, Lumentum can charge higher prices and choose which customers to sell to. This makes the 1.6T transition a strong growth driver for the company for at least the next 5 years.

4.2. Optical Circuit Switches (OCS)

Optical Circuit Switches (OCS) are a revolutionary new way to route data.

In a normal network, data has to be turned from light into electricity, sorted by a computer, and then turned back into light to be sent to the next server. This process is slow and uses a lot of power.

An OCS uses tiny, high-tech mirrors to bounce light directly from one fiber to another without ever turning it into electricity.

This technology is incredibly important for AI because AI data centers use massive amounts of power. Using OCS can reduce a data center’s power use by up to 40%. Lumentum’s OCS business has grown from almost nothing to a major revenue source in just 18 months.

Analysts at Mordor Intelligence forecast that the Optical Switches market will grow with a 9.54% CAGR to reach $12.7B in 2031!

As of early 2026, the company has a backlog of OCS orders worth more than $400M.

Management believes this will eventually become a $1B annual business as more companies like Google and Nvidia adopt the technology

4.3. Co-Packaged Optics (CPO)

Co-Packaged Optics (CPO) is the long-term future of AI computing.

Currently, transceivers are separate parts that plug into the outside of a switch or server. In the future, the optical lasers will be moved inside the machine and placed directly on the same chip as the main processor.

This allows data to travel even shorter distances, which saves even more power and makes everything faster.

Lumentum is a pioneer in this field. They have already received a multi-hundred-million-dollar order for CPO light engines, which are the specialized lasers used in this setup.

These products will start shipping in large numbers in 2027.

CPO evolves in stages:

First, Scale-Out Phase 0, optics are still separate from switches, with mostly copper connections.

Scale-Up Phase 1, optics move closer with more optical links, but copper backplanes remain.

Scale-Up Phase 2, systems use hybrid or mostly optical backplanes with optics tightly integrated alongside compute chips.

Each stage increases bandwidth and efficiency by replacing electrical connections with optical ones closer to the silicon.

We are currently in Phase 0, but quickly moving to Phase 1!

By being one of the first companies to perfect CPO technology, Lumentum is making sure that it will remain the primary provider of light for AI systems even after the current generation of transceivers is replaced, and the industry moves to the next stage.

5. Valuation

Lumentum’s valuation has climbed rapidly as the stock market realized the company’s importance to the AI world.

As of March 2026, Lumentum’s stock price was trading around $703 per share. This is a massive increase compared to early 2025, when the stock was trading under $100. Over the past 12 months, the stock has risen by approximately 1,027%, reaching a market cap of $50B.

Several key factors have caused this huge price increase:

The Nvidia Effect: In March 2026, Nvidia announced a strategic partnership and a $2B investment in Lumentum. This gave investors massive confidence that Lumentum is a winner in the AI race.

S&P 500 Inclusion: The company was added to the S&P 500. Not only a sign of trust, but also this meant that many large mutual funds were forced to buy the stock.

Record Earnings: Every quarter, the company has reported sales and profits that are much higher than anyone expected, leading to beat and raise cycles.

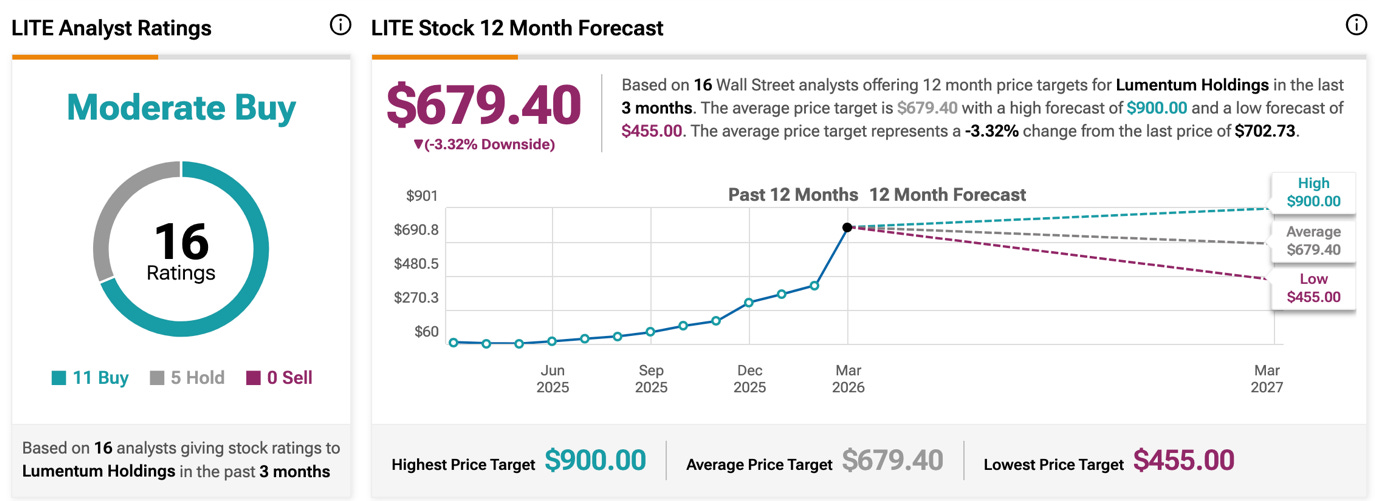

Looking at analyst price targets, the stock is currently seen as a Moderate Buy. Out of 16 ratings, 11 analysts say you should “Buy” the stock, and 5 say you should “Hold” it.

None of the analysts is currently saying you should “Sell” it.

The average price target from these analysts is $679.40, though some very optimistic analysts think it could go as high as $900.

5.1. Valuation Multiples and Comparison to Peers

Because Lumentum is growing so fast, it is often compared to other companies in the optical networking space, such as Coherent ($COHR) and Fabrinet ($FN).

Lumentum’s valuation looks high if you only look at the past, but it looks more reasonable if you take into account future growth expectations.

For example, its forward P/E ratio of about 60x is higher than Coherent’s 38 and Fabrinet’s 36. However, Lumentum is growing its revenue much faster (66% vs 17% and 36%).

This suggests that investors are willing to pay a premium for Lumentum because of higher future growth expectations.

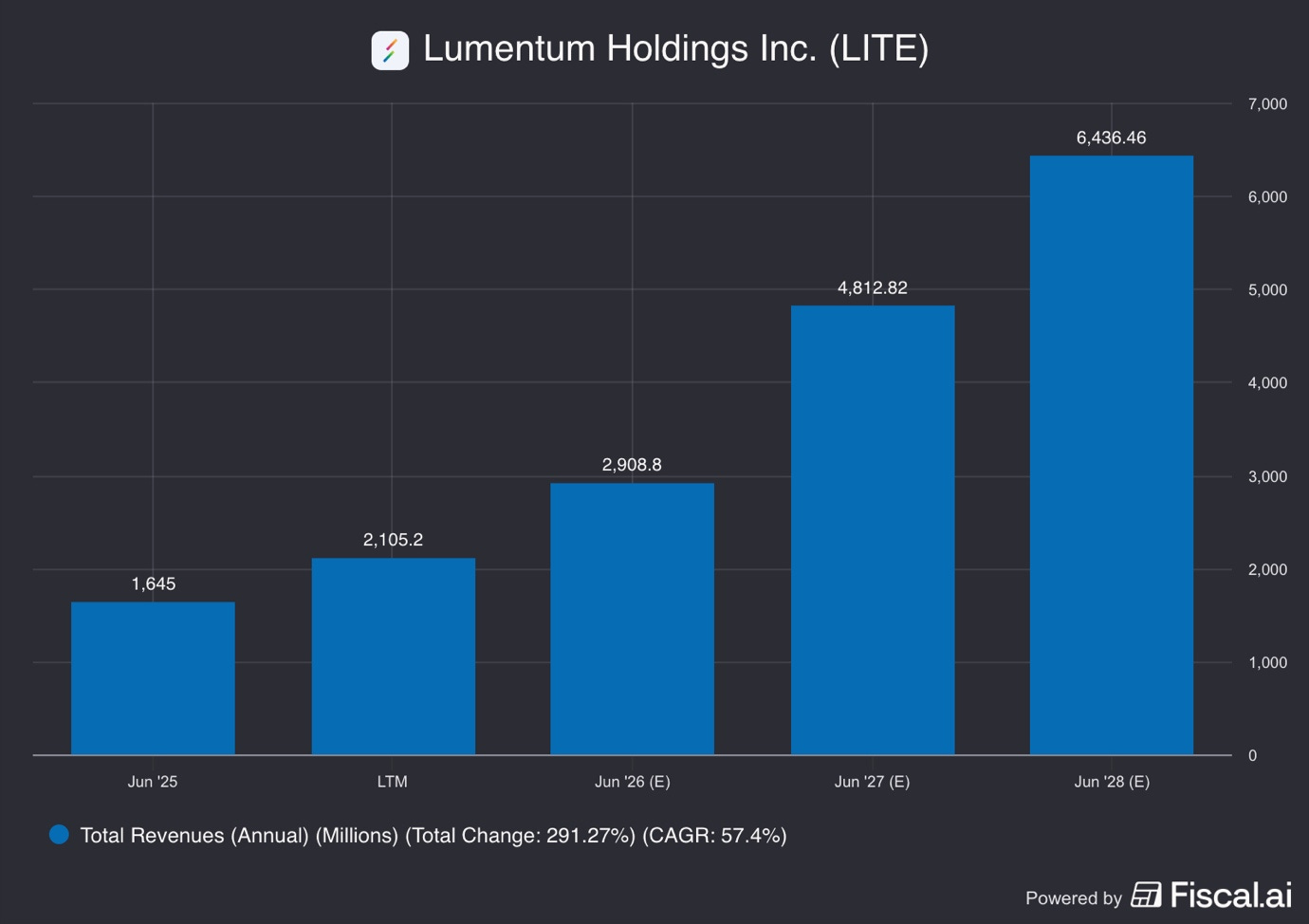

5.2. Analyst Growth Expectations

Analysts have become incredibly bullish on Lumentum’s future. They have been raising their earnings estimates for the company faster than for almost any other stock in the tech sector.

As you can see in the picture above, analysts expect the company’s annual revenue to grow at a CAGR of 47.4% between 2024 and 2028, with revenues reaching $6.4B.

Meanwhile, EBITDA and operating profit are also expected to reach $2.7B and $2.2B.

Taking these estimates into account, Lumentum trades for a 2028 P/E of 35.

While this is significantly lower than the current FWD P/E of 60, this is still a premium valuation. This means that Lumentum investors are betting that either the company will improve on these already healthy estimates or the growth could continue significantly past 2028.

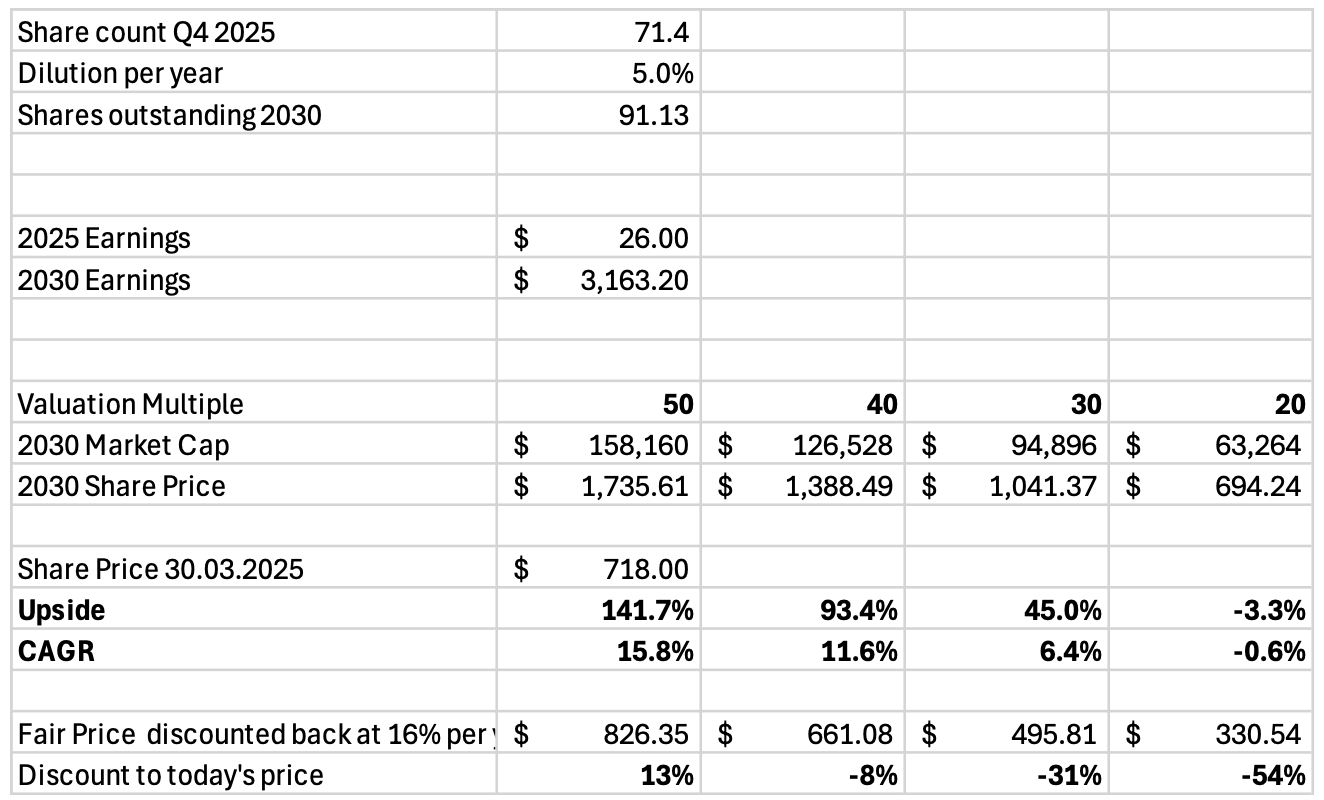

6. 2030 Valuation Model

To estimate what Lumentum might be worth by 2030, we can build a model based on the optimistic targets and market trends.

Key Model Assumptions:

I am modelling a 45% revenue CAGR. We assume the company can maintain a high growth rate, supported by the move towards its photononics products across the AI ecosystem.

Next, as the company scales up, its operating margins grow to a heathly 40%.

We get 2030 revenues of $10.5B and operating income of $4.2B!

This is a 541% and 2,443% increase from 2025 levels!

Next, I am modelling tax and other expenses at 25% of operating income.

The result is a net income of $3.16B!

In terms of dilution, I model the share count increasing by about 5% per year, reaching 91M in 2030.

Assuming an exit multiple of 40, we could be looking at a $1,338 stock in 2030, implying an upside of 93%!

Discounting that back at 16% per year to today, we get an estimated fair value per share of $661.

That is 8% above today’s share price of $718.

So this valuation model shows that Lumentum appears overvalued.

Thus, for the company to deliver meaningful upside to its shareholders, it needs to either grow faster than the 45% CAGR I modeled, has better operating margin than 40%, or a much higher multiple than 40.

If I increase the CAGR to 55%, the operating margin to 50%, and exit multiple to 45, the upside increases to 280%.

While that is certainly possible, considering the speed at which the AI industry is moving, I won’t be betting my money on it.

7. Conclusion

Lumentum has successfully transformed itself from selling photonics products to the networking and communications industries into a foundational engine of the AI boom.

By focusing on the most difficult and high-value parts of the optical network, the lasers and the mirrors that guide light, the company has built a competitive moat that is very hard for other companies to cross.

Its financial situation has improved dramatically, with revenue and profits now growing at their fastest rates in history. While the stock price has risen over 1,000% and currently trades at a demanding valuation, the underlying business is supported by real orders and massive customer demand. The partnership with Nvidia and the $400M OCS backlog are strong signals that Lumentum is a mission-critical partner for the world’s most powerful technology companies.

Furthermore, Lumentum represents a classic picks and shovels investment.

As long as the world continues to build more AI models and larger data centers, the need for high-speed optical connections will only grow. With its vertical integration strategy and lead in 1.6T lasers, Lumentum is better positioned than almost any other company to capture this growth.

While there are risks, such as high spending on new factories and potential increased competition, the overall trend toward light-based computing makes Lumentum a key beneficiary of one of the most significant technology shifts of the 21st century.

However, despite the fundamental qualities this company has, the valuation model clearly demonstrates that the company is very richly valued.

Even with generous growth assumptions of 45% revenue CAGR, 40% operating margin, and 40x exit multiple, the model found only 93% upside in the stock by 2030.

Essnetially todays investors are betting on the company delivering astronomical levels of growth.

So while the company could deliver a decent upside for today’s shareholders if everything goes better than I modeled, to me it seems that the bulk of the gains have already been made.

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 11 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.