Why Dilution is Not Always Bad!

Investing Basics #7

Dilution is a very important, yet often misunderstood, aspect of investing.

One of Warren Buffett’s most famous pieces of wisdom is that “investors must think as business owners”. One doesn’t own a “stock”, but rather “a piece of a business”. He encourages investors to think not about what will cause the stock price to increase, but what will drive the company’s earnings higher.

But crucially, as investors don’t own the whole business, they mustn’t forget about dilution.

Dilution refers to a company issuing new shares, thus increasing the total number of shares outstanding, reducing each share’s right to company earnings. Simply put, if Company A has 100M shares outstanding, an investor who owns 2M shares has rights to 2% of its profits. If in 10 years that company doubles its share count to 200M shares, those same 2M shares only have rights to 1% of the company’s profits.

Throughout his illustrious career, Mr. Buffett regularly talked of the importance of understanding dilution and not ignoring it. He criticised management teams and company boards for being careless when giving out equity as if it were free money.

“True, the share count doesn’t change when a company pays cash for an acquisition. But when a company issues shares, it is giving away a portion of everything it owns—its cash, its future earnings, and its management talent.” Warren Buffett

This change in paradigm transformed how millions of people view investing.

However, often I see that this thinking has gone too far, with investors instantly viewing any dilution in all cases as bad. I don’t believe that is the case, as in many cases, dilution is not only not bad, but actually crucial for growing the business.

So, in this Investing Basics article, I will explain to you why dilution is not instantly and always bad.

1. Dilution and EPS

Dilution is not necessarily bad for existing shareholders if it is used prudently to grow EPS!

Many investors are taking Warren Buffett’s quotes out of context without deeply analyzing what he meant by them. When they hear dilution, their first thought is “I own less now”. But that doesn’t have to be the case.

What actually matters is not how many shares exist or what percentage of the company you own. What matters is how much economic value each share represents.

If a company uses the funds generated from the sale of equity to grow EPS at a significantly faster rate than it could have without selling the equity, this sale of equity was not dilutive, even though the total number of shares outstanding increased.

Let’s return to the example of Company A from the introduction:

It is true that 10 years ago the shareholder owned 2% of the company, but now, because the total number of shareoustanding has doubled, the shareholder owns 1%.

However, this view ignores the EPS.

Let’s say that in 2015, Company A earned $100M in net income. 100M shares outstanding means EPS is $1, and the investor who owns 2M shares has rights to $2M of earnings.

In the next 10 years, Company A issued 100M new shares to fund growth, building a new factory, and hiring employees to develop new products.

This enabled Company A to grow net income from $100M to $800M.

200M shares outstanding means that EPS is $4. Now the shareholder with 2M shares has rights to $8M of earnings.

Despite the shareholders’ ownership decreasing from 2% to 1%, the value of his share of the company’s earnings increased by 300%.

Simply put, growth in the total number of shares outstanding must be strongly correlated with EPS growth. If that is the case, then the issuance of new shares is not economically dilutive to existing shareholders.

Shareholders own less of something, but if the overall pie is much bigger, then they own more.

An investor’s objective should be to have more kilograms of cherry pie on their plate, it doesn’t matter if it comes from 2 large slices or 10 small ones.

Issuing shares is no different than raising debt or reinvesting cash flow. It’s simply a way to fund growth. Whether it hurts or helps shareholders depends entirely on what management does with the capital.

A perfect example is Shopify.

From 2015 to 2020, the company grew the total number of shares outstanding by 53%. During this time, Shopify was unprofitable, making it difficult to secure significant non-dilutive debt financing. However, they needed billions of dollars to build their e-commerce platform.

Now the platform is built, EPS is growing at a stable rate, and dilution has slowed down.

While there were individual mistakes, with bad acquisitions, it’s hard to argue that the overall dilution strategy was unsuccessful.

2. Funding High ROIC Growth

Another justification to issue new shares is to fund high return on invested capital growth.

ROIC measures how effectively a company uses capital to invest in its business to generate operating profits. It is calculated by dividing net operating profit after taxes by invested capital.

(NOPAT/Invested Capital) where Invested Capital is Equity+Debt-excess cash.

When a company identifies an opportunity to invest in a project where the potential ROIC significantly exceeds its cost of capital, issuing shares to fund that investment is a mathematically superior decision for long-term wealth creation. Especially if they can’t raise capital in any other way.

Of course, this is where there is space for lots of debate, as it is impossible to tell what the ROIC will be beforehand. There is no guarantee that ROIC will be the same as for the earlier project, so it ultimately comes down to trust in the management. Investors need to independently assess if they trust the management that the ROIC will be high enough to justify the dilution.

Furthermore, some investors simply say, “Why don’t they just raise more debt?” Well, a company’s ability to raise debt is limited by its EBITDA. It is generally viewed that a business must maintain a debt-to-EBITDA ratio of around 3:1. Above that, it could become increasingly difficult to find willing lenders, and the cost of debt rises significantly. In such a scenario, it could be more financially sound to fund business expansion with equity raises, but only if the ROIC is high enough.

I think a good example to show this is Sofi.

During 2025, Sofi issued 2 convertible notes, raising over $3B in total. During both issuances, the stock reacted negatively to the offering. This is because, as a profitable company, Sofi was not expected to use dilution to fund its growth.

However, what some shareholders didn’t understand was that as a bank, Sofi can’t simply raise more debt, because of strict regulations. Any other business can essentially raise as much debt as they want if someone is willing to lend them (barring any loan covenants), whilst banks need to maintain a safe Tier 1 capital ratio so the government knows the money of ordinary depositors is not at risk.

I won’t overexplain, but essentially, Tier 1 capital is the minimum required reserves. By adding $3B to it, Sofi is strengthening its ratios way above the minimum government requirements. This allows them to issue significantly more loans using customer deposits, up to even 10x leverage of $30B.

Not all of the $3B will be used in this manner, this is just one example of what the company can do with this capital. So I don’t view this stock dilution as economically dilutive, because Sofi could use the capital to issue more loans, generating interest income, which will further compound, allowing them to issue more and more loans.

Simply put, this capital will fund high ROIC growth.

3. Rapid Growth

If a company has a great business model, with a large and growing total addressable market, it is not only acceptable to issue equity to grow, but it is recommended. A business that can deploy lots of capital to grow incredibly quickly benefits from:

Scale

Speed

First-mover advantages

Strenghtening moat

A larger company benefits from increased economies of scale as it is able to spread its cost basis over a larger output, reducing unit costs. Lower unit costs allow companies to reduce prices to capture more market share or have higher margins, leaving more profit for reinvestment. In certain circumstances, shareholders could be much better off if the company uses equity to grow and establish a strong position in a market, compared to a competitor’s shareholders that don’t.

In some situations, waiting to fund growth organically with FCF can actually destroy value if it slows expansion or allows competitors to catch up. This is why many of the best capital allocators are comfortable issuing shares when opportunities are abundant.

For instance, many high-growth industries, such as e-commerce, fintech, SaaS, consumer technology, and others, are often required to reinvest aggressively in R&D and market expansion long before they achieve profitability. In these instances, the ROIC may appear negative or low in the short term, but this is because the company is heavily investing in future growth. The underlying unit economics suggest massive future returns. Equity issuance provides the necessary runway for these companies to scale, allowing them to capture market share and establish competitive moats that would be unattainable through debt financing alone.

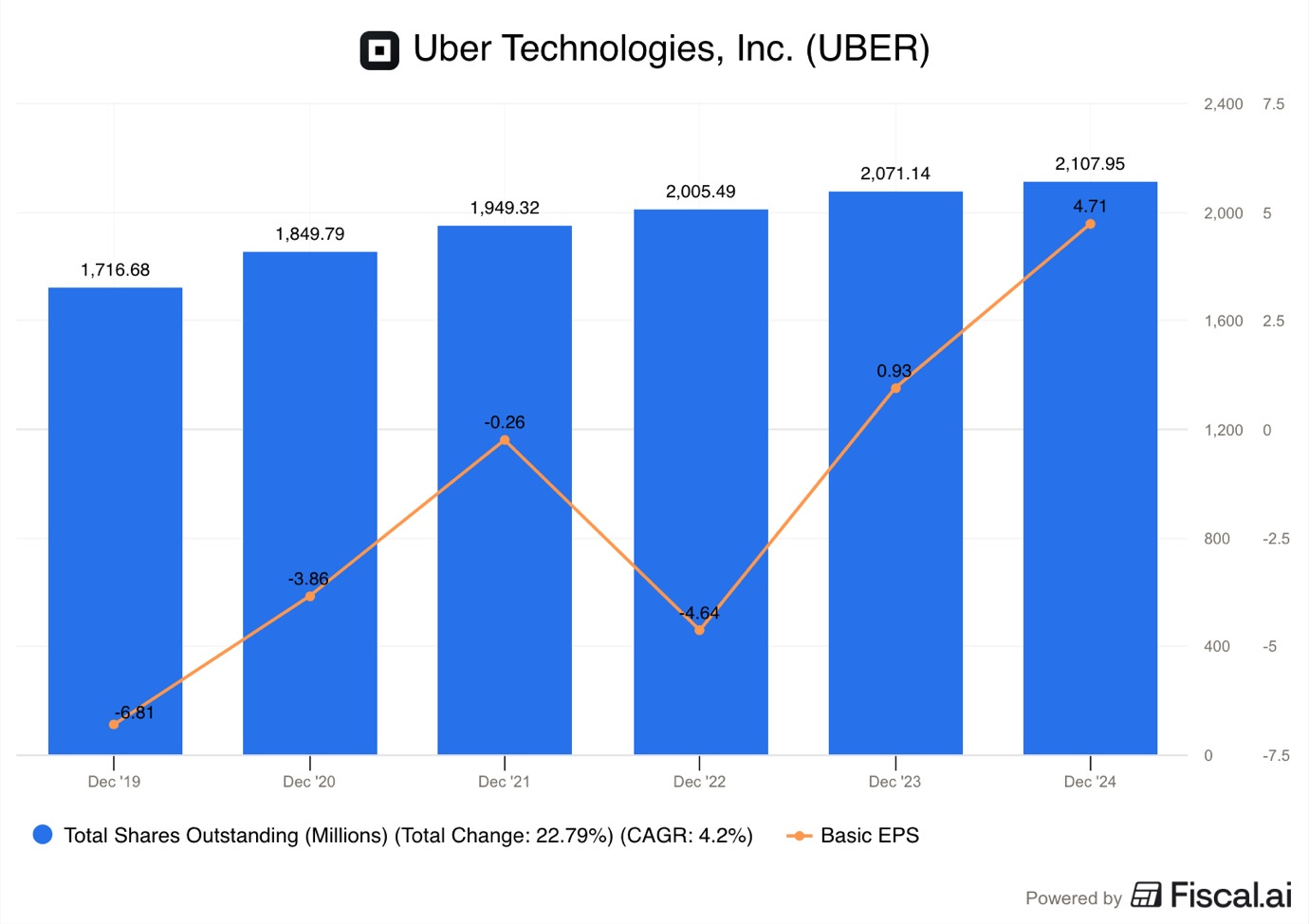

A clear example is Uber.

The company went public in 2019 and has since grown the total number of shares outstanding by 23%, yet at the same time, EPS has grown many times over.

Uber was unprofitable till 2023 and used equity to fund their operations. Today, they have established themselves as the ride-hailing and food delivery leader in the US, Canada, and much of Europe. This would not have been possible if they hadn’t used their equity as a funding mechanism.

4. When Dilution is Bad

That being said, I agree with the general sentiment that most of the time, stock dilution is bad. Most of the time is the key part of this statement, as it’s not the same as always.

It is true that many CEOs and management teams are often driven by ego instead of shareholder focus. Thus, investors must look at what the management is saying without rose-colored glasses.

Companies frequently economically dilute shareholders because of:

Terrible acquisitions

Excessive Stock-Based Compensation

BuyBacks

Mergers and acquisitions are a primary catalyst for share dilution, as acquiring firms often use their stock as currency to purchase targets. While a stock-financed deal immediately reduces existing shareholders’ ownership, it can create immense value through P/E arbitrage and strategic synergies.

However, unfortunately, most of the time, CEOs overpay, even if the target has a lower P/E.

The theory is that if the acquiring firm trades for a P/E of 30, whilst the target trades for a P/E of 10, the acquisition is immediately accretive to the EPS. While that is true mathematically, in year 1, in the long term, this thinking could prove disastrous. Most of the time, the market determines what P/E a company trades for based on its prospects. A 30 P/E company is growing faster than a 10 P/E company, which might be stagnating.

The acquiring company that gives up 5% of its 30 P/E equity to purchase a 10 P/E company might see an increase in EPS by 10% in year 1. But, if after 5 years, the EPS of the purchased company is flat, yet the acquiring company’s EPS has grown by 40%, this was a bad deal.

The acquiring company gave up 5% of its entire future earnings to purchase a business that is not growing.

Despite no EPS growth, this deal could, in theory, still be accretive to the EPS because of synergies. Yet often these so-called strategic synergies never materialise or are greatly exaggerated.

Another common way of shareholder dilution is share-based compensation.

SBC can be a great way to reward loyal employees, increase company morale, and attract highly sought-after talent. However, in recent years, there has been a growing trend of management teams and CEOs using SBC to enrich themselves at the expense of regular shareholders.

The most obvious and egregious example is the parent company of Snapchat, Snap.

Since 2017, Snap has paid more than $10B in SBC, increasing the total number of shares outstanding by 41%. Yet, EPS has gone absolutely nowhere.

Furthermore, one counterintuitive way in which companies destroy shareholder value is the activity of “countering dilution” with stock buybacks. There is a bit of a misconception that stock buybacks reduce dilution. Share repurchases reduce the number of shares outstanding, but they are still economically dilutive. Buybacks are money leaving a company’s wallet. This leaves less funds for investment, requiring companies to raise debt.

Doing stock repurchases to counter excessive SBC, or bad M&A, or create the appearance of shareholder benefits to then borrow money to fund operations might reduce the total number of shares outstanding, but this is incredibly economically dilutive.

Share repurchases are:

Economically accretive if the company buys shares below intrinsic value

Economically dilutive if it buys shares above intrinsic value

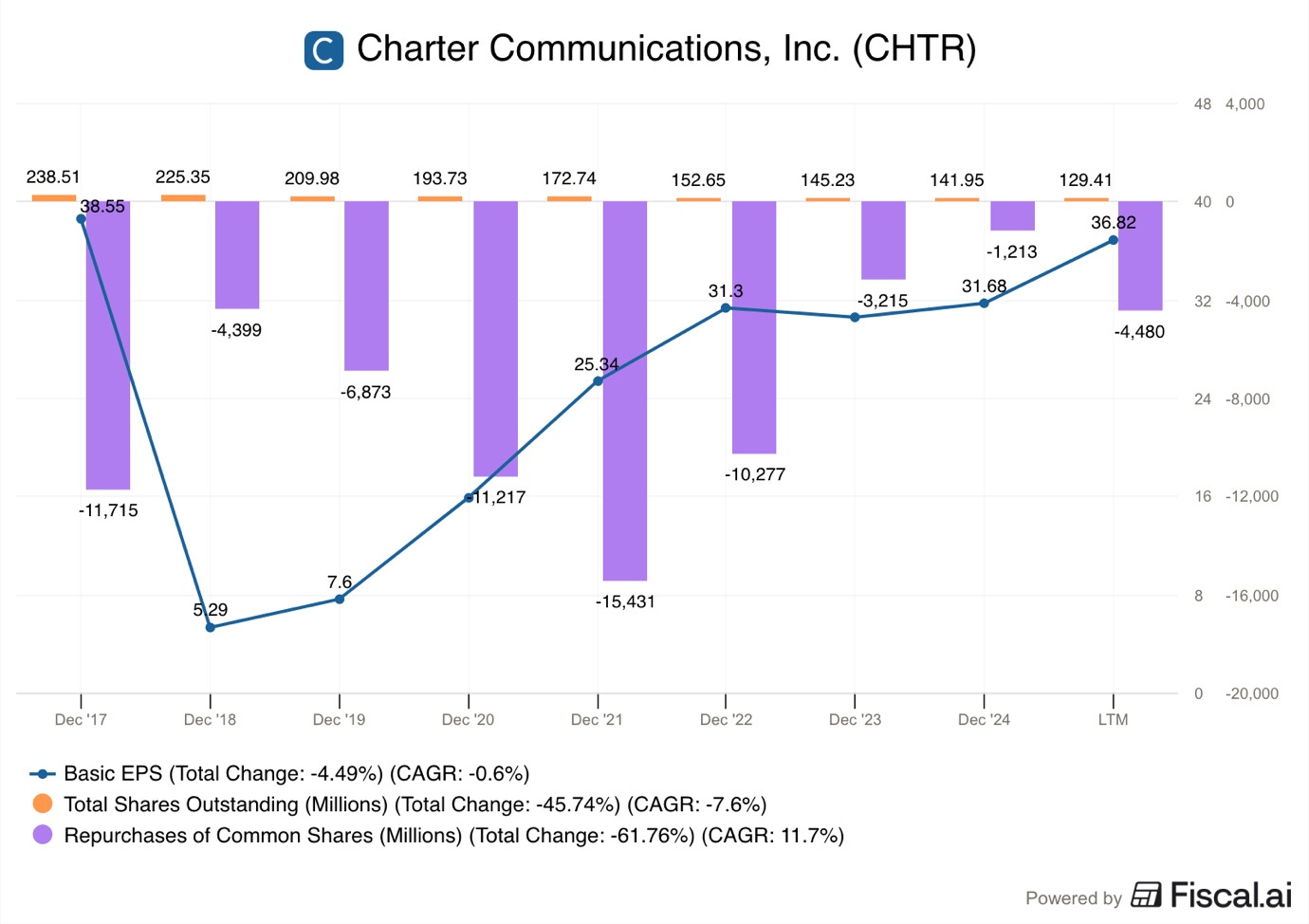

Since 2017, Charter has spent close to $70B on share repurchases to reduce the total number of shares outstanding by 46%. Despite this, EPS is down 4.5%.

For me, it is clear that these share buybacks were economically dilutive.

That might seem counterintuitive, as the share count went down. But what is the point of reducing the sharecount if EPS is not growing? Share repurchases can be incredibly beneficial as they increase the economic rights of a single share. However, if a company doesn’t grow EPS, it is meaningless.

You might have fewer but larger slices of cherry pie on your plate, but the overall weight of the pie on the plate is smaller.

If Charter had invested the $70B to build a new business, the total number of shares outstanding might be double what it is today, but EPS might be 2 or 3x higher than today. Because share repurchases increase EPS in the short term, the market loves them. This simple mathematical reality causes investors to:

Panic when companies issue shares

Cheer when companies repurchase shares

Even though, as the Charter and Sofi examples show, this reaction is not always based on long-term economic reality.

I prefer a thriving business like Sofi, that’s “diluting” shareholders by issuing shares to fund high ROIC growth, over a stagnating business like Charter that is “reducing dilution” with buybacks.

5. Conclusion

Is management turning dilution into more long-term value per share?

That is the core question that investors must answer when determining whether issuing shares to fund growth is justified. Ultimately, it all comes down to trust in the management.

Does the plan of the management team make sense?

If it does, then issuing equity to fund growth is justified.

Furthermore, shareholders need to understand that an increase or decrease in the share count doesn’t equal an increase or decrease in economic dilution.

Simply put, dilution only hurts shareholders when the capital raised earns low returns.

On the other side of the equation, reducing the number of shares outstanding using cash reserves or debt can be very economically dilutive if the company is underinvesting in its core business or not entering new ones.

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 11 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

This article comes at the perfect time. Understanding dilution is critical for long-term valuation.