Nebius $27B Meta Deal, $2B Nvidia Investment, and Tavily.

Ready to Service the AI Demand!

March is not finished yet, but it is safe to say that it has already been one of the most eventful months in Nebius history.

First, on March 11, it was announced that Nvidia is investing $2B in Nebius.

Then, yesterday on March 17, Nebius signed a monster $27B deal with Meta.

This comes after the company spent $275M to acquire the agentic AI start-up, Tavily, in February.

These 3 events were important, so I decided to write this article and look at them in a little bit more detail.

Let’s dig in.

1. $2B Nvidia Investment

When the AI revolution began in 2022, it quickly became clear that Nvidia is the biggest beneficiary. Demand for their GPUs exploded as Meta, Google, Amazon, and Microsoft raced to participate in the AI battle.

Thanks to this incredible demand, Nvidia now has $62.6B of cash on its balance sheet!

Rather than letting this cash just sit in the bank, Nvidia has made a series of strategic investments, with the aim of increasing demand for its products and driving further innovation in the AI industry.

As Nebius has a good relationship with Nvidia and exclusively uses their GPUs, Nvidia decided to take this relationship a step further by investing $2B in the company!

As part of the deal, Nebius targets the deployment of 5GW of Nvidia chips by 2030. Additionally, Nebius is given a strategic allocation of Nvidia’s next-generation Vera Rubin chips and will collaborate with Nvidia about AI server rack design.

Nvidia is now a holder of warrants equivalent to roughly 21M shares of Nebius, giving them about 8.3% stake in the company.

The $2B amounts seems to be the sweet spot for Nvidia when they make strategic investments. The company has invested $2B in Coherent and Lumentum, the developers of optical networking components for AI clusters.

Moreover, Nvidia also invested $2B in CoreWeave, Nebius direct competitor.

There are 3 key reasons why I believe Nvidia invested in Nebius:

Securing long-term demand

Countering the moves of Hyperscalers towards internal chips

Increasing geographic diversification

The strategic investing model has become a key strategy of Nvidia to secure long term GPU demand and reduce demand for AMDs chips.

By providing capital to neoclouds like Nebius and CoreWeave, they ensure these companies have the liquidity to purchase billions of dollars worth of their newest chips. Without these investments, Nebius might decide to build data centers based on the AMD chips. Such a scenario now becomes increasingly unlikely, and that solidifies Nvidia’s moat and technological advantage over AMD. Critics suggest this creates a synthetic demand loop that may inflate demand.

However, from Nvidia’s perspective, these investments diversify the customer base.

When a business sells its products only to a small number of customers, it becomes dependent on them and gives up leverage. If traditional Hyperscalers (Microsoft, Google, Amazon) demand better terms, Nvidia can reject that with threats of selling more chips to Nebius.

Furthermore, Hyperscalers are increasingly developing their own AI chips to reduce their reliance on Nvidia.

By funding independent specialized clouds, Nvidia maintains a direct channel to AI-native startups and enterprises that do not want to be locked into the proprietary hardware of a specific hyperscaler.

Also, while Nebius is rapidly developing data centers in the US, they are an Amsterdam-based European company with a strong presence in Israel. Additionally, they recently hired a Singapore-based team to expand in Asia.

Thus, this deal also helps Nvidia diversify the demand geographically.

Nebius is also a key participant in efforts to modernize European infrastructure, working with the European Commission and partners like Accenture to establish sovereign AI Factories across the continent. The European Union is notoriously pathetically slow at everything that matters. They are grossly behind in AI, but there are hopes in the European AI community that this could change. If the EU does get its act together, with this $2B investment in Nebius, Nvidia has secured a strong pathway through which to build its presence in this region.

But this arrangement is not only a win for Nvidia, as in addition to capital, there are also other benefits to Nebius:

Technical collaboration

Vera Rubin allocation

Validation of Nebius to clients

The relationship extends to a deep engineering collaboration across the entire AI stack.

Nvidia and Nebius are collaborating on the co-design of AI factories, providing Nebius with access to proprietary partner design materials, early hardware samples, and system software support.

This collaboration focuses on optimizing fleet management through Nvidia’s latest GPU health monitoring tools and building a best-in-class inference and Agentic AI stack. Such technical integration allows Nebius to achieve higher GPU density and superior thermal management. This is not something that a simple reseller could do.

This is also a slight strategic advantage over Iren and Coreweave, who typically buy standard AI servers from vendors like Supermicro and Dell. Nebius, however, co-designs the actual server racks with Nvidia. However, this advantage is not large enough to overcome scale and high energy costs if a data center is small or built in an expensive area (Iren’s core strength).

But most importantly, this collaboration is crucial if Nebius wants to have any shot at all to compete with Hyperscaler clouds like AWS, Google Cloud, Azure, and Oracle.

As part of the agreement, Nebius will be an early adopter of Nvidia’s next-generation Vera Rubin platform.

Vera Rubin architecture is specifically engineered to eliminate communication and memory bottlenecks that hinder fast AI processes. The platform integrates several breakthrough chips that will be deployed at scale across Nebius’s global data center footprint starting in early 2027.

Nebius priority allocation from Vera Rubin clearly signals that Nebius is being treated as a priority partner with early access to cutting-edge compute, which is scarce and highly strategic.

That matters because in AI infrastructure, getting the newest GPUs early directly translates into attracting top customers and higher-margin workloads, giving Nebius a chance to compete despite being much smaller than rivals.

Lastly, this validates Nebius strategy and tech stack in the eyes of Nebius clients.

I am certain that Nebius sales team is already talking about early access to the Rubin and Nvidia partnership in sales calls.

2. $27B Meta Deal

While the deal with Meta was likely in the works for months, as such agreements are difficult to negotiate, Nvidia’s $2B investment, strategic partnership, and Rubin allocations were likely crucial factors that convinced Zuckerberg that Nebius is the real deal.

This deal agreement is structured in 2 tranches:

$12B of dedicated capacity

$15B of optional capacity

The foundational element of the deal is a $12B commitment for dedicated AI compute capacity.

Under this supply agreement, Nebius will provide Meta with massive, localized GPU clusters for Meta’s exclusive use.

Typically, Cloud customers share GPUs with other Nebius customers. Meta won’t be sharing any GPUs with other customers and will be physically separated from GPUs used by other Nebius customers.

Dedicated GPUs provide Meta with consistency, full performance, low latency and stronger security, since no other users are competing for GPU compute. Shared GPUs are cheaper but can suffer from variable performance, making them less reliable for demanding or workloads.

Delivery of this capacity is scheduled to begin in early 2027, marking one of the first and largest commercial deployments of Nvidia’s Vera Rubin architecture.

This dedicated tranche ensures that Meta’s internal research teams, particularly those working on the Llama 4 and Avocado foundational models, have guaranteed access to the best AI chips in the world.

The remaining $15B of the contract value is structured as a commitment for Meta to purchase additional available compute capacity across upcoming Nebius clusters.

This tranche contains a clever monetization mechanism as Nebius intends to market this capacity to third-party enterprise and startup customers first, where it can get higher retail margins.

Meta serves as the guaranteed backstop, committing to purchase any remaining capacity that is not absorbed by the broader market. For Nebius, this provides a revenue floor of up to $27B, significantly de-risking its aggressive $20B capex roadmap for 2026.

Essentially, Nebius has secured the right to shop around to see if they can get a higher price or better payment terms. If they can’t find someone willing to pay more than Meta, the capacity will go to Meta.

This is clearly a sign that Meta has such strong demand for compute that Nebius had the upper hand to get this carveout.

Nebius doesn’t want to give up all its capacity to one client, as they are also focused on building their AI Cloud that competes with AWS, Oracle, Azure, and Google Cloud.

2.1. Profitability?

Unfortunately for us analysts, Nebius is not very forthcoming with contractual details. We don’t know how many MW this contract is for, how many chips are to be used, the price per hour, the price per MW, or whether Meta will pre-pay or not.

Such secrecy is understandable, as the industry is very competitive and there are many parties involved!

Nebius doesn’t want to publicize the price per hour that it charges Meta, as its wholesale price is likely significantly lower than the retail price. Revealing it could put downward pressure on retail prices.

At the same time, Meta doesn’t want others to know how much they are pre-paying, so that other cloud deals that they sign don’t ask for the same.

Also, Nvidia doesn’t want other customers to know on what contractual terms they are selling Rubin chips, because they could demand similar terms. We don’t know about bulk discounts or whether Nvidia is providing any vendor financing or generous payment terms.

My guess is that all these terms are very generous to Nebius, as Nvidia wants them to succeed to become large purchaser of Nvidia chips.

Nebius is still early in its journey and is capital-constrained, by providing generous payment terms, it would greatly help them. But that’s all it is, a guess. But we can go to Nebius financial filings and management statements to find some clues.

“How are we going to finance the CapEx?

So obviously, we will first finance it from our cash flows…

But most importantly…..we will continue to receive cash in 2026 from the favorable terms of our long-term contracts.

This cash flow will actually finance the majority, actually around 60%, maybe even more, of all of our CapEx needs in 2026.

So how are we going to finance the remaining amount?

As of today, we don’t have any corporate level debt.

We don’t have any asset-backed financing,

We don’t have any bank revolver”

Ofir Naveh, Chief Operating Officer of Nebius, Q4 2025 Earnings Call.

So, as Ofir says, 60%+ of capex will come from “the favorable terms of our long-term contracts” and the rest from contracted cashflows and conventional financing.

In Q4 2025, Nebius collected $1.6B from deferred revenue.

This is revenue that customers have already paid for, but Nebius has yet to deliver the service to recognize revenue. Simply put, these are customer pre-payments. The balance sheet further categorizes it with $1.3B is listed as non-current and $0.3B as current. This means that from the $1.6B that Nebius collected, it plans to recognize $0.3B as revenues in the next 12 months.

So the vast majority of this pre-payment was for services that will be recognized in 2027!

This demonstrated that the demand is so strong that Nebius is able to receive significant payments from customers more than a year before delivering services to them.

We also see a large spike in accounts payable, going from $228M to $1.2B. Many analysts have interpreted that “favorable terms of our long-term contracts” quote as pre-payments, but it also clearly means vendor financing and attractive payment terms.

If Nebius can receive early payments from customers while simultaneously delaying payments to suppliers, it can drastically reduce immediate cash requirements!

Nebius is essentially getting interest-free loans from both its supplier and the customer. It helps smooth out cash outflows, reduces interest costs, helping Nebius to scale quickly.

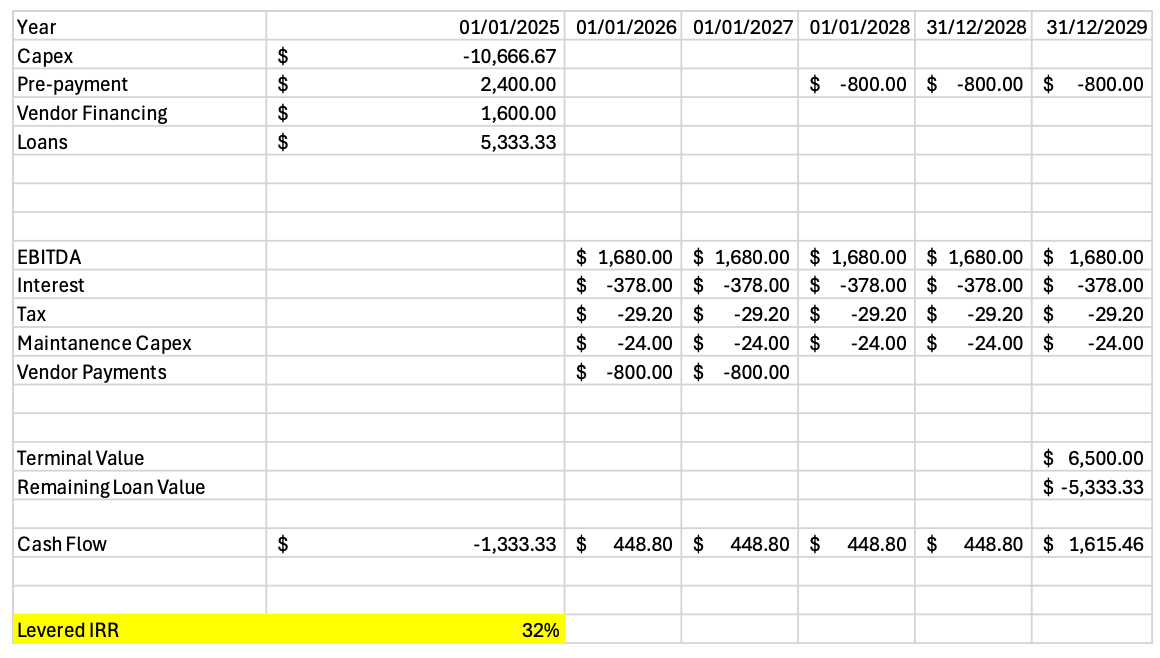

As we don’t have any concrete figures, I will have to speculate using back-of-the-napkin math and my own estimates to calculate how profitable this agreement could be.

Modeling about $10.7B in capex requirements.

Assuming 70% EBITDA margin, the $12B part could generate about $1.68B in EBITDA per year.

1 year service $2.4B pre-payment from Meta, credited towards years 3-5.

24-month vendor financing of 10% of capex, around $1.6B.

Conventional bank loans of $5.3B, about 50% of capex, at 7% interest rate.

Loans refinanced at the end.

Terminal value of $6.5B.

I get levered IRR of about 32%.

That seems decent to me. But granted, this model is very sensitive to terminal value, pre-payment size, vendor financing, and loan amount.

Lastly, we don’t know if the Meta agreement is pure bare metal GPU rental or if Nebius is also providing some kind of cloud software. If they do, that could drastically improve margins.

Meta is not Microsoft, they don’t have as much experience in running cloud software and are more likely to use various software solutions that Nebius offers.

3. Tavily Acquisition

The Tavily acquisition is meant to strengthen the value proposition of Nebius.

Tavily is an Agentic AI start-up that serves as the eyes of the AI agent.

The company provides integrations for data crawling, designed especially to make it easier for AI agents to process information and find exactly what they are looking for.

Traditional search engines are designed for human browsing, optimizing for visual layout. In contrast, Tavily’s engine is optimized for machine ingestion, returning structured content that is pre-filtered for relevance and formatted for Retrieval-Augmented Generation (RAG) pipelines.

RAG pipelines are AI systems that combine a language model with a retrieval step, where the model first searches external data (like documents or databases) and then uses that information to generate more accurate, up-to-date responses. This approach improves factual correctness and reduces hallucinations by grounding the model’s output in real, relevant sources.

")

According to Grand View Research, this corner of the AI industry is projected to go from $0 in 2020 to about $11B in size by 2030!

In a RAG pipeline, you have to retrieve the data, augment it by attaching it to the prompt, and generate the LLM answer.

Tavily specifically handles the retrieval step as it searches the web or data sources, returns relevant, structured results optimized for LLMs.

Simply put, this technology is crucial for AI agents because it allows them to access reliable an up to date information instead of relying only on training data.

This makes agents more accurate and enables them to handle more complex tasks across various domains. Nebius acquired Tavily to integrate this high-quality AI retrieval capability directly into its AI stack, enabling customers to build more powerful and accurate agents.

4. Implications

I think the biggest implication is that Nebius is clearly positioning itself to challenge Hyperscaler clouds for AI compute demand!

The Nvidia deal not only gives them $2B of capital but also additional integrations with the world’s best AI chip company to maximize performance. For bare metal GPU providers that might not be as crucial, but for AI clouds that run their own software, it is. Getting the most out of each GPU is paramount if one wants to have a leading AI cloud business.

Ultimately, the price per hour of GPU rental is not the only factor that determines the end user’s total AI compute cost. The real cumulative all-in cost of AI compute is driven by the time to result. How quickly can customers achieve their goals with GPUs?

Nebius is working to build an ecosystem that delivers a superior time to result.

This is what the acquisition of Tavily is about.

Faster training, quicker iteration, and better AI models sooner.

Faster inference, that leads to a better user experience.

Tavily aims to achieve just that by helping AI models navigate vast data sets.

Another implication is that Nebius is likely to become a major partner for Meta.

Meta is desperate for AI compute, and Nebius is a great source of conflict-of-interest-free compute. While Meta works in some way or another with AWS, Azure, and Google Cloud, the truth is that Meta competes heavily with these companies in various domains.

It would rather not finance its own competition, and Nebius provides them with that option.

If you are interested in a Detailed Nebius 2030 Valuation Model, you can find it below:

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 12 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

Great article Ray. I saw the list of 50 companies you have done research on. Is RMBS on your list. It’s quite a unique storage play and I think is flying under the radar but not for long I suspect.