One Stop Systems: Enabling Military and Physical AI!

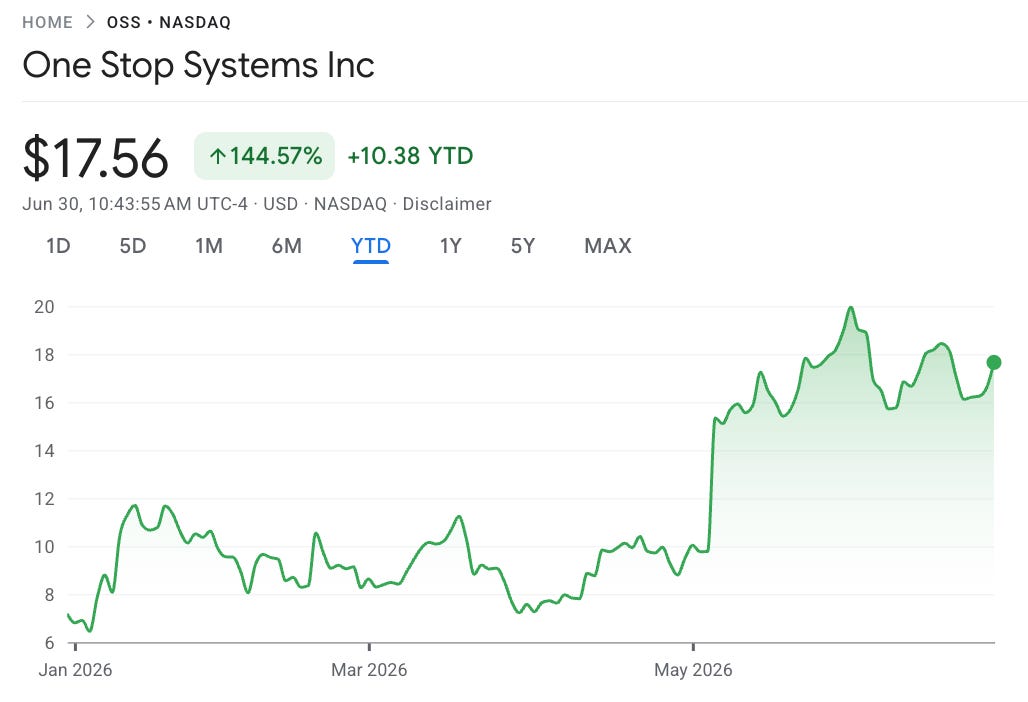

Stock is up 146% YTD as investors seek Physical AI companies.

So far, AI infrastructure spending has been concentrated in data centers.

Companies like Nvidia, Microsoft, Amazon, and Google have driven demand for dense GPU servers operating in huge, stable, climate-controlled data centers.

While the majority of the AI demand will indeed be served from these purpose-designed data centers, there is a large and growing subset of the AI industry that cannot be served from these on-the-ground data centers.

And that is Physical and Military AI.

The next stage for AI is moving out of the data center.

Instead of sending sensor data back to the cloud, organizations increasingly need AI to run at the edge, where decisions must be made quickly, and internet connectivity cannot be guaranteed.

This is where One Stop Systems (OSS) operates.

The company purchases Nvidia AI chips and modifies them to work on planes, tanks, submarines, and wherever else its clients need them to work. This is not all, as the company has a large and growing portfolio of products and services that enable AI and advanced sensors to work in other difficult/rugged environments.

OSS estimates the global TAM for rugged compute at $17B.

The defense industry has only recently begun a multi-decade procurement cycle to prepare itself for the age of AI.

In this OSS equity Deep Dive, I will examine the company’s business model, its growth opportunity, finances, and, as always, conclude with a valuation model.

Let’s begin.

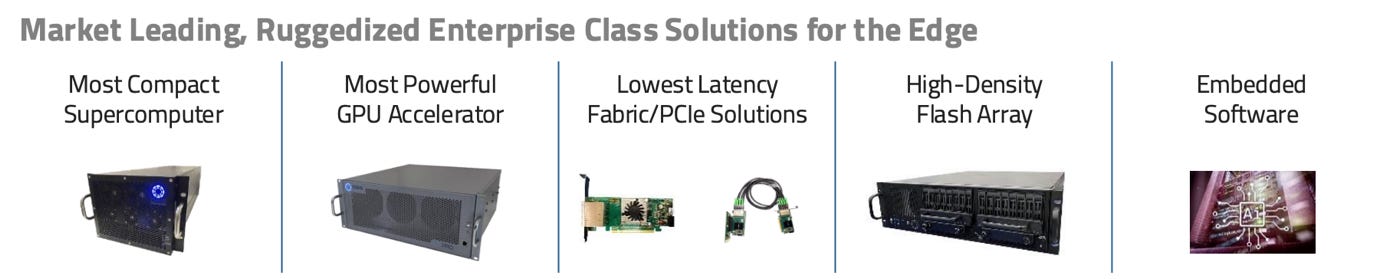

1. Key Products

2. Business Model

3. AI Growth Opportunity

4. Financials

5. Valuation Model

6. Conclusion

1. Key Products

I hope that after reading many of my equity reports by now, it is clear that running powerful AI models requires massive computing power.

AI requires many physical components to work together, such as GPUs, CPUs, memory, networking, cooling, and more.

In a data center, keeping these components safe is simple because they reside in quiet, air-conditioned rooms.

However, only delivering that computing power through the internet is not always possible or desired. Especially in situations where stable internet access might not be possible.

Military operations happen in some of the most punishing environments on Earth. Computers are bolted inside moving tanks, Navy warships, fighter jets, drones, and submarines.

In these environments, standard AI servers fail immediately due to physical stress.

To deliver AI under these conditions, systems must be heavily modified to handle:

Vibration and shock

Environmental factors

Very high and very low temperatures

Power conditioning

Military installations and equipment encounter rough terrain, waves, or high g-forces.

The physical chassis must be built from rugged aluminum, using mechanical hold-down bars to lock cards in place and specialized dampening mounts to absorb physical shocks.

Additionally, systems must be sealed against dust, sand, and wet conditions so that particles do not clog electrical connections.

Furthermore, computers must operate in freezing cold temperatures as low as minus 20 degrees Celsius or intense heat up to 50 degrees Celsius. This requires specialized thermal management like sealed liquid-cooling blocks.

Lastly, military vehicle generators produce erratic electrical currents. Custom power supplies are needed to clean the power and protect the delicate and expensive computer chips.

In the industry, such tough environments are called rugged.

Modifying commercial high-performance parts to survive these physical threats is the core business of One Stop Systems.

1.1. Ruggedized Short-Depth Servers

Standard data center servers are long metal boxes.

In such data centers, server racks are uniform, they are about 19 inches wide and anywhere from 30 to 36 inches deep. They sit in massive, climate-controlled rooms with plenty of space behind them for cables and airflow.

Vehicles like naval ships, fighter jets, trucks, and submarines do not have 3 feet of depth to spare.

If you try to jam a standard data center server into these environments, it literally sticks out into the hallway or blocks a door.

OSS solves this problem by designing Short-Depth Servers (SDS) that are only 20 inches deep, shrinking the length of a high-performance server by over 30%.

The company compressed and packaged enterprise-level AI capabilities into a footprint small enough to fit inside a standard equipment closet or a vehicle hull.

The flagship Gen 5 SDS is a highly compact system built from rugged, lightweight aluminum, weighing 45 lbs.

This compact machine enables data center-level computing speed for edge use cases.

It supports up to 5 Nvidia H100 GPUs, 16 high-speed NVMe storage drives, and high-power AMD EPYC processors running up to 400W.

Because the box is small, components are packed tightly together. OSS designs specialized physical boards and high-speed PCIe circuits that allow the GPU and CPU to transmit data instantly without creating massive interference or choking on data bottlenecks.

The SDS platforms incorporate 2 key features designed specifically for high-risk military and defense missions:

Removable storage canisters

Secure single-command erase

Removable storage canisters are tough, hot-swappable canisters that hold up to 1 petabyte of solid-state storage. Military missions require swapping data fast. If a surveillance plane lands after an 8-hour flight, technicians don’t want to plug in cords to download data.

Soldiers can pull these canisters out in seconds to transport recorded sensor data.

They pull a physical handle, pop out a canister containing all the terabytes of recorded data, slide a fresh one in, and the plane takes off again.

Moreover, let’s not forget that the security of military information is paramount.

If a military vehicle is in danger of capture, a soldier can trigger the secure data erasure command with a single command or immediately wipe all classified data, physically destroying the encryption keys.

The commercial potential of this product was demonstrated this June, when OSS announced an initial $8.4M contract from a leading defense company. Under this contract, the company will deliver 91 high-performance 3U SDS units to process large volumes of signal surveillance data and AI models to run real-time data.

Instead of beaming messy, raw battlefield radio waves, radar signals, or video feeds back to a cloud server in Virginia (which could easily be jammed by the enemy), the 3U SDS sits right there on the deployment platform.

It runs local AI inference models to filter out the noise and detect hostile communication frequencies.

This gives commanders immediate, split-second situational awareness without needing an internet connection.

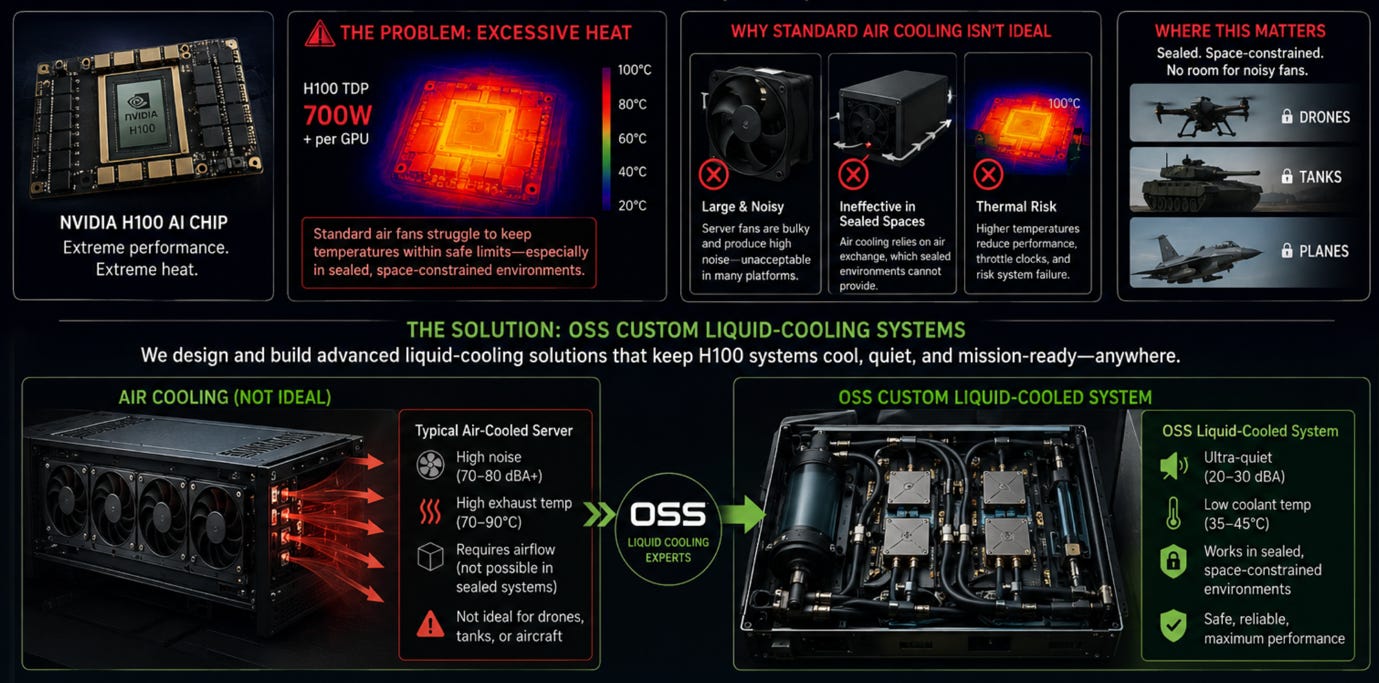

1.2. Liquid Cooled Enterprise Solutions

To run high-end AI inference, you need massive processing power. The problem is that Nvidia’s H100 AI chips generate a lot of heat that standard air fans cannot always safely cool down.

For example, in a sealed drone, tank, or plane, you cannot use those massive and noisy server fans.

For extreme environments, the company designs liquid immersion-cooled systems.

The system uses a pump to circulate liquid coolant directly over the hot processor surfaces. The liquid absorbs the heat and carries it to a radiator, which allows the chips to run at top speeds without slowing down.

This involves submerging the entire computer directly into a tub of specialized fluid that does not conduct electricity. The fluid absorbs heat from all components simultaneously.

OSS won a contract to supply a liquid immersion-cooled storage server to a US Intelligence AI project.

On the commercial side, the company received a $300,000 prototype order from a major commercial vehicle manufacturer to design a rugged liquid cooling system for Level 4 autonomous trucks. This system integrates a coolant pump, chiller, and custom control firmware to cool the advanced driver-assistance computing systems mounted on the back of the truck cabs.

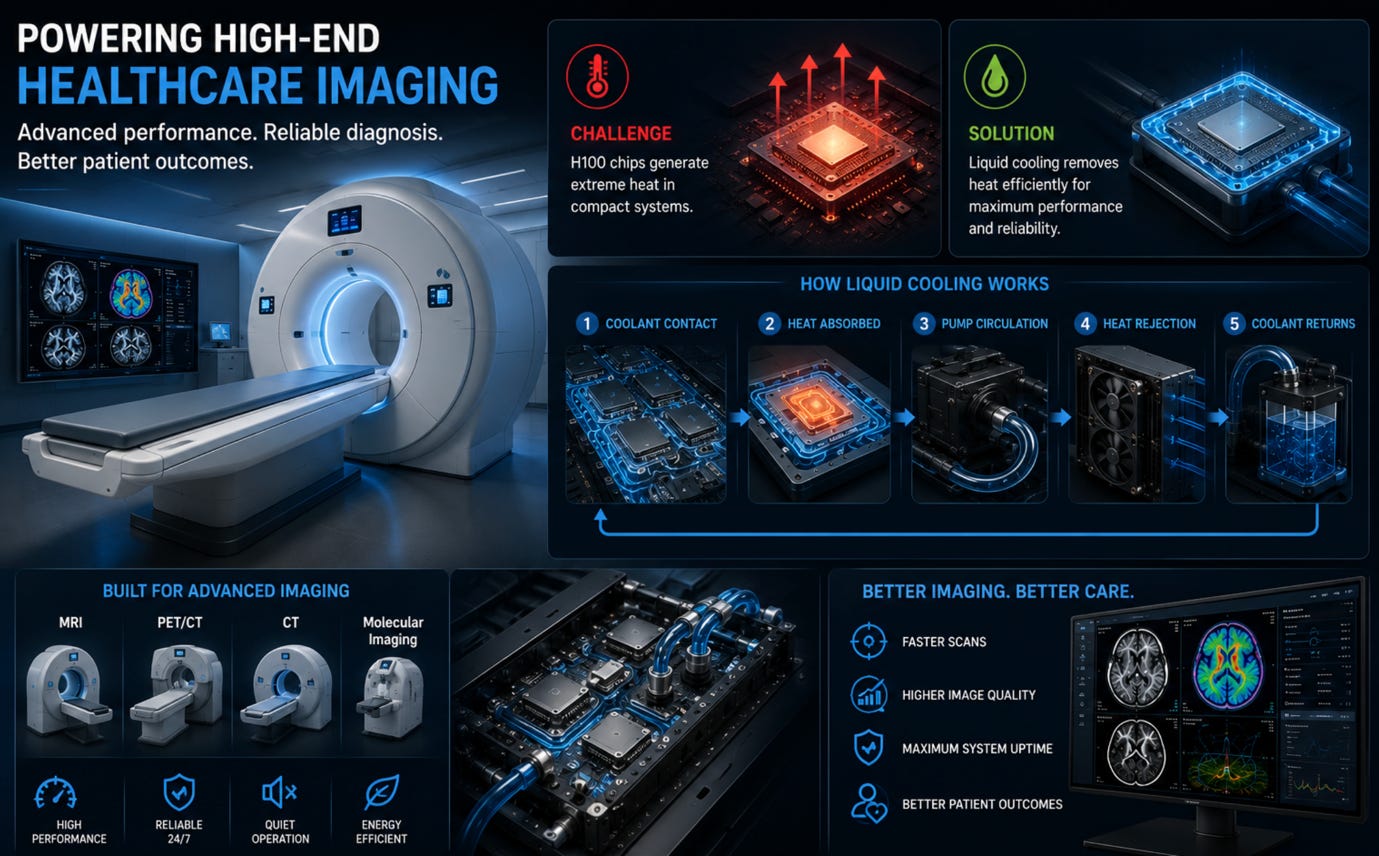

Another major application is high-end healthcare imaging.

Advanced medical scanners process thousands of high-resolution images every second, relying on AI to map out human tissue or catch anomalies.

In certain instances, hospitals prefer these machines to process data instantly and locally right next to the patient, rather than sending data to the cloud or server.

OSS liquid-cooled server modules slip right inside the chassis of MRI and CT equipment. Because liquid cooling eliminates the need for loud, roaring server fans, the computer runs in absolute silence, an important requirement for calm clinical hospital settings.

1.3. Flash Storage and Sensors

OSS also provides products that handle the brutal mechanics of high-speed data acquisition in tough environments.

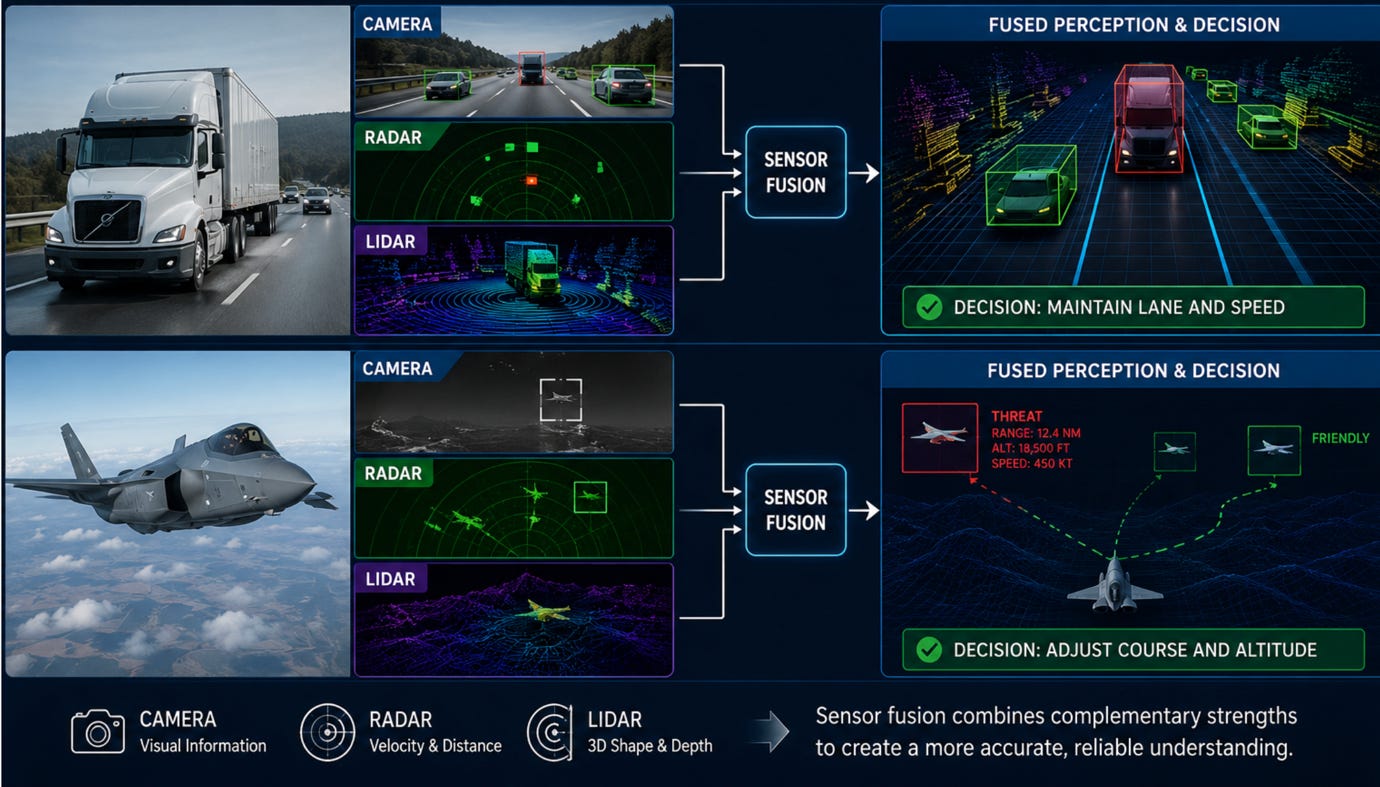

Self-driving trucks and military aircraft must make immediate decisions by combining data from cameras, radar, and other scanners.

This process is called sensor fusion.

Sensor fusion creates continuous streams of data that must be saved instantly without latency.

If a plane has 10 cameras, radar, and various sensors all running at the same time, it creates a massive amount of digital data, sometimes reaching gigabytes per second. If the storage drive inside the plane is too slow, the system chokes, drops frames, and the AI models become useless.

OSS designs strong storage using solid-state memory, which has no moving parts and does not break during heavy vibration.

This system collects this data, encrypts it in real time, and passes it to the AI server.

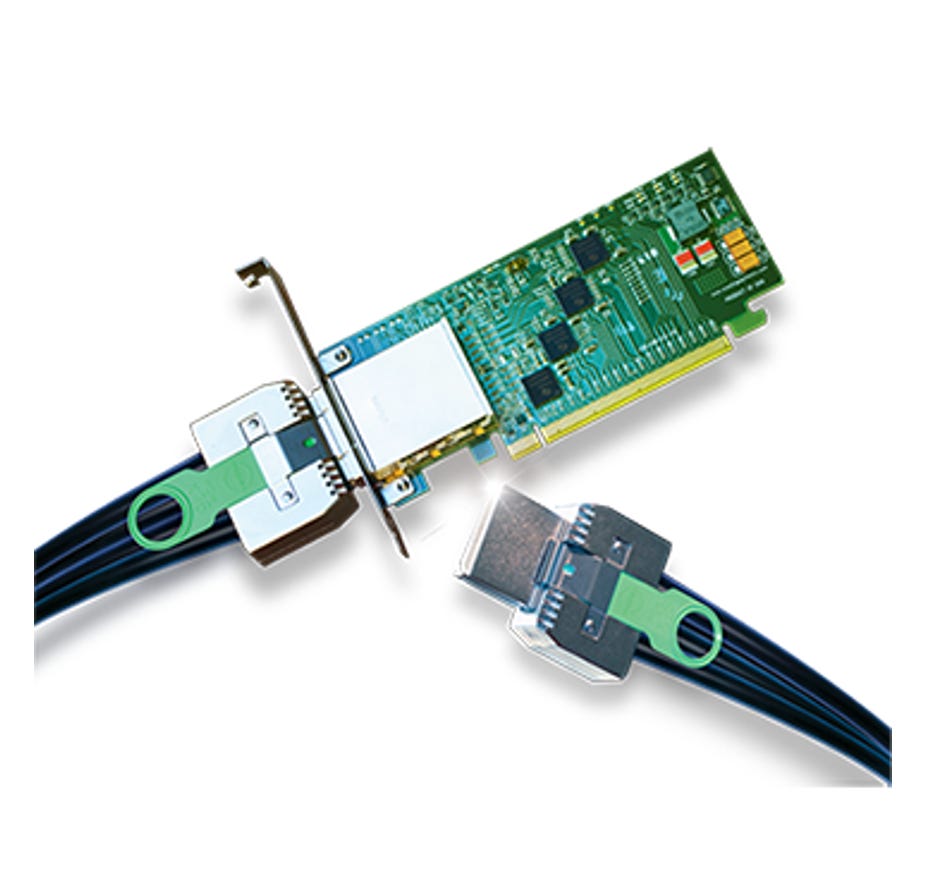

Outside of aircraft, OSS makes specialized PCIe extension systems.

When an autonomous truck or a military vehicle needs to link up 10 different radar and camera modules to a single central CPU, standard computer wiring creates a lag or latency issue.

OSS sells physical interconnect systems.

These are flexible, ultra-fast physical bridges that link external sensor boxes straight into their central servers. This enables the blending of radar, lidar, and camera into a single, cohesive 3D environment map in real time with near-zero latency.

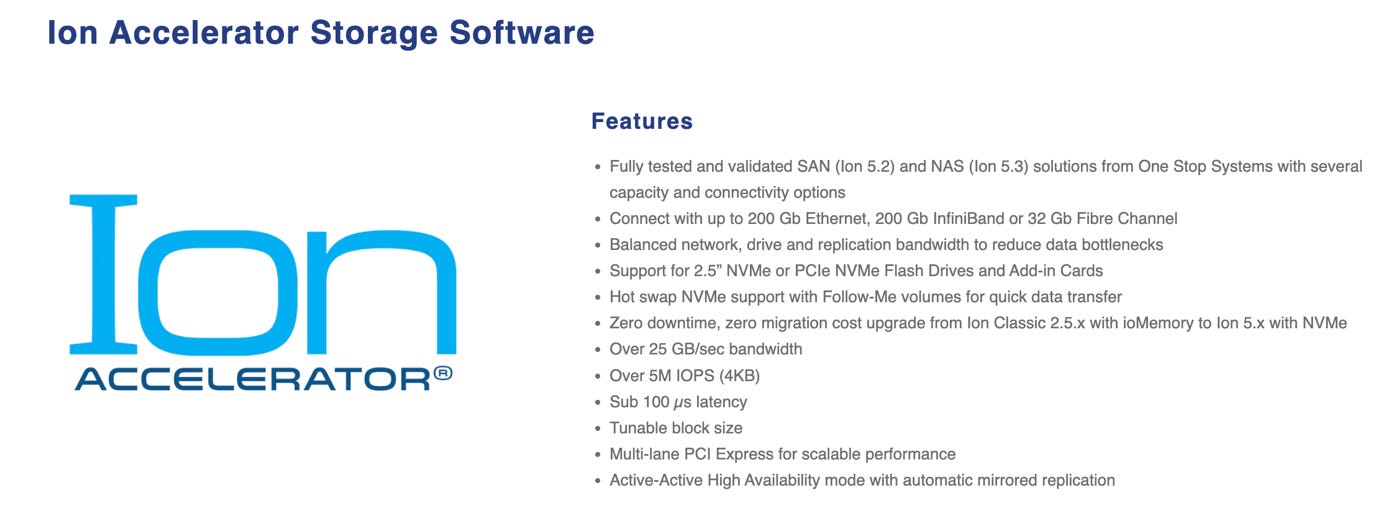

To run their systems, the company developed its own specialized storage software, called Ion Accelerator 5.3.

In demanding AI computing, hardware is only half the battle. If you pack a server with ultra-fast solid-state flash drives but use standard commercial storage software like Windows data management tools, the software creates a massive processing overhead.

The code acts as a traffic cop that slows down the data, resulting in latency bottlenecks.

Ion Accelerator 5.3 is custom-designed to bypass that overhead, extracting near-native, unthrottled performance directly out of flash drives.

2. Business Model

2.1. Assembly and Modification

OSS does not build or design computer chips.

That is an incredibly expensive, difficult, and time-consuming industry dominated by giants.

Instead, the company operates an asset-light assembly and modification business model.

OSS purchases parts, such as GPUs from Nvidia, CPUs from AMD or Intel, and flash memory chips from Micron or Sandisk. The core competency of these companies is to design the best computer chips possible. They don’t care about the assembly and the modifications business, as it is too small for them.

Instead, chip suppliers work with companies such as OSS that build around these computer chips to enable them to function in tough, rugged environments.

OSS adds value by designing custom high-speed circuit boards, like PCIe switch fabrics, that allow these chips to communicate with almost 0 delay.

They also construct the rugged aluminum chassis, build the liquid-cooling systems, and write the essential system management software.

This business model is highly efficient. It keeps capex requirements very low.

For example, during Q1 2026, the company spent only $15K on capex, less than 1% of revenues.

OSS can simply adopt the latest chips as soon as Nvidia or AMD releases them.

It then modifies and repackages them to work in rugged environments in which its military or commercial clients operate.

2.2. Military Contracts

Defense contracts are a key focus for OSS.

The company operates as a subcontractor to large multi-billion-dollar companies, which often outsource some processes to smaller partners.

The sales cycle for military programs is slow, often taking 2 to 3 years of testing, engineering, and meeting strict military standards.

However, once a military customer selects OSS, the company becomes a platform incumbent.

Military organizations do not want to change suppliers because doing so would require starting the expensive testing and certification process all over again. This makes military contracts highly sticky, providing highly predictable sales that span over multiple years.

Key military and defense programs include:

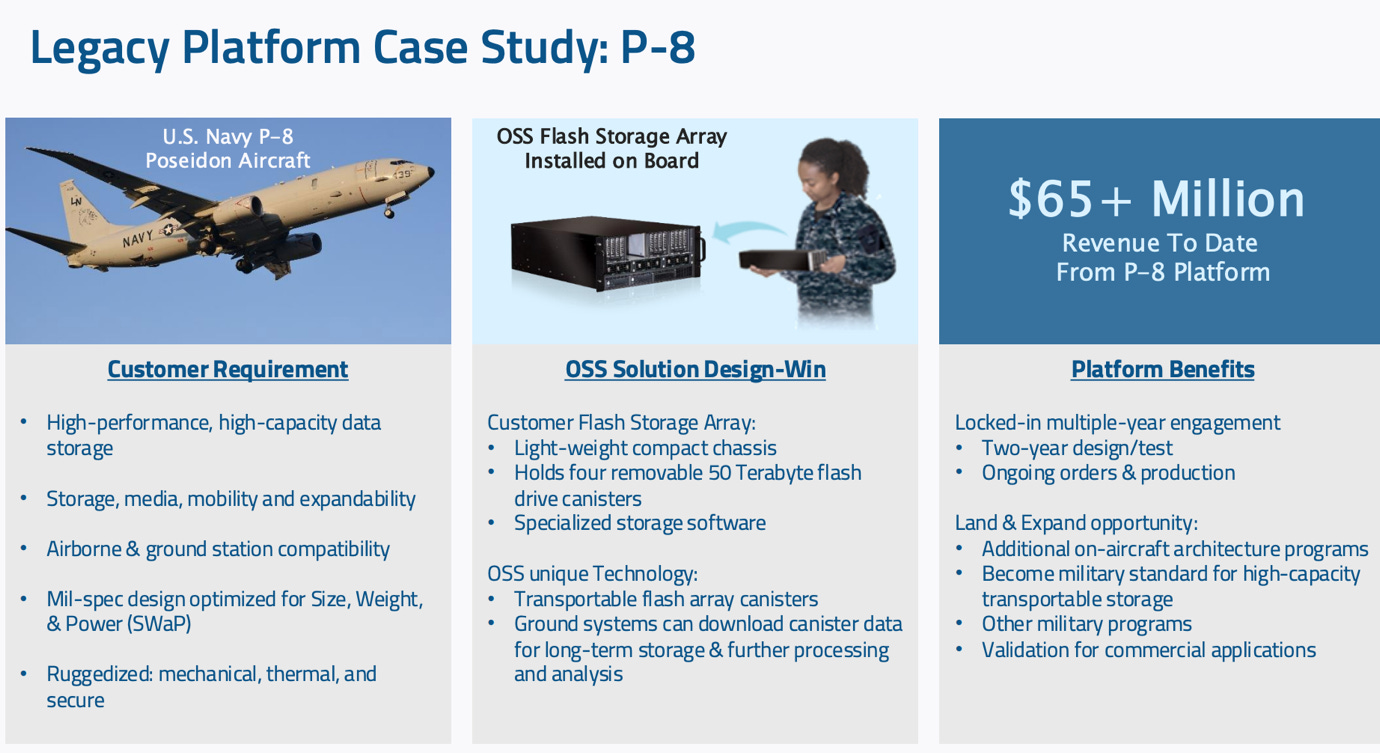

P-8 Poseidon aircraft

US Army rotary-wing platforms

Radar simulation upgrades

The P-8 Navy patrol plane has been a key driver of sales for OSS.

This plane famously participated in the US capture of the Venezuelan dictator Nicolas Maduro.

OSS supplies rugged storage products that have over $65M in contracted sales, with over $23M awarded since early 2025. This includes $10.5M in new orders that will contribute to sales in 2026 and 2027.

For US Army rotary-wing platforms, OSS secured an initial $500,000 contract to supply 3U SDS units for high-speed airborne data recording on helicopters. If successfully integrated, it could lead to more orders.

Next, the company secured a $3M contract to upgrade radar simulation systems for the US Department of War.

The main business risk in military contracts is budget lumpiness. Sales can swing dramatically from quarter to quarter, depending on the timing of budget approvals and product delivery

2.3. Commercial Contracts

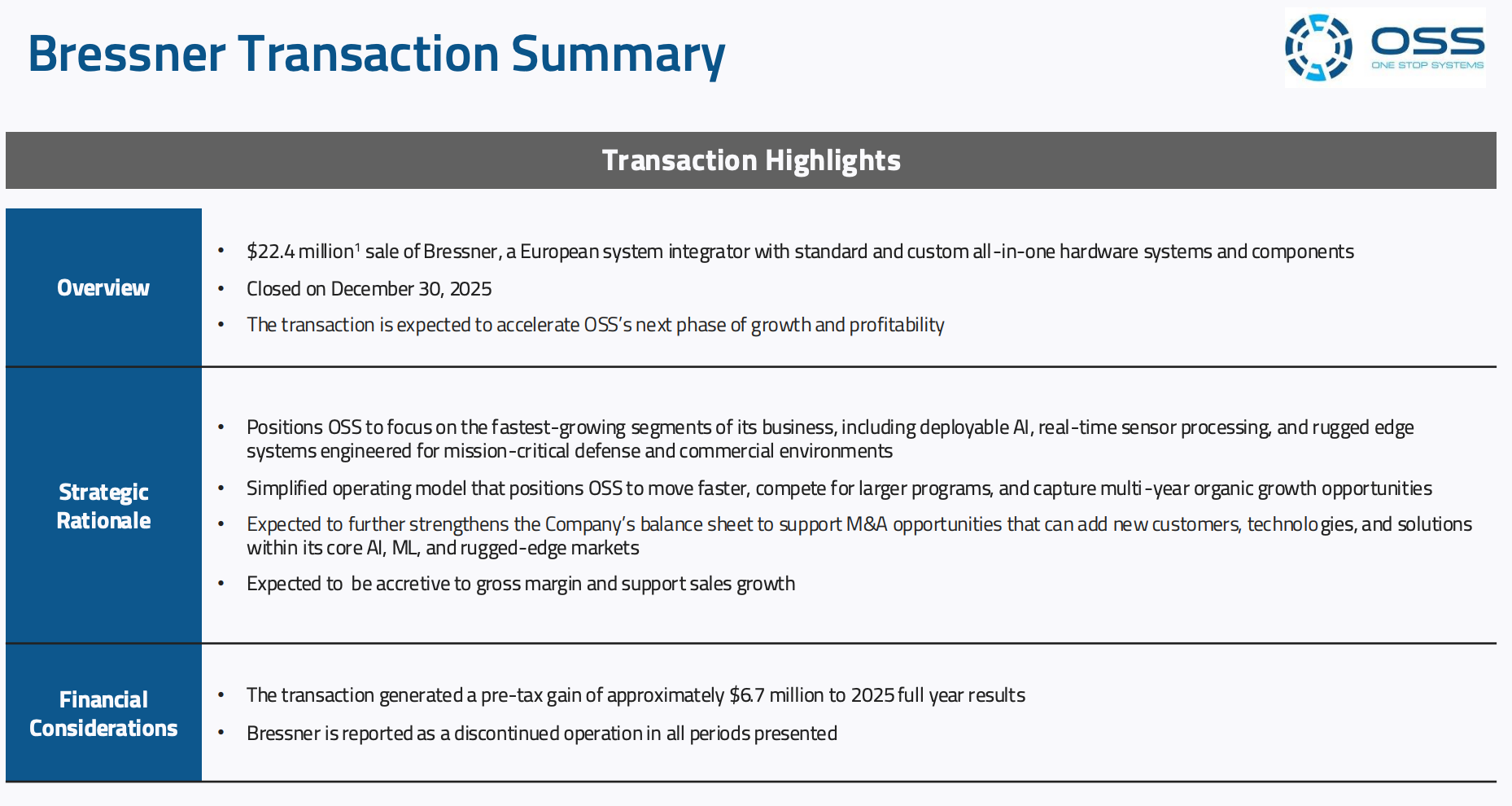

Last year, OSS completed the sale of its European assembly business, Bressner, for over $20M. OSS had originally acquired Bressner in 2018 for approximately $5.6M, so they sold it for a decent profit.

While Bressner grew sales, it operated with thin gross margins.

Divesting this division allowed the company to focus entirely on its higher-margin, custom rugged AI business.

Following the sale of Bressner, the commercial division focuses on high-value partnerships across several industries:

Medical imaging

Autonomous trucking

Commercial aerospace

Autonomous robotics

Alternative energy data centers

OSS has a signed 5-year partnership with a medical imaging company that has a potential value of over $25M. The company supplies custom liquid-cooled servers to handle real-time calculations for advanced medical scans that I mentioned earlier in the report.

Furthermore, OSS secured a contract with an autonomous mining and construction robotics company. This program is expected to generate $2M in orders in 2026, with a 5-year opportunity of $10M to $15M.

$25M and $15M potential orders over 5 years seems small, and it is. However, these orders should be in part viewed as R&D and technology validation. If successful, more and larger orders for these use cases will follow.

3. AI Growth Opportunity

The AI market is expected to continue growing rapidly, but much of the current investment is focused on data centers.

If edge AI adoption accelerates over the next decade, OSS could benefit from the growing demand for rugged AI compute.

Moreover, the US and its allies have only recently begun a multi-decade procurement cycle to prepare their militaries for the AI revolution.

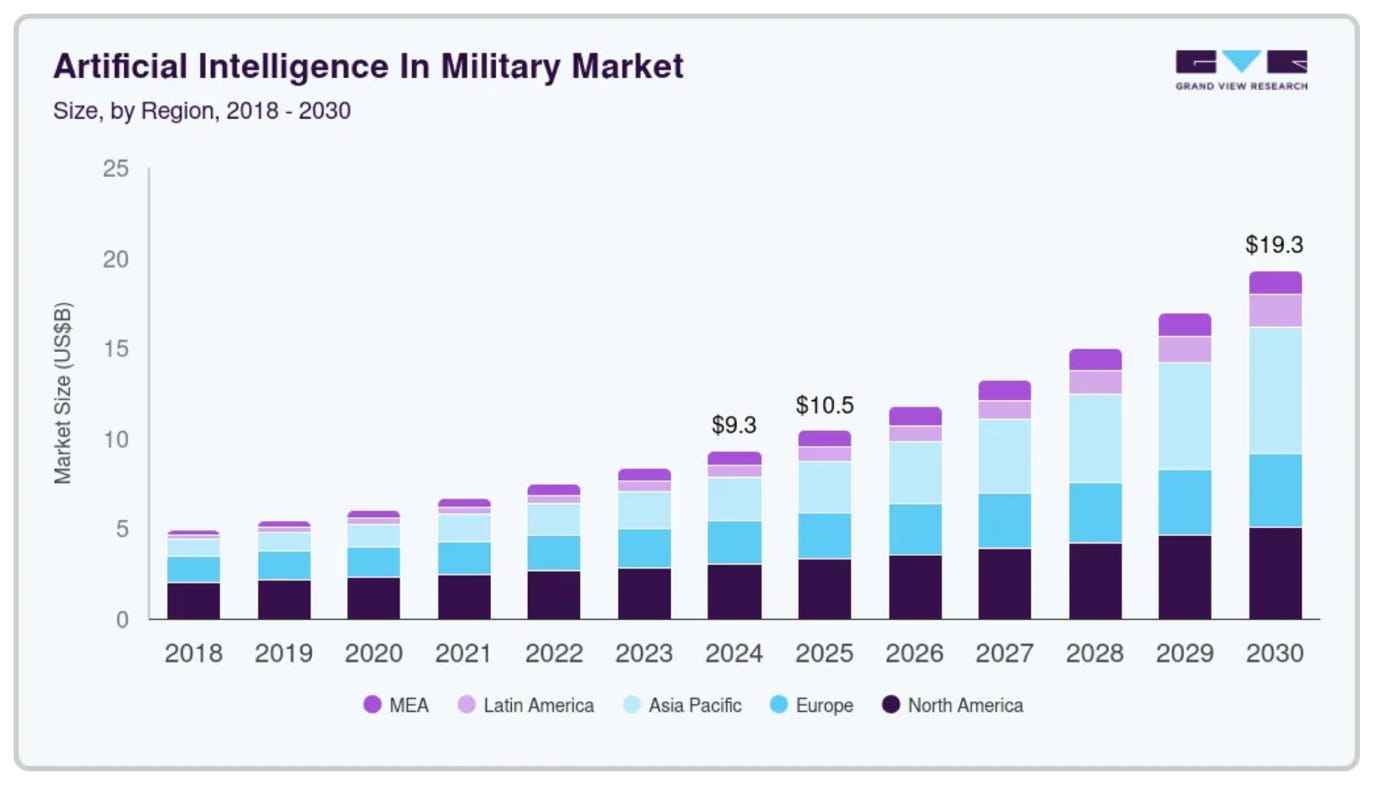

For instance, the research firm Grand View Research forecasts that the Military AI market will grow with a strong 13% CAGR to reach $19.3B in 2030.

The defense segment stands as a key driver of long-term revenue growth, representing a potentially highly profitable and stable market.

While the majority of this market will be served by the AI software giants such as OpenAI, Anthropic, Microsoft, and Palantir, there will be a lot of demand that will spill over to OSS.

To run the software that these companies develop, a lot of OSS systems products could be purchased by the US and allied militaries.

Every few years, as AI advances and sensor requirements increase, military clients are forced to buy denser, faster flash storage from OSS to keep up. Furthermore, the more powerful AI chips get, the more it makes sense to have them embedded directly on military vehicles.

This gives the company a more predictable revenue stream embedded directly into major government equipment fleets.

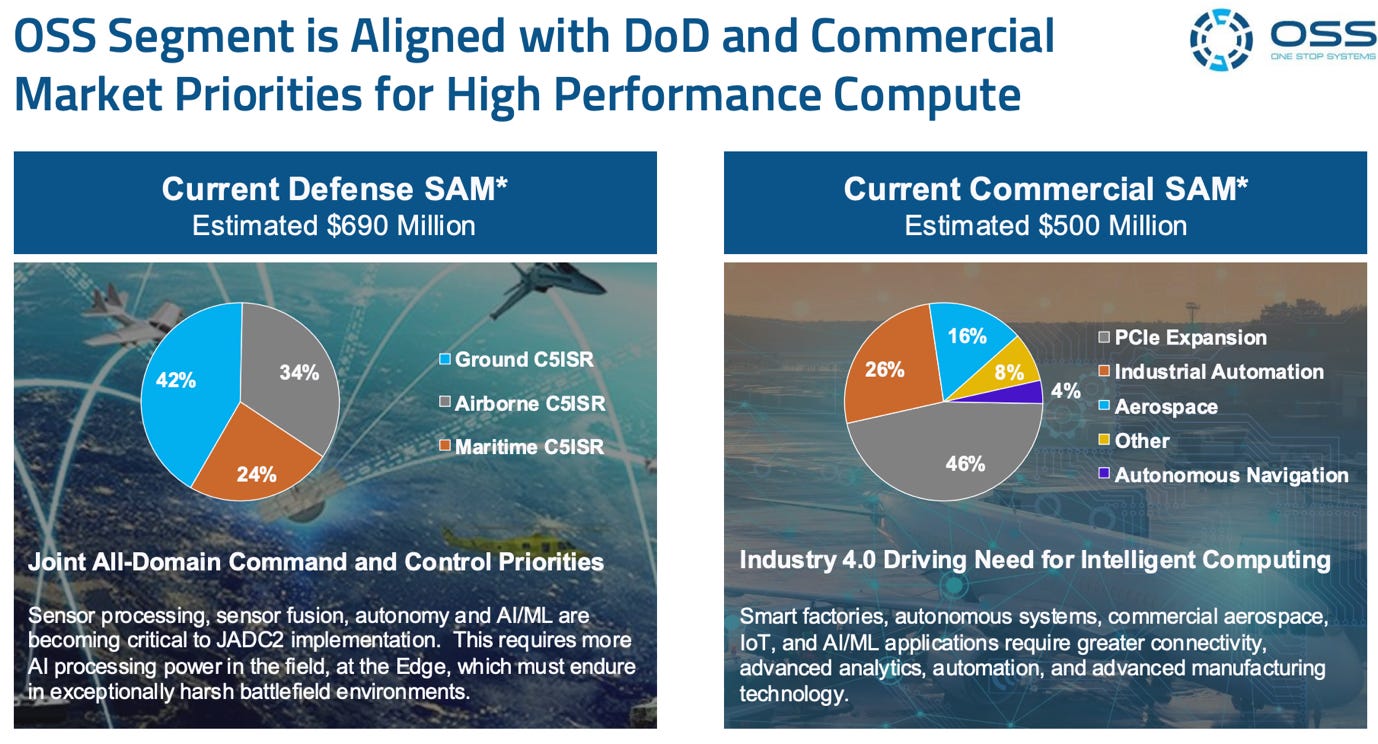

OSS estimates that with its current product offering, it has a serviceable addressable market of $690M a year in Defense industries and $500M in Commercial.

Within defense, the largest opportunities are in ground, airborne, and maritime applications.

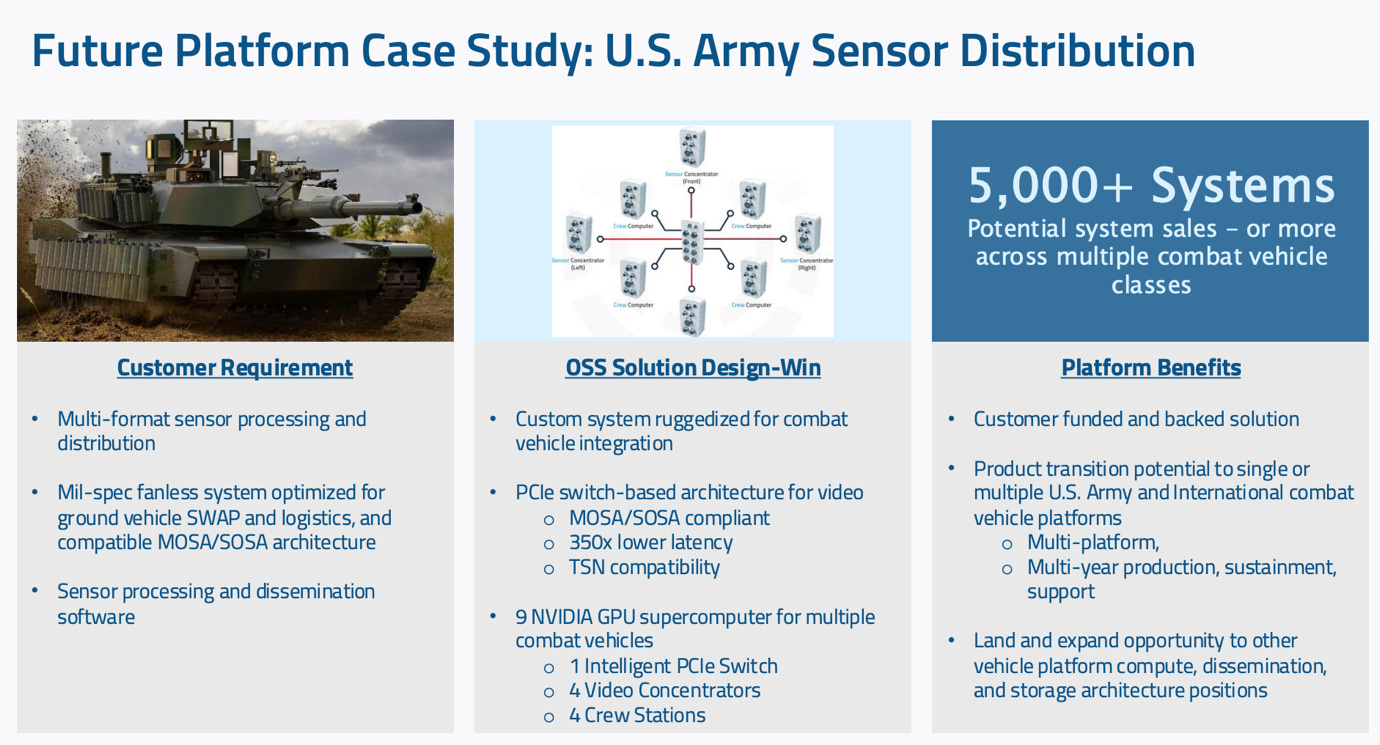

For instance, the U.S. Army alone represents a significant opportunity.

OSS recently secured a design win for a ruggedized sensor processing and distribution system built around its PCIe switch architecture and Nvidia GPU technology for combat vehicles.

Management estimates this platform could be deployed across 5,000+ combat vehicles over time, with the potential to expand into multiple US. Army and international vehicle programs.

Beyond the initial deployment, the program also creates opportunities for follow-on revenue through production, sustainment, and additional upgrades.

On the commercial side, industrial automation, PCIe expansion, aerospace, and autonomous navigation are expected to be the primary growth drivers as the shift to Industry 4.0 intelligent solutions.

Management believes this represents only its current opportunity, with further product development potentially expanding its addressable market over time.

Furthermore, to increase its serviceable addressable market and capture a larger share of its TAM, the company is open to M&A.

Management is targeting acquisitions in adjacent AI, sensor processing, fusion, and rugged edge AI server businesses. The goal is to find targets that can add customers, technologies, or markets.

Rather than pursuing transformational deals, OSS is focused on disciplined, earnings-accretive bolt-on acquisitions that enhance its capabilities.

As a publicly listed company with improving finances (will expand in the next chapter), OSS is in a great position to acquire military start-ups at favourable multiples. Historically, this industry has been capital constrained, due to ethical and ROI considerations of usual VC investors.

This strategy should strengthen its position in the rapidly growing edge/rugged AI market and accelerate both organic and inorganic growth.

A key focus on M&A could be international expansion, with the company estimating that its current product portfolio has a $1B international market.

An acquisition of a European company could both increase the product portfolio and be used as a launchpad for existing products into Europe.

4. Financials

OSS reported a strong financial performance in Q1 2026, showing that its strategy of focusing on core AI edge platforms is succeeding.

In Q1 2026, revenue from continuing operations grew by 55% Y/Y to $8.1M, compared to $5.2M in Q1 2025.

This excludes the financials of the sold Bressner division.

Product sales rose by 48% to $7.1M, up from $4.8M, while customer-funded development rose by more than 100% to $1M, up from $0.4M.

Customer-funded development refers to revenue OSS earns for design and development work for customized products. This allows the company to recover R&D costs upfront while creating the potential for larger follow-on production orders and long-term support revenue. Large military contractors know that they need an AI server, but instead of dealing with all the R&D, they pay OSS to do it for them. This is cheaper and faster for the end customer.

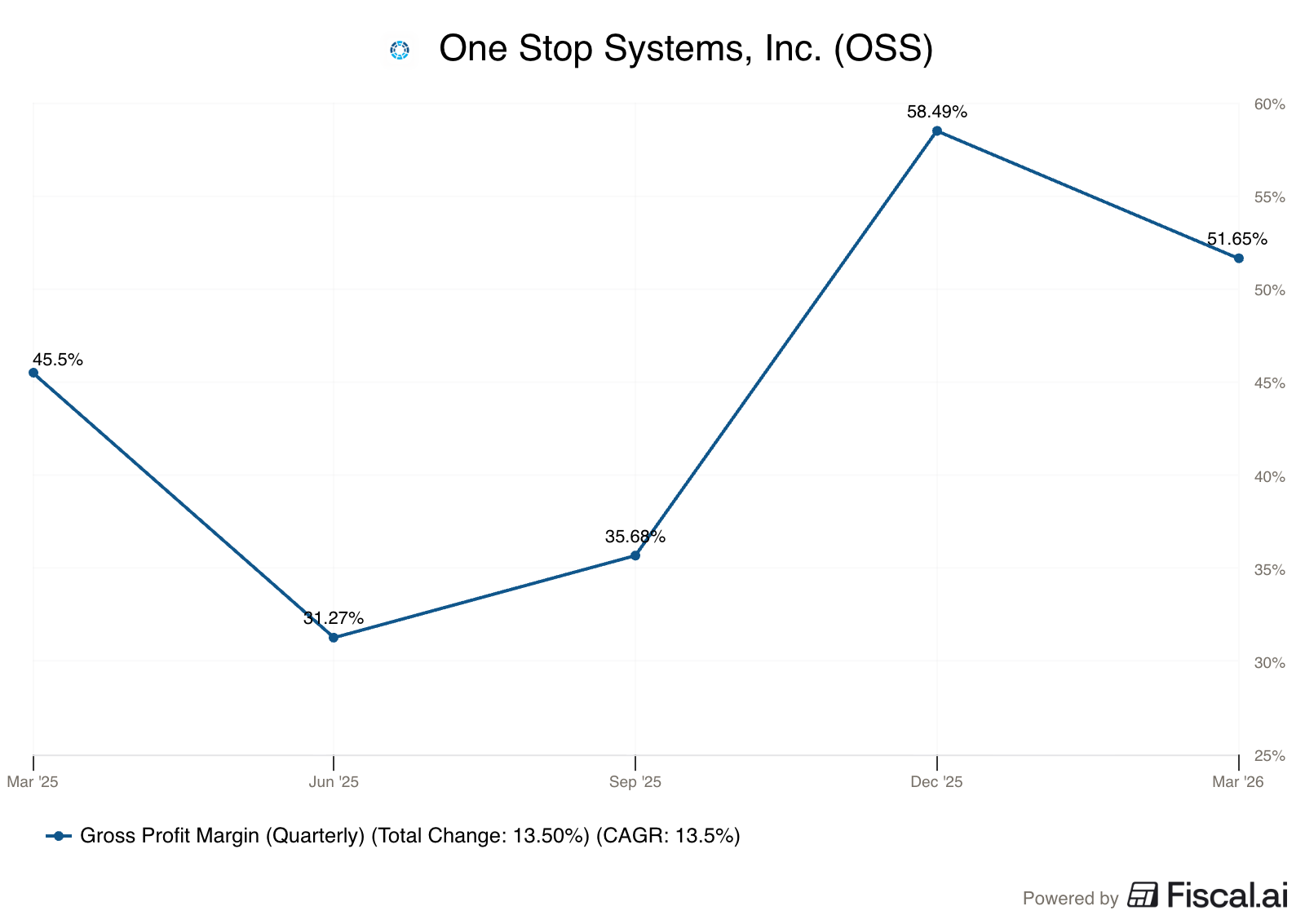

This growth enabled the gross margin from continuing operations to reach a record 51.6% in Q1 2026, up from 45.5% in Q1 2025.

This expansion was driven by a highly profitable mix of product sales and manufacturing efficiencies. Operating expenses grew very modestly by 2.5% to $4.8M, reflecting improving cost controls.

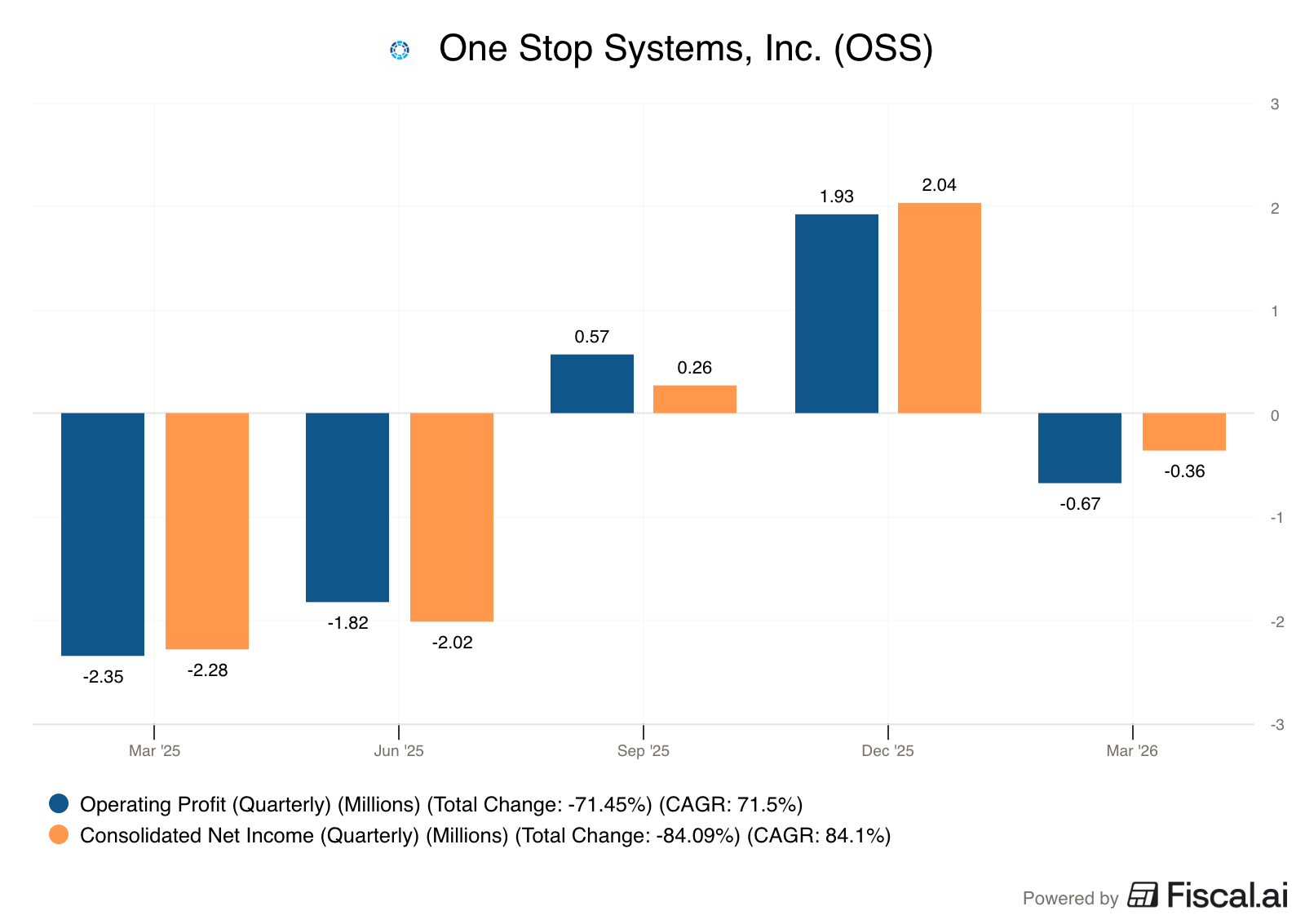

Because of these improving margins and flat expenses, the operating loss narrowed to $671K.

The net loss from continuing operations narrowed to $360K, which is only -$0.02 per share, compared to a net loss of $2.28M in Q1 2025.

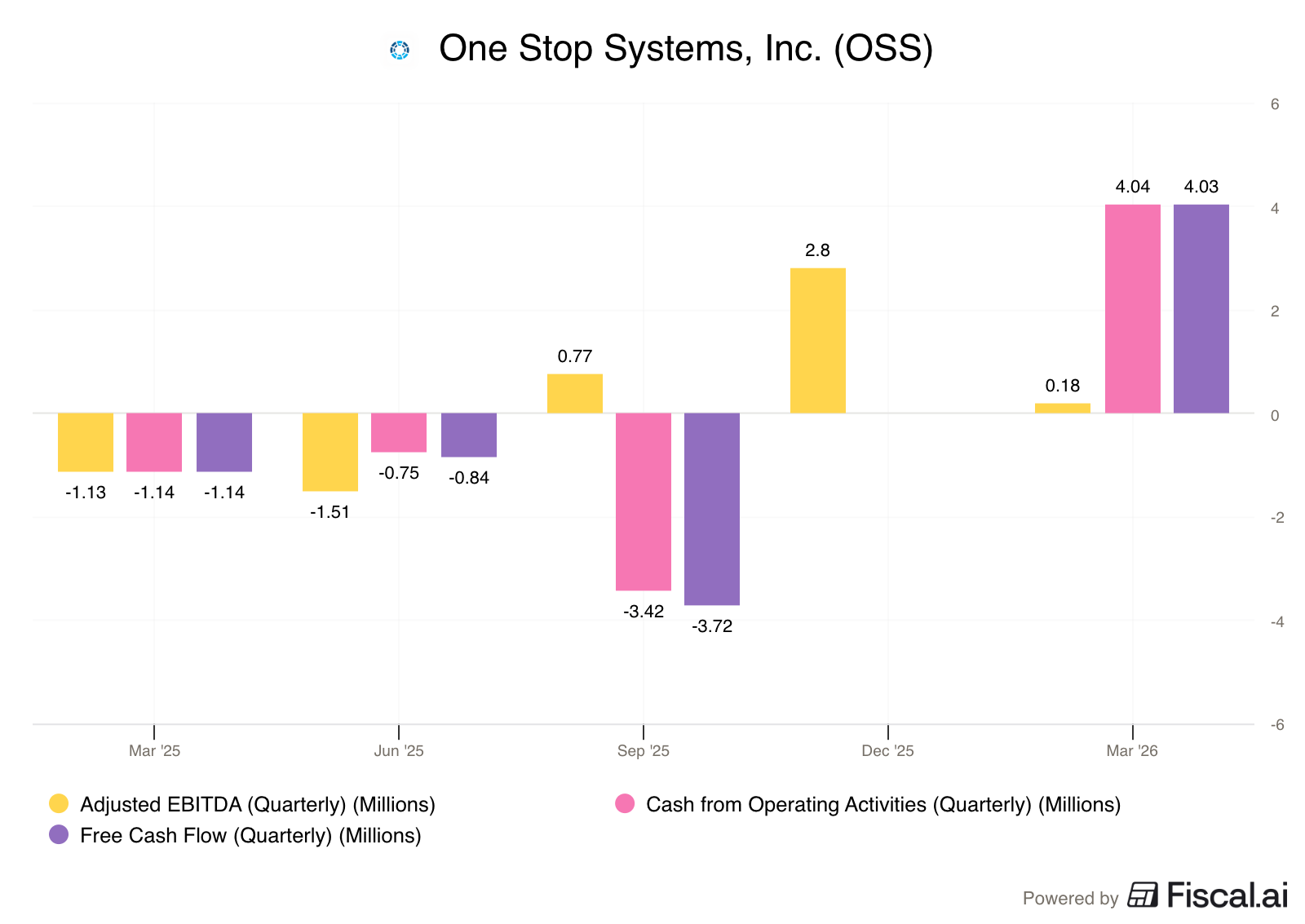

Furthermore, ADJ EBITDA turned positive at $180K compared to a loss of $1.1M in the same quarter last year.

Next, OSS achieved a record positive OCF of $4M, a huge swing from the negative OCF of $1.1M in Q1 2025.

Since capex was extremely low at $15,000, FCF for the quarter was $4M.

Bookings reached nearly $15M, creating a strong book-to-bill ratio of 1.8x, which provides excellent visibility for future sales.

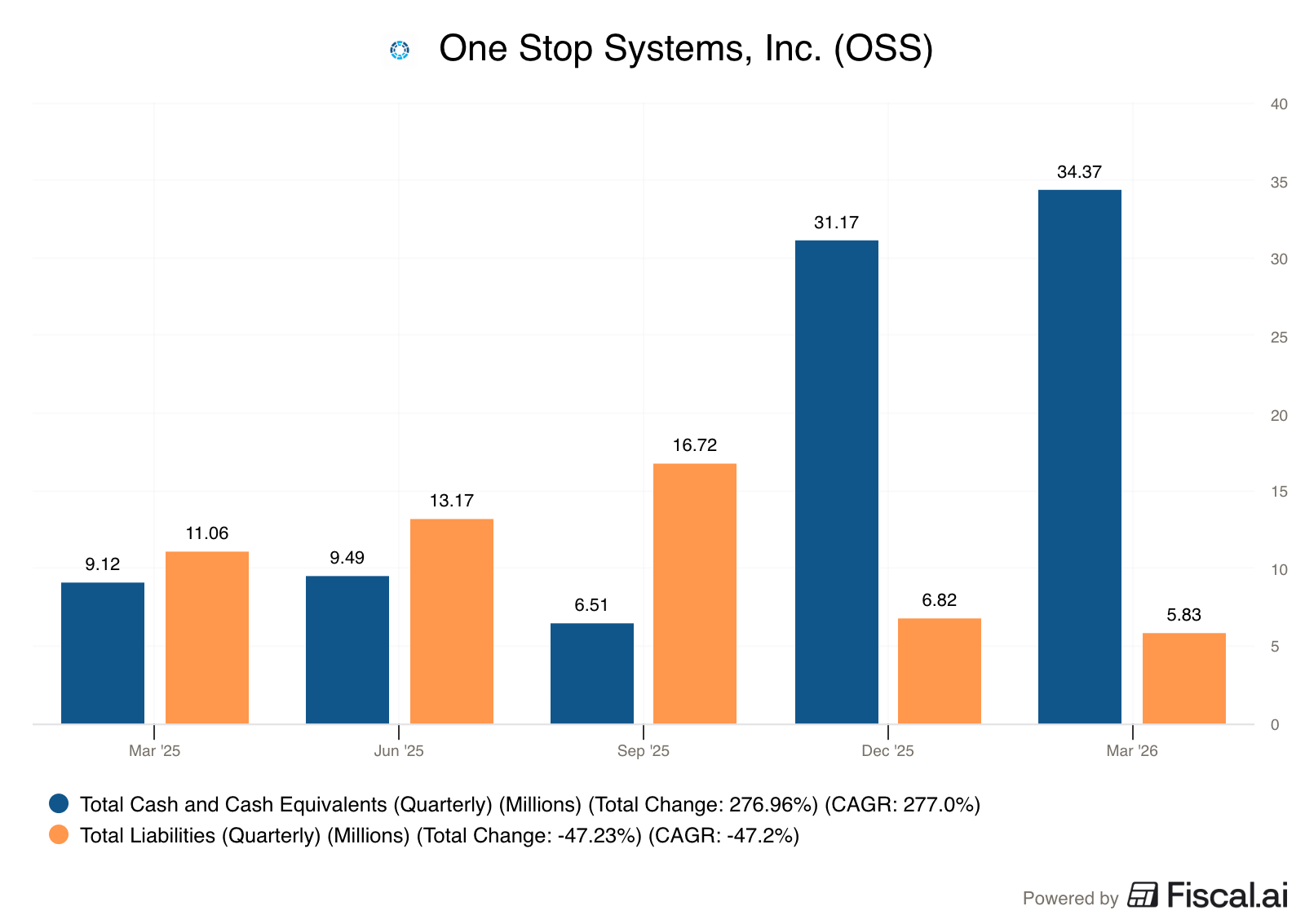

Most importantly, for a company of this size and a clear goal to do M&A, the balance sheet is clean and holds no long-term debt.

As of Q1 2026, the company held $34.4M in cash and had total liabilities of around $5.8M. This gives the company ample wiggle room to raise debt to fund expansion or product development.

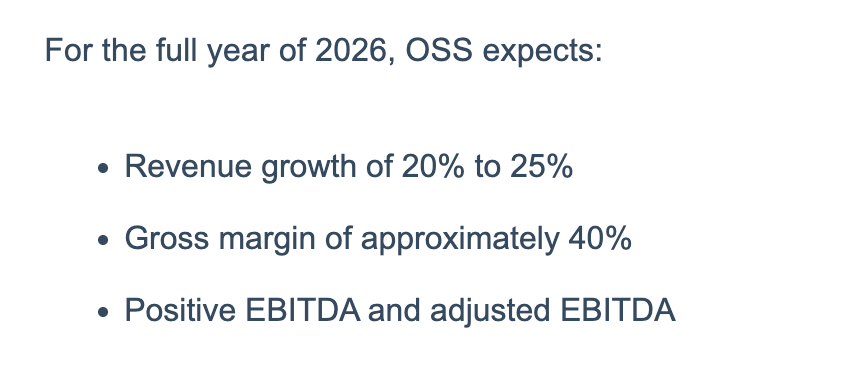

For the full year of 2026, the firm expects sales growth of 20% to 25%. Gross margins are expected to normalize to approximately 40% as product mix changes, and ADJ EBITDA is projected to remain positive.

5. Valuation Model

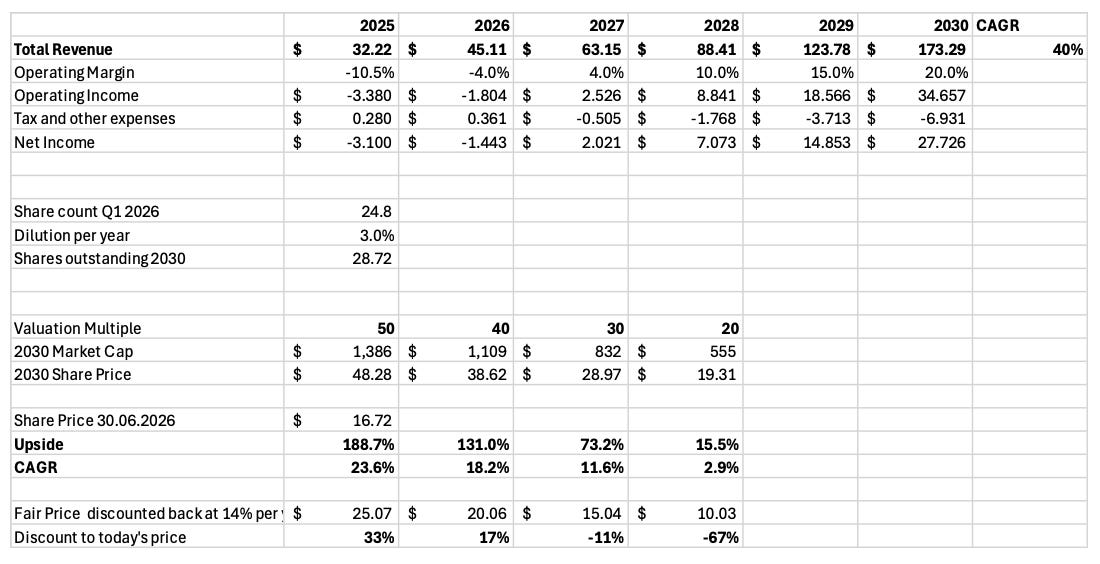

After rising 145% in 2026, OSS now trades for a market cap of $445M. With LTM revenues from continuing operations (excluding the sold business) of $35M, the company trades for TTM P/S of 13x.

This is a bit of a demanding multiple for an unprofitable company that guided for 20-25% growth in 2026.

Investors buying at today’s multiple are betting on the growth to meaningfully accelerate in the next few years.

So, let’s model what kind of growth and margins the company would have to deliver for investors to make meaningful gains.

Assumptions:

Revenue 40% CAGR

Operating margin of 20%

Tax and other at 20% of operating income

Dilution of 3% per year

With such assumptions, we get net income of $27.7M.

Modelling an exit multiple of 30-40, we get an upside of 73-130%.

Considering the company is guiding for 20-25% growth in 2026, a 40% 2025-2030 revenue CAGR is an aggressive assumption. So is the 20% operating margin, considering the company currently has a negative operating margin.

So, achieving such assumptions, while possible, is certainly not a very likely outcome.

Furthermore, even if these results are achieved, an investor could only be rewarded with 73-130% upside.

Thus, at this valuation, I don’t find OSS to be an attractive investment opportunity.

However, that can change rapidly if there is a sell-off in the stock or the company shows improvements that would increase growth expectations.

“in that pipeline, we’re seeing probably an increased number of potential transitional or transformational opportunities ….. it is creating more opportunities for us to find potential transformational organic growth out of out of things that we’re doing….

continuing to strengthen our positive feeling about the ability to grow at that 20% to 30% range.

As I mentioned, there are those transformational opportunities and some long programs of record that were we to see those come to fruition, would represent substantially greater growth than what we’re seeing.” Mike Knowles, OSS CEO, Q1 2026 Earnings Call

Essentially, the CEO said that they expect a 20-30% long-term growth rate. However, there is a probability of this growth rate being substantially higher if they get more Army, space, or robotics contracts.

However, it seems that the company is priced as if these successes are guaranteed.

6. Conclusion

In conclusion, OSS is a high-growth, pure-play edge/rugged AI hardware player.

The company works with large military defense companies to build AI servers capable of working in tough environments like air, sea, and space.

It is clear that the next stage of AI development is moving out of the data center.

OSS is well positioned to serve that large and growing $17B TAM for rugged/edge AI. With its existing product and regional portfolio, the company has a serviceable addressable market of over $1B across military and commercial applications. By successfully expanding outside the US internationally, the company could further increase that by another $1B.

Moreover, with consistent product development and smart M&A, OSS could increase its addressable market further.

However, the stock price of OSS has risen dramatically by 146% in 2026, reaching a market cap of $445M. While that is great for existing investors, it makes entering the stock problematic.

As the valuation model showed, investors are already paying for strong profitability and 40% revenue CAGR, while the company has indicated it expects its long-term growth rate to be in the 20-30% CAGR range.

As such, I don’t find the current valuation of OSS an attractive entry point.

However, I will continue following the company to see if that changes.

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 15 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

You can follow me on Social Media below:

X(Twitter): TheRayMyers

YouTube: TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Equity Research Report List

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.