Share Cannibals: Why Charlie Munger Loved Them.

10 great and 4 failing examples of Share Cannibals.

Charlie Munger famously told investors to “look at the cannibals”.

A share cannibal is a company that repurchases huge amounts of its own shares.

When a mature and financially strong company buys back its own stock, it directly reduces the float.

As a result, the remaining shareholders automatically own a larger piece of the business.

This shrinking of shares has a powerful effect on driving EPS growth.

If a company has $100M in net income and 100M shares outstanding, its EPS is $1.

If that company buys back 50% of its shares, leaving only 50M shares outstanding, the EPS jumps to $2.

This is a 2-fold increase in EPS, even though the core business net income did not grow at all.

By investing in growing businesses that regularly repurchase a lot of shares, investors could turbocharge their returns.

Mohnish Pabrai describes this capital return method as Uber Cannibal investing.

He points out that if a business grows its earnings by 15% each year and buys back 84% of its shares over 20 years, the investment turns into a 100-bagger with 0 changes to its price-to-earnings multiple.

If the earnings grow by 10% Y/Y, the company buys back 80% of its shares, and the price-to-earnings multiple expands by 50%, it becomes a 50-bagger in 20 years.

This shows how stock repurchases could compound wealth for patient investors, even in companies that are not seen as “exciting growth stocks”.

For some investors, 10-15% might not seem strong in this AI era, but if combined with consistent buybacks for over a decade, it could lead to quite healthy results.

So, in this report, I decided to take a break from the AI discussion and focus on these share cannibals that Charlie Munger loved so much.

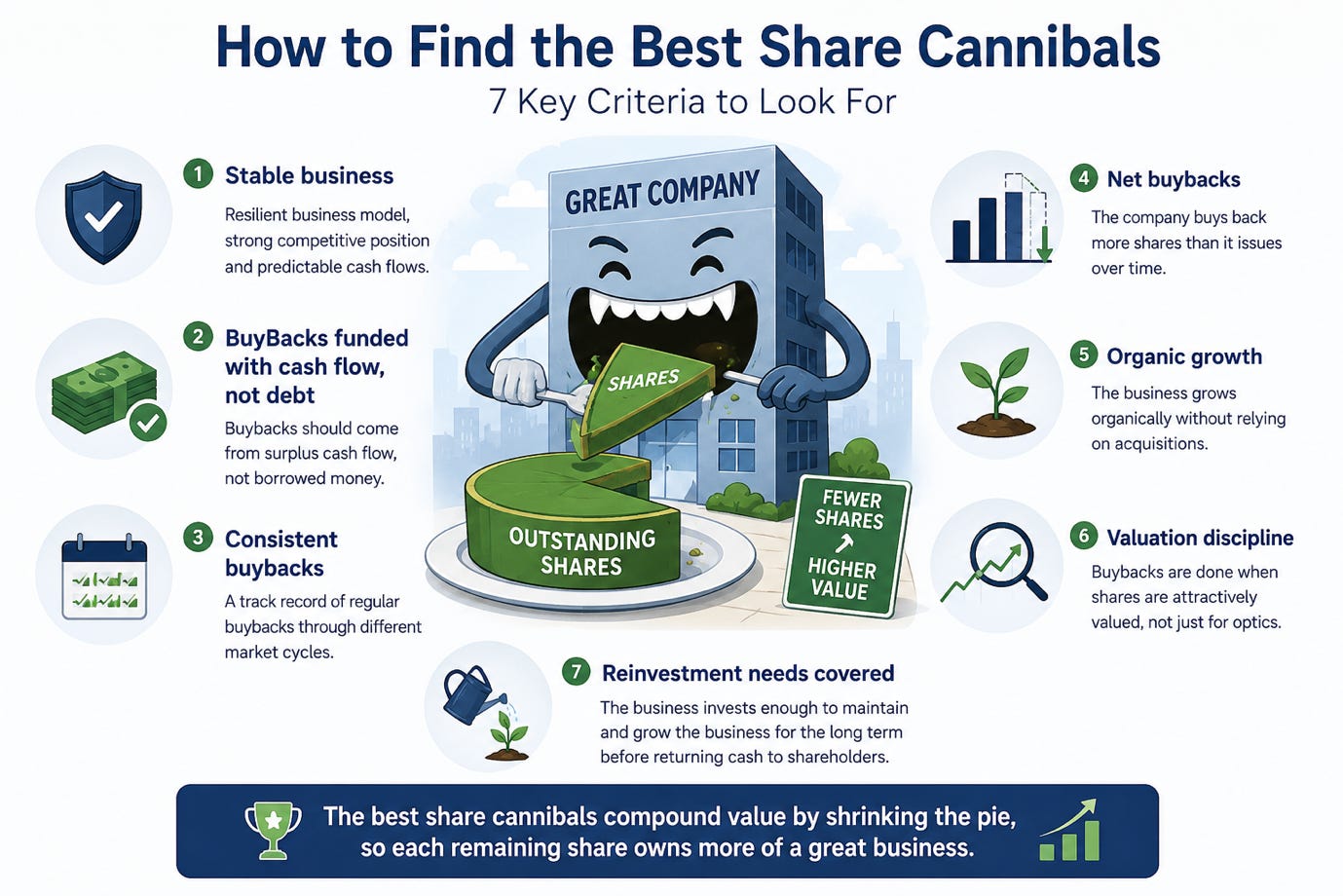

1. Criteria for Investing in a Share Cannibal

Investors often hear quotes from famous investors without really understanding the context in which it was said and apply them the wrong way.

When Mr. Munger said to focus on the cannibals, he didn’t mean to simply look at the buyback yield or the announced buyback plan.

Not all stock buybacks are good. Many companies destroy cash by buying back stock under unfavorable conditions.

Management teams are constantly evaluated based on the performance of their stock. So, in the hope of increasing their share price, some CEO’s announce aggressive buyback plans. While buybacks are great, investors have been conditioned to love them, even when done out of weakness, and that has led to many CEOs focusing too much on buybacks and not enough on their business.

To find the best share cannibals, investors must look for some key criteria:

Stable business

BuyBacks funded with cash flow, not debt

Consistent buybacks

Net buybacks

Organic growth

Valuation discipline

Reinvestment needs are covered

Let me explain.

A great share cannibal must have a highly stable, mature business.

It should not be in decline. If a company is losing sales or customers, buying back stock is useless because the core business value is eroding. Investors must look for companies with a high level of expected stability over the next 10 to 20 years.

Furthermore, ideally, stock buybacks must be paid for with cash flow, not debt.

They should never be funded by taking on high levels of debt. Some bad management teams borrow huge amounts of money to buy back stock just to artificially boost the share price in the short term. This is highly dangerous and can lead to massive trouble in the long term. Using debt to fund share repurchases is beneficial to long-term investors only if the company has a stable balance sheet and it can borrow at a fair rate to purchase undervalued stock.

A clear bad example of this is Hims and Hers. Last year, they raised $1B in a convertible note offering, diluting shareholders. It then committed to spending $250M of that on share repurchases. They spent $80M of this allocation on buybacks at a high share price in Q4 2025, and when it fell over 50%, they didn’t do any buybacks. Now the company is unprofitable and raising $250M in a convertible note offering. Why dilute shareholders by raising funds that were meant for investments, then not announcing buybacks, then raising money again? Such a mess.

So clearly, for buybacks to have a real effect, the company must be a reliable and consistent repurchaser of its own stock.

Sporadic buybacks often happen only when management has too much cash at the peak of a market cycle, like in the Hims and Hers example. This means that likely they pay very high multiples. Consistent buybacks average out the purchase price over time, showing a disciplined plan to return cash to shareholders.

Crucially, investors must not take the buyback yield and announced repurchase plans at face value.

Many companies issue a massive number of shares to employees every year. If a company repurchases shares just to offset employee dilution, those buybacks do not directly benefit shareholders. A real share cannibal must reduce its net share count over time, even after counting new shares issued for compensation or acquisitions.

Stock buybacks should act like gasoline on a fire, it should not be the only thing growing the EPS.

While a declining share count boosts EPS, the core business must also grow its net income. When organic growth is combined with a shrinking share count, the EPS compounds very quickly. Relying solely on buybacks to grow EPS without any real business growth is a bad long-term strategy.

Also, valuation discipline is a key rule for buyback success.

Repurchasing stock only makes sense if the shares are bought below their intrinsic value. If a company pays a ridiculous price for its own shares (like Hiims and Hers in Q4), it destroys cash that could be better spent elsewhere. Management must act like smart capital allocators and only buy when the stock is cheap, not only when they have cash.

Most importantly, a company must never underinvest in its core operations to pay for buybacks.

All reinvestment needs, like capex and R&D, must be fully covered before considering any buybacks. If a company underspends on R&D to buy back shares, it will lose its long-term competitiveness. Excellent cannibals can easily fund both technological innovation and massive buybacks.

2. 10 Examples

The following 10 companies show how disciplined stock buybacks can build massive shareholder value over long periods.

2.1. Apple

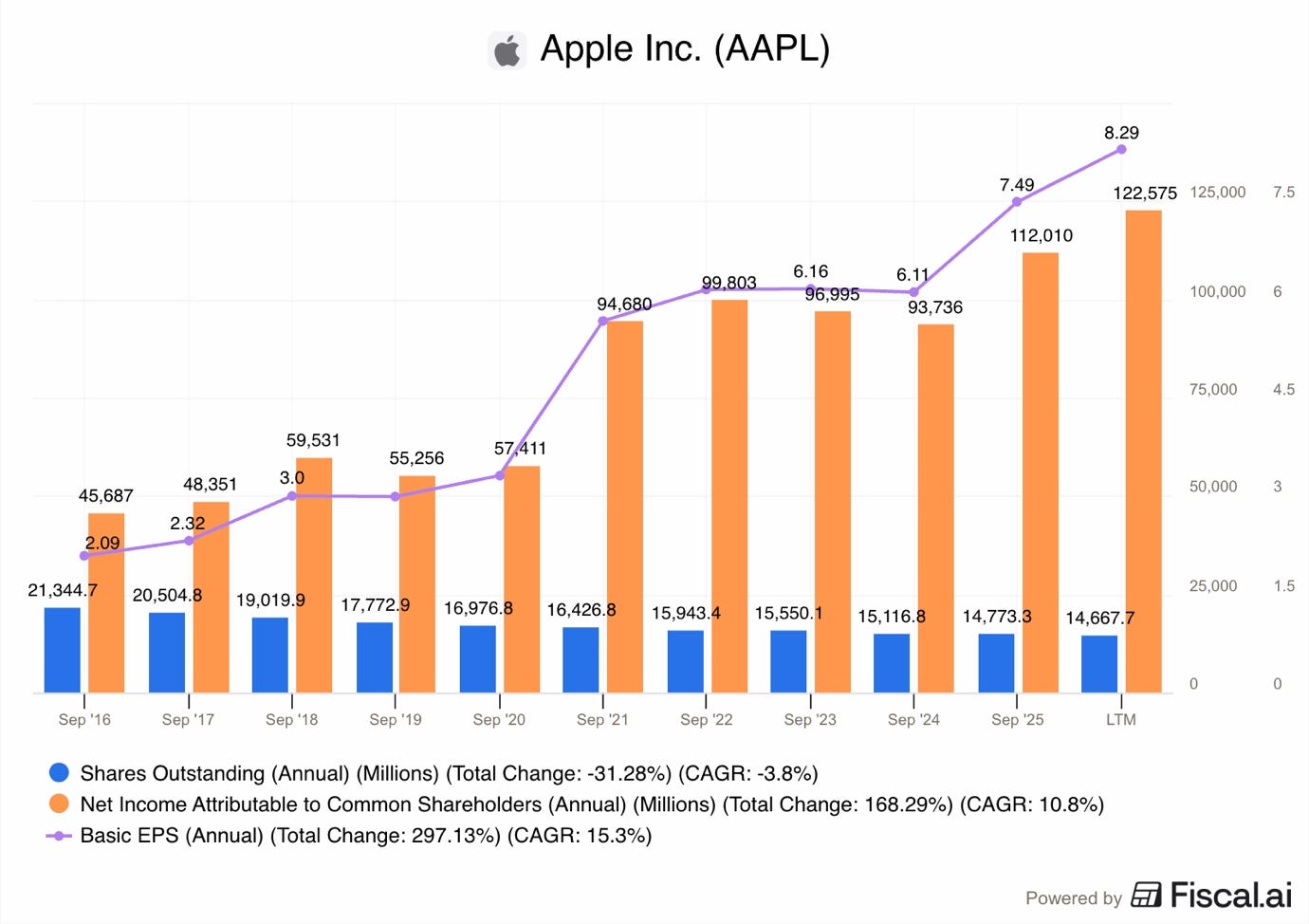

Apple is the most famous share cannibal.

The company started its buyback program in 2012. At its peak in 2012, its outstanding share count stood at 26.47B. By 2025, Apple reduced its shares outstanding to 15.005B, a massive 43.3% decline.

Apple spends huge amounts of excess cash on repurchases. For example, in 2024, its net share repurchases totaled $94.9B, up 22.4% from 2023.

Apple did this while investing billions in R&D, releasing new highly successful products, and without hurting its product pipeline.

Let’s look at what results these buybacks have had on Apple’s income statement.

Since 2016, Apple has repurchased 31.3% of outstanding shares, reducing the share count by about 3.8% per year.

During this time, net income grew by 168% with a CAGR of 10.8%.

However, EPS grew by 297% with a CAGR of 15.3%.

This is a clear example of how buybacks work over a long period of time.

Total EPS growth rate was 77% higher than the net income growth, while the CAGR was 42% faster.

Essentially, had Apple not done these buybacks, EPS would have been $5.61, not $8.29 it is today.

Buybacks are much better than dividends because share repurchases are taxed more favorably and force the investor to reinvest more of their gains.

In the US, share repurchases are taxed at 1%, while dividends are taxed much higher, depending on the state and situation, at even 40%.

Furthermore, buybacks essentially force an investor to reinvest. If one receives dividends, they can be reinvested to compound for the long term, but most investors don’t do that.

Buybacks can also be viewed as the company essentially reinvesting your dividends in its own stock for you, so you don’t have to.

This is a tax-efficient way to amplify your returns.

2.2. AutoZone

AutoZone is an incredibly aggressive share cannibal.

It launched its repurchase program in 1998. Over 2 decades, it spent more than $36B to buy back almost 90% of its outstanding shares.

AutoZone’s annual shares outstanding dropped from 27.83M in 2017 to 16.52M in Q1 2026, a reduction of 40.7%.

Net income grew with a CAGR of 7.9% compared to 14.9% EPS CAGR.

2.3. NVR

NVR is a US homebuilder that has repurchased stock since 1994.

Its shares outstanding fell from 3.69M in 2017 to 2.63M in Q1 2026, down by 28.9%.

NVR’s buyback yield peaked in March 2026 at 10.5%.

Its average buyback yield from 2021 to 2025 was 7.1%.

Do you like the chart above?

FiscalAI makes managing investments smarter, faster, and stress-free.

Visualizations

AI-powered insights

Financial data

Earnings transcripts

Portfolio analytics

All in one place. Instead of wasting hours digging through filings and spreadsheets, Fiscal.ai helps you get to the important information in minutes.

Save time, stay organized, and let Fiscal.ai handle the heavy lifting so you can focus on growth.

Join with my link below.

Net income grew with a CAGR of 10.6% compared to 14.3% EPS CAGR.

The stock hasn’t done well in the last 5 years due to stagnation of the US new build housing market, because of rising inflation, and high interest rates.

However, the company continues buying back shares, spending $1.8B in 2025. Once the cycle turns and housing construction rebounds, investors will benefit from these buybacks.

2.4. O’Reilly Automotive

O’Reilly is an automotive part retailer that began its stock buyback program in 2011.

Since then, the company has spent over to $30B on share repurchases.

It has reduced its share count by 34.2% since 2017.

Net income grew with a CAGR of 10.6% compared to 16.8% EPS CAGR.

As you can see, the long-term EPS CAGR is 58% higher.

The longer the buybacks are done, the more they compound.

2.5. Booking

Booking is an online travel agency that has very low capex requirements.

In 2025, its capex was only $322M, while its OCF was a huge $9.4B.

This leaves almost all of its cash available for buybacks and dividends, a perfect combo to be a share cannibal.

It has reduced its share count by 35.6% since 2017. This is especially impressive considering the disruption the COVID-19 pandemic caused to its business in 2020 and 2021.

Booking’s position is so stable that the company paused share repurchases only for a single year in 2021, returning with a $6.6B buyback in 2022.

Net income grew with a CAGR of 12.4% compared to 18.3% EPS CAGR.

As you can see, the long-term EPS CAGR is 48% higher.

Do you like this report?

Become a Paid Premium member to see dozens of exclusive pay-walled equity research reports such as this.

Curious about which stock I own?

Full portfolio with all holdings, cost basis, and unrealised gains is visible to Premium members. I do weekly updates and detailed monthly reviews. Premium members are also notified of all sales and purchases using the pay-walled Substack Chat.

The annual plan is available for 50% cheaper per month than the monthly plan.

2.6. Domino’s Pizza

Domino’s is the world’s largest pizza chain that has steadily bought back its stock.

Its shares outstanding fell from 42.9M in 2017 to 33.5M in Q1 2026, a reduction of 21.9%.

Net income grew with a CAGR of 9.6% compared to 13.7% EPS CAGR.

The long-term EPS CAGR is 43% higher.

2.7. Adobe

While historically, Adobe has not been a share cannibal, the company is positioning itself to become one.

Adobe has aggressively repurchased shares to fight off investor fears about AI disrupting its seat-based corporate subscription business.

Its shares outstanding fell from 491.26M in 2017 to 406M in Q1 2026, a reduction of 17.4%.

This might seem modest compared to other cannibals, but this is set to change. In the last 12 months, Adobe has spent $10.5B on share repurchases and only $2B on SBC, for a net buyback of $8B.

A market cap of $100B implies that Adobe is set to reduce its share count by a net 6-8% per year. If the valuation and buyback cadence remain the same, Adobe will repurchase 20-30% of its outstanding shares in the next 3-4 years.

So far, net income has grown with a CAGR of 19.2% compared to 21.6% EPS CAGR.

The long-term EPS CAGR is just 13% higher, but that will change rapidly in the next 3 years.

If AI doesn’t disrupt the business, Adobe will be a massive compounder.

2.8. Oracle

Oracle has historically been cannibal that has reduced its share count significantly over the last 15 years.

However, that trend stopped in 2022 as the company focused on building its AI cloud business.

Despite that, the share count is still 30.5% smaller today than it was in 2017.

As a result, net income has grown with a CAGR of 6.4% compared to 10.9% EPS CAGR.

So, the long-term EPS CAGR is 70% higher.

2.9. Hilton

Hilton has transformed from an asset-heavy hotel builder and developer into a capital-light franchise model that generates huge excess cash flow.

For instance, in 2025, the company returned $3.3B to its shareholders through buybacks and dividends.

Hilton’s shares outstanding dropped from 317.42M in 2017 to 228.33M in Q1 2026, a reduction of 28%.

As a result, net income has grown with a CAGR of 4.4% compared to 8.6% EPS CAGR.

So, the long-term EPS CAGR is an amazing 95% higher. This demonstrates the power of thoughtful buybacks executed at favorable market prices.

Similar to Booking, Hilton used the COVID rebound to repurchase $1.6B and $2.3B in shares in 2022 and 2023.

2.10. American Express

American Express is a prime example of how share buybacks benefit long-term investors like Warren Buffett.

Berkshire Hathaway has held about 151M shares since 1994, which is roughly 21% ownership in the company.

Berkshire has not bought new shares in years, but its ownership share keeps increasing because American Express constantly buys back its own stock.

Amex shares outstanding fell from 857.1M in 2017 to 682MM in Q1 2026, a reduction of 20.4%.

In Q1 2026 alone, the company returned $2.3B to shareholders, including $1.7B in buybacks.

As a result, net income has grown with a CAGR of 18.6% compared to 22.5% EPS CAGR.

So, the long-term EPS CAGR is an 21% higher.

3. Failing Share Cannibal Examples

As I said earlier, buybacks alone do not guarantee compounding for investors.

Many companies buy back stock to hide structural decline.

These businesses show that stock repurchases are useless if the core model is eroding and management underinvests in new revenue sources.

Let’s look at 4 distinct examples:

PayPal

Charter

Western Union

General Motors

PayPal has spent billions on share repurchases, but this has failed to create long-term value.

Since 2020, the company has spent over $26B on buybacks.

Despite this, its stock has crashed by over 80% from its 2021 peak.

This collapse happened because PayPal’s core business is in decline. Their branded checkout growth has stalled, growing only 2% in Q1 2026 and 1% in Q4 2025. This branded checkout button is PayPal’s highest-margin product.

At the same time, the company is facing intense competition from Apple Pay, Stripe, and Adyen.

PayPal’s active accounts have slowed to 439M, and its ADJ operating margin fell from 20.7% to 18.4%.

Instead of investing in creating high-margin products, PayPal is growing in low-margin products like Venmo and unbranded processing, which cannot replace its lost high-margin revenue.

Buying back shares is useless when the core business model is eroding, and the company underinvests in building new revenue-generating products capable of replacing it.

Charter is another clear example of a failing cannibal.

The company does not pay dividends and focuses entirely on buying back its own stock.

Since 2017, Charter has spent close to $70B on buybacks.

Despite this, its stock has crashed by over 79% in the last 5 years.

This is because Charter is facing a terminal business decline.

Charter lost 120,000 customers in Q1 2026, worse than the 59,000 lost in Q1 2025, showing that its broadband cable subscriber losses are accelerating.

Its total revenue fell 1.0% to $13.6B in Q1 2026. This erosion is caused by fierce competition from fixed wireless providers like T-Mobile and AT&T, as well as new fiber networks.

To fight this competition, Charter is carrying out a massive capex cycle, spending $11.7B in 2025.

This heavy capex drains cash and reduces FCF. At the same time, Charter carries a very heavy debt load with a leverage ratio of over 4x EBITDA.

Spending billions in buybacks while carrying huge debt in a shrinking industry is plain stupid.

If subscriber losses continue, EBITDA will decline, and the leverage ratio will rise. This makes Charter’s buybacks a value trap rather than a wealth creator. It would have been more beneficial for the shareholders if Charter had invested these $70B to create new revenue-generating businesses.

Western Union has a long history of stock buybacks, but that doesn’t change the fact that the company is in structural decline.

Since 2016, the company has spent $3.3B on buybacks.

This has had no beneficial impact on its stock, which is down 66% in the last 5 years.

Its stock sits near multi-year lows, showing that buybacks don’t change business fundamentals.

Western Union’s business is in structural decline as its high-margin, cash-based retail remittance business is shrinking.

In 2025, its North American regional money-transfer revenues fell 11%.

This decline is driven by digital-first competitors like Wise, Remitly, and Revolut. These fintech rivals are growing at 30%+ and stealing market share by offering better service and lower fees. This has lowered Western Union’s average take rate and reduced pricing power.

Western Union is trying to build its own digital platform and stablecoin, but its digital growth is too slow to offset the retail drop.

Its digital platform also operates at much lower profit margins. Western Union’s ADJ operating margin dropped to 13% from 18-19% in Q1 2026. Operating cash flow fell 26% Y/Y in Q1 2026.

Repurchasing stock in a business facing structural decline and profit compression is a waste of capital, they should have invested these $3B in rebuilding its tech stack and releasing new neo-banking fintech products, expanding upmarket from being a simple money transmitter into a more developed fintech platform.

General Motors is a dying automotive dinosaur on its last legs that, instead of innovating, has focused heavily on outsourcing and share buybacks.

In 2025, the company repurchased $6B of stock. In Q1 2026, the board approved another $6B share repurchase authorization.

This aggressive buyback program helped lower its outstanding share count from 1.2B in 2023 to 904M in 2025.

Overall, since 2016, the company has spent close to $34B on share repurchases.

This is madness considering that General Motors is facing massive structural issues.

Its core internal combustion business is eroding under a highly challenging and chaotic EV transition. In late 2025, General Motors took massive impairment charges to shift its Orion assembly plant back from EV to ICE production.

It also discontinued its BrightDrop electric van and wrote off several other EV assets.

Meanwhile, its automotive OCF dropped 21.7% to $18.733B in 2025. Spending billions of dollars on share buybacks while cutting EV platforms and facing declining cash flows is a classic sign of artificial EPS boosting.

Tesla and the Chinese automakers are coming for General Motors.

The company is terribly run with incompetent leadership. If the US automotive market were open to Chinese EVs, GM would be bankrupt already. They are cheaper and better than anything GM can offer.

However, this is only a question of time, as eventually the transition will happen and GM won’t be part of it.

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 13 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.