Sofi Q1 2026: Stellar Execution vs Mad Market!

Crashing stock despite, 43% revenue growth and 100% EPS growth.

Welcome to Global Equity Briefing, my weekly investing newsletter.

I am Ray, a passionate investor and equity analyst. And today I am covering Sofi.

I am only 30 years old, so I have not been investing for that long.

But the reaction to Sofi’s earnings is the biggest disconnect between what the reality is and how the market reacted I have ever seen in my investing career.

43% Revenue Growth

62% ADJ EBITDA Growth

100% EPS Growth

Yet the stock was down 16%!

This is especially insane, considering the stock was already down 30% YTD and traded at a FWD P/E of 28 before the earnings.

Find me another stock that is delivering such rapid top and bottom-line growth at such a valuation, with such a strong TAM and incredible innovation in the last 3 years.

So why would the market react in such a way to these earnings?

There are some culprits we can blame.

1. Tech Platform segment is performing so badly that Sofi decided to rebrand it.

2. Deceleration in the Loan Platform Business.

3. Didn’t increase the guidance.

4. Dilution.

In this Q1 2026 earnings review, I will look at the quarterly performance and analyze all 4 of these reasons to determine whether they are valid or not.

Let’s begin!

1. Overall Performance

Revenue $1.1B +43%

ADJ EBITDA $339.9M +62%

Net Income $166.7M +134%

EPS $0.12 +100%

Tangible Book Value $9.2B +83%

Tangible Book Value per share $7.21 +57%

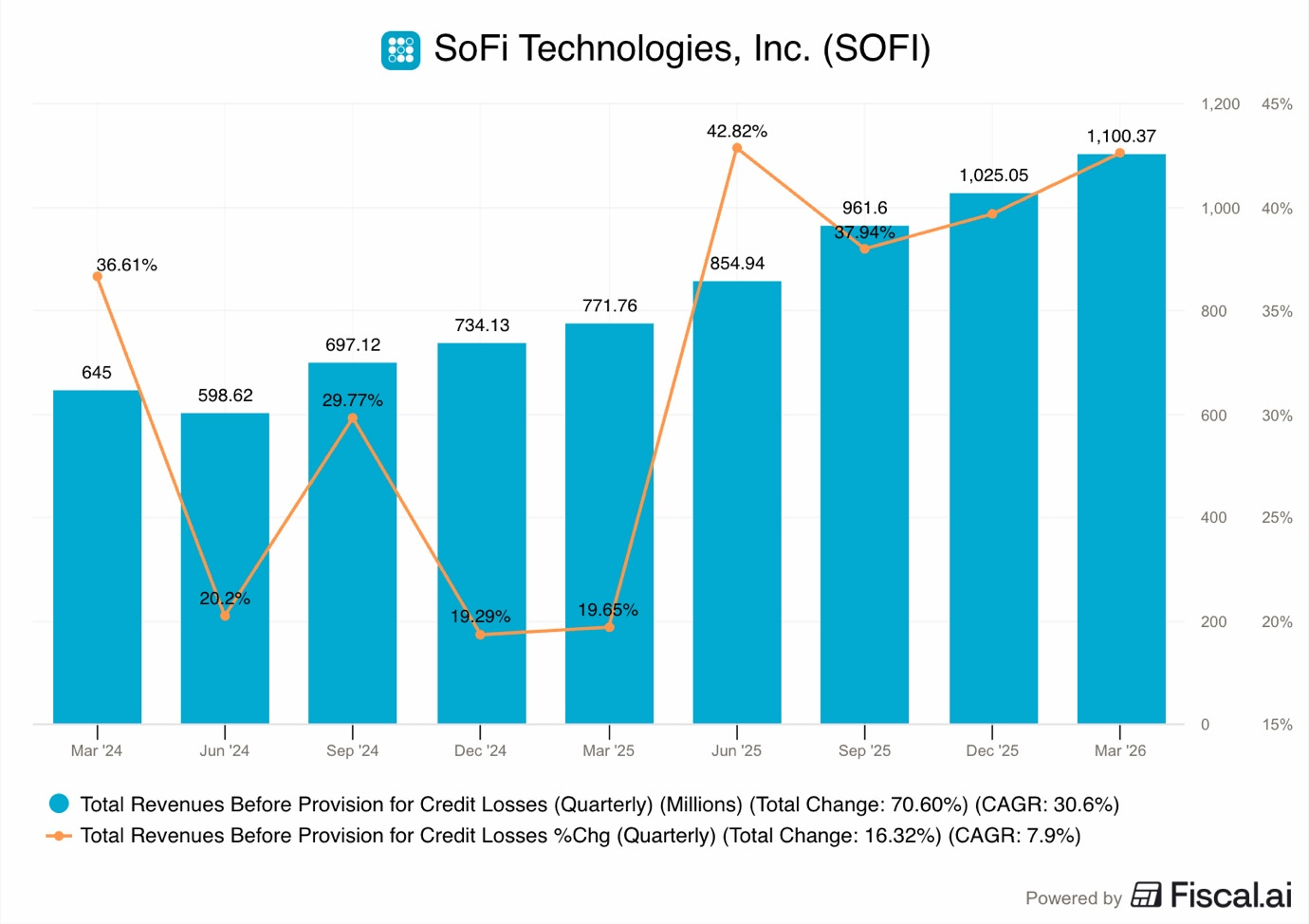

1.1. Revenue

The company brought in $1.1B in GAAP revenue, which is a 43% Y/Y increase from the $771.8M it made in Q1 2025.

As you can see in the graph above, Sofi demonstrated strong acceleration from the 19.65% growth it had in Q1 of 2025.

This growth is much faster than what legacy banks and other fintechs are seeing right now and is largely driven by the lending business, on which we will expand in a bit.

A big part of this money came from Net Interest Income, which reached $693M, up 39% Y/Y.

Sofi is making more money from interest because it is using member deposits to fund its loans, which are cheaper than other ways to get money.

Meanwhile, gee-based revenue reached $386.8M, up 23% Y/Y. This includes money from the loan platform business and fees from credit cards and investing. While this is growing, it is not growing as fast as the interest income.

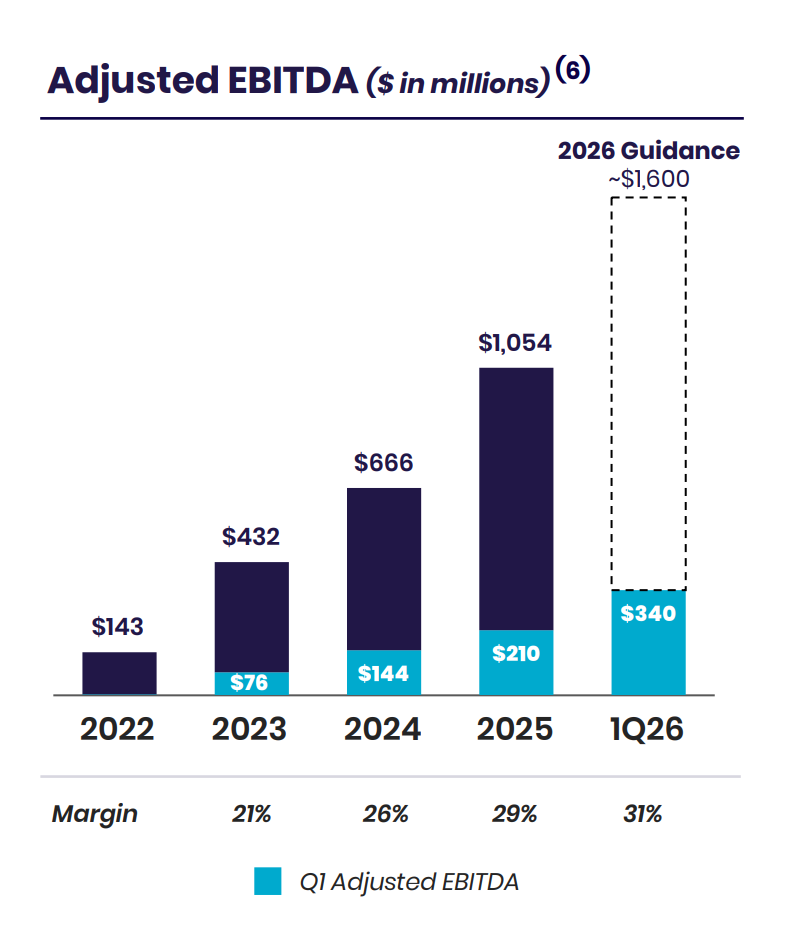

1.2. ADJ EBITDA

ADJ EBITDA is Sofi’s preferred way to see how much money the business makes from its daily operations.

In Q1 2026, ADJ EBITDA was a record $339.9M, which is 62% higher than the $210.3M made in Q1 2025.

The ADJ EBITDA margin was 31%, showing that the company is getting more efficient with each quarter.

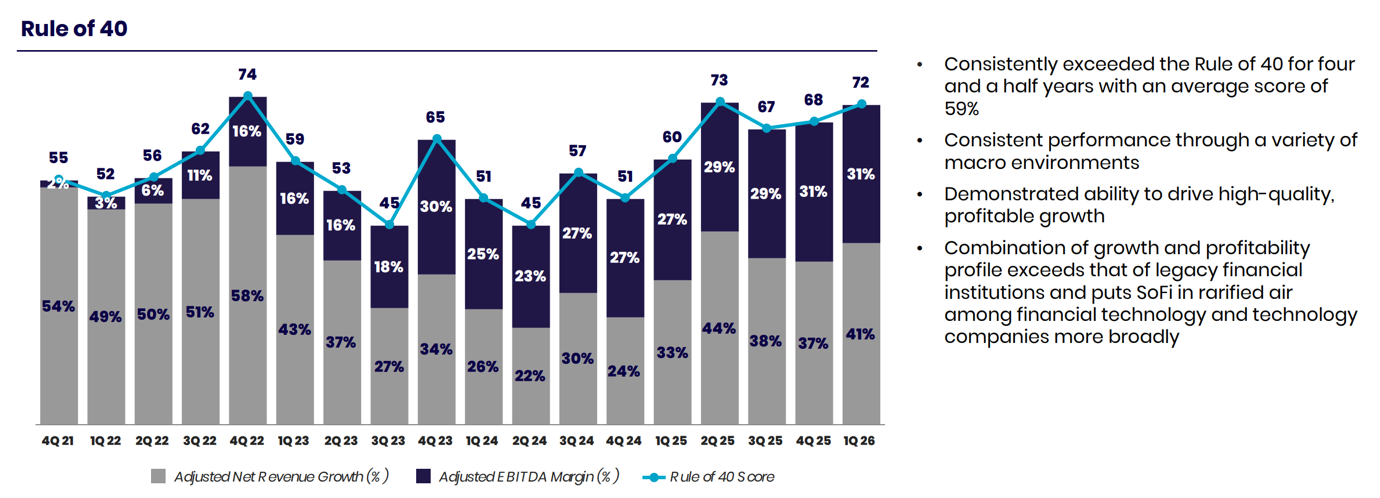

Sofi also emphasizes the Rule of 40 metric, which is popular with tech companies, where you sum the growth rate and the profit margin. If the score is above 40, it is considered that the company is achieving a great combination of growth and operating leverage.

Sofi had a score of 72 in Q1 2026. This was the 18th quarter in a row that Sofi has beaten this goal.

Furthermore, Sofi reported and incremental EBITDA margin of 41% means that for every new dollar of revenue, 41 cents went straight to profit.

This shows that Sofi’s business model is working. The more members they get, the more profit they make because they don’t have to spend as much to serve each new person.

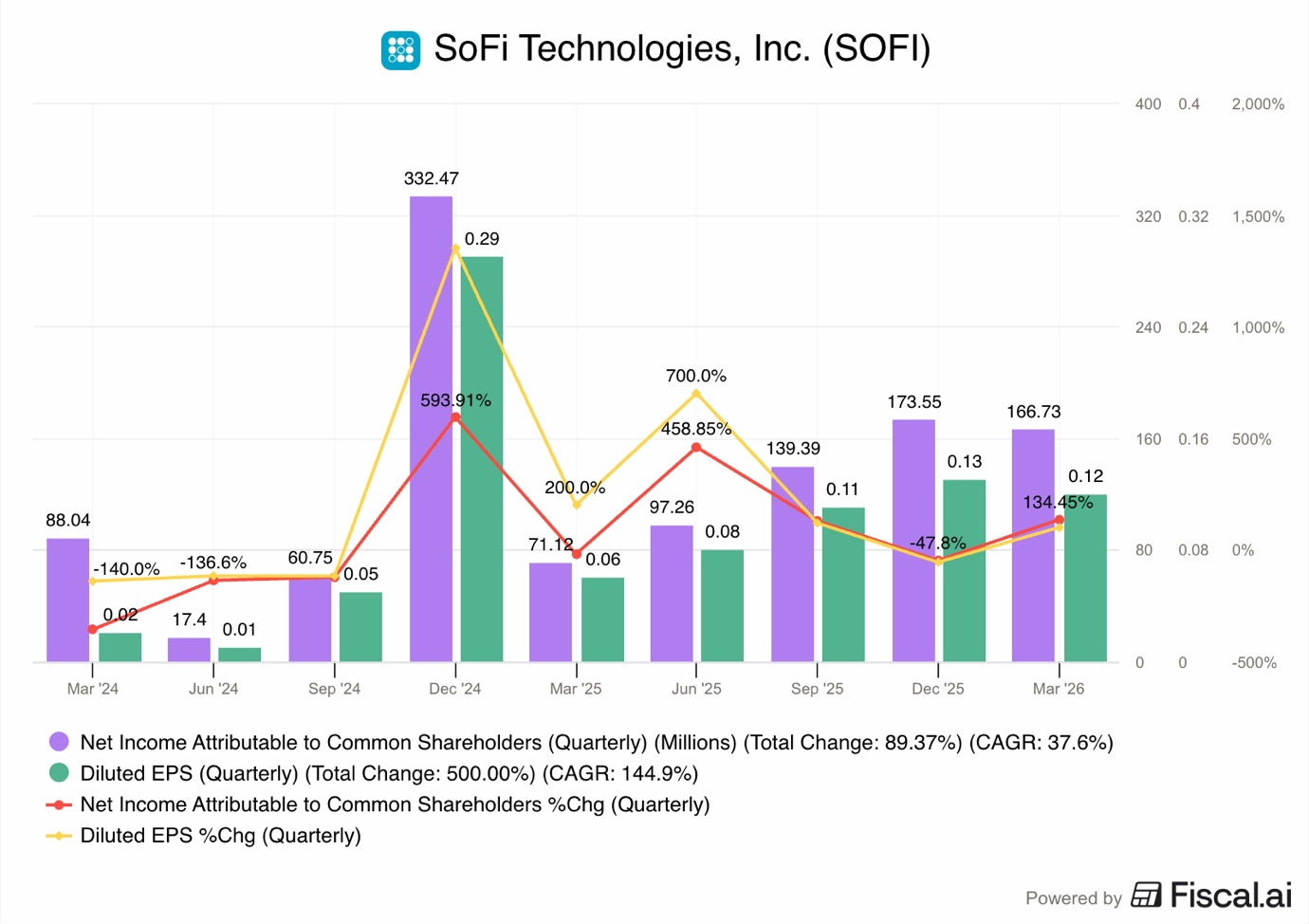

1.3. Net Income and EPS

For Q1 2026, GAAP net income was $166.7M. This is a massive jump of 134% Y/Y from the $71.1M made last year. This resulted in an EPS of $0.12.

This number was exactly what analysts expected, but it was not a beat like in previous quarters.

EPS grew by 100%, significantly lower than the 134% net income growth. This is because of Sofi issuing new shares and diluting shareholders.

The net income margin was 15%, which is double what it was in Q1 2025. Management also mentioned that if the stock price had not changed, the EPS would have been $0.13.

This is because the way they account for some stock-based costs depends on the share price.

The Tangible Book Value per share is now $7.21, up 57% Y/Y.

This is a very important metric for banks. It shows the actual value of the assets the company owns.

The fact that this is growing so fast suggests the company is becoming much more valuable, even if the stock market is currently disagreeing.

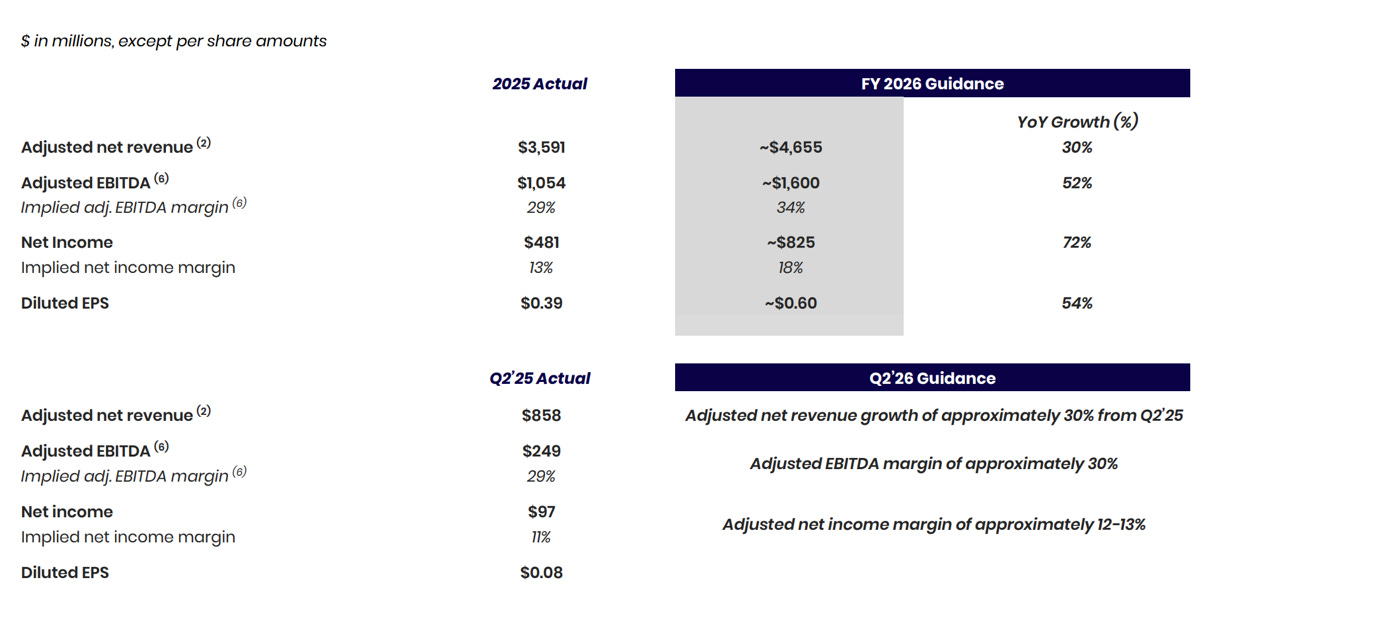

1.4. Guidance

As I mentioned in the introduction, guidance was the disappointment that caused the stock to sell off so much.

For Q2 2026, Sofi expects ADJ net revenue to be about $1.115B, which is 30% growth Y/Y. They expect an ADJ EBITDA margin of 30% and an EPS of $0.10 to $0.11.

The problem for investors was that Sofi did not raise its full-year 2026 guidance.

They still expect about $4.655B in revenue and $0.60 in EPS for the whole year.

Usually, if a company has a record Q1, they raise their goals for the year.

By keeping them the same, it looked like they expect a slowdown later in 2026.

In an interview with Bloomberg, CEO Anthony Noto explained that they made the guidance before the Iran War. At that point, they expected 2 rate cuts to happen in 2026 and modeled their performance accordingly.

Due to Trump’s actions in Iran, that seems unlikely now, as oil, natural gas, fertilizer, and other commodity prices have risen substantially.

2. Tech Platform

The “AWS of Fintech” bull case is officially dead!

Revenue for the Tech Platform was only $75.1M. This is a 27% drop from the $102.9M it made in Q1 2025.

Even worse, it was a 38% drop from the $122M it made just last quarter in Q4 2025.

This part of the company is supposed to be the tech in fintech, providing the backend systems for other banks.

The main reason for this failure was the loss of a very large customer. While Sofi did not name them in every report, it is known to be Chime.

Chime moved its business off Sofi’s platform at the end of 2025, and the loss of that money was felt heavily this quarter.

The number of accounts on the platform also fell 16% Y/Y to 133M.

This segment was supposed to be a high-margin business that didn’t need a lot of capital, but right now it is struggling to find its footing. Management says that if you ignore the lost customer, the segment actually grew 12% Y/Y, but even that is patheticaly slow growth.

Because the performance was so bad, Sofi is rebranding the whole segment.

It will now be called Sofi Technology Solutions.

They are also changing how they sell the product. Instead of just selling to small fintechs, they are trying to sell to big banks. They have broken the business into four areas:

Processing

Banking Core and Services

Payment Hub

Risk and Fraud

Management hopes this change will help the segment grow by 20% to 25% in the future.

They also noted that 13 new clients started using the platform this quarter, but they are clearly much smaller than Chime was.

For many bears, the performance of this segment clearly shows that Sofi might just be a bank and not a fast-growing tech company.

Unless the SofiUSD revenue scales and gets reported in this segment, I am skeptical that things can be turned around. We have been hearing one excuse after another for 3 years now.

First, it was because the fintechs didn’t have the budget for upgrades after the 2022 stock market crash.

Then, it was because inflation and high interest rates reduced capex budgets.

Now, it’s because of the Iran War.

The execution in this segment has been poor and extremely disappointing from Anthony Noto and the Sofi team.

It could be that the TAM for this segment is much lower than the company hoped, or that many fintechs and banks don’t want to help fund their competitor.

Do you like this report?

Become a Paid Premium member to see dozens of exclusive pay-walled equity research reports such as this.

Curious about which stock I own?

Full portfolio with all holdings, cost basis, and unrealised gains is visible to Premium members. I do weekly updates and detailed monthly reviews. Premium members are also notified of all sales and purchases using the pay-walled Substack Chat.

The annual plan is available for 50% cheaper per month than the monthly plan.

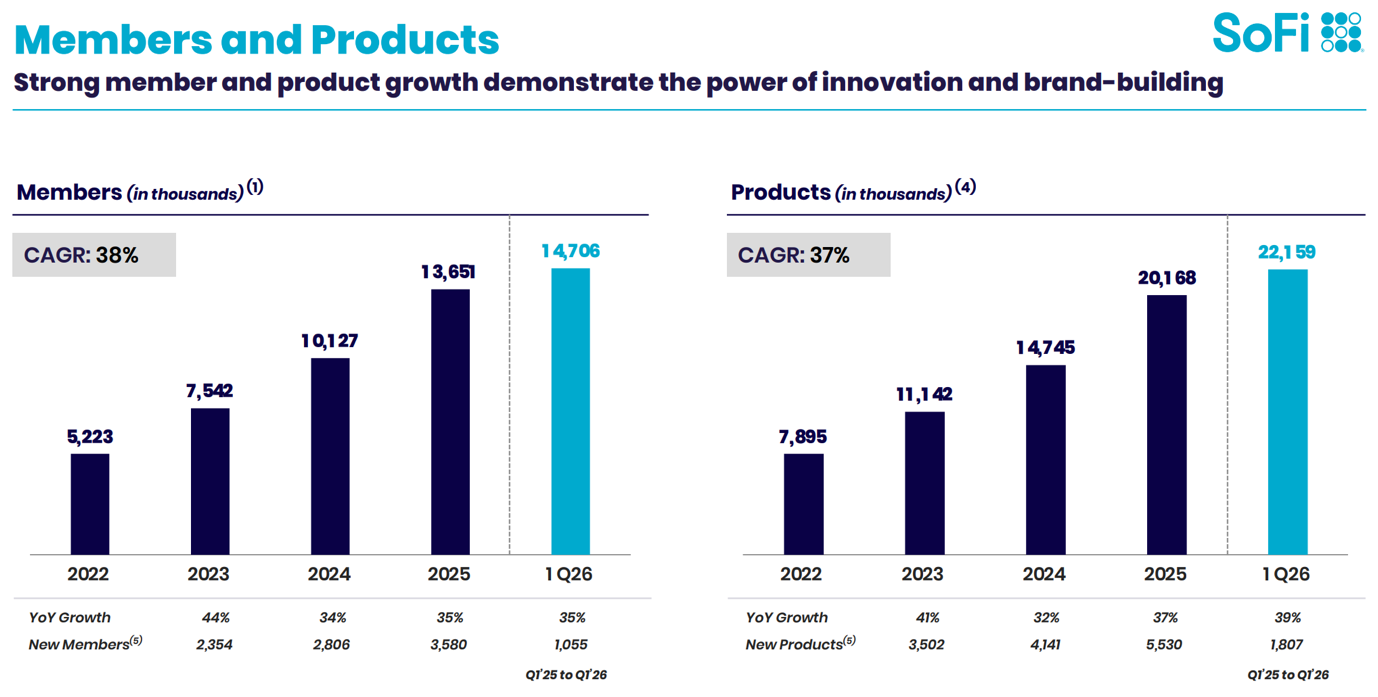

3. Member and Product Growth

While the technology business is struggling, the banking business is growing very fast.

Sofi is very good at getting new members and selling them more than one product. Sofi calls this the Financial Services Productivity Loop. The more products a member uses, the more money Sofi makes, and the less it has to spend on ads.

In Q1 2026, Sofi added 1.1M new members. This is a record and brings the total number of members to 14.7M, which is up 35% Y/Y.

It is extremely impressive for a company of this size to keep growing its customer base at such a rapid pace.

The total number of products reached 22.2M, up 39% Y/Y.

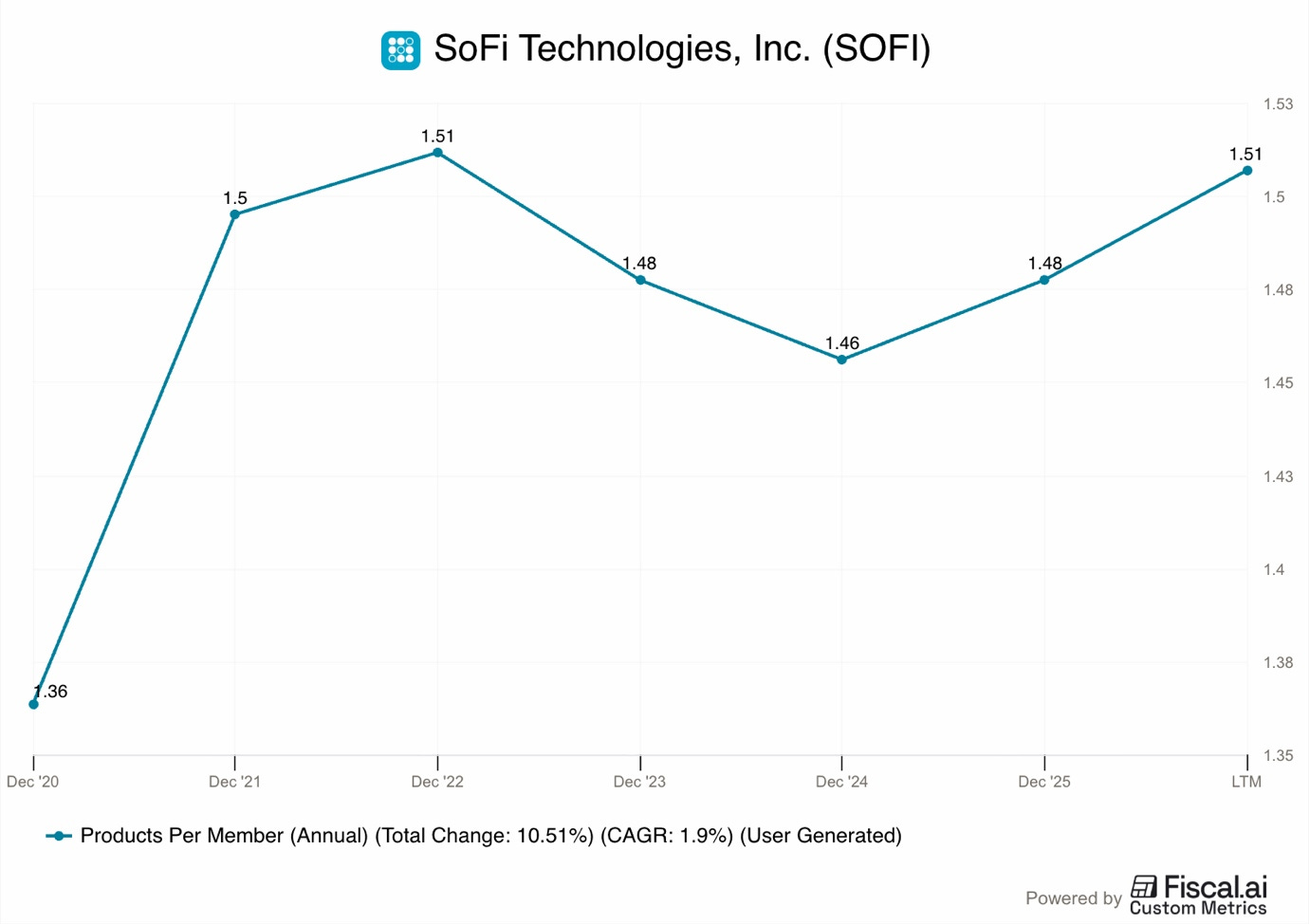

This means that the average member has about 1.5 products with Sofi. A very important number is the cross-buy rate. This shows how many new products were opened by people who were already members. In Q1 2026, this was 43%, up from 36% a year ago.

This is great for Sofi because it’s much cheaper to sell to an existing customer than to find a new one.

As you can see in the chart above, this is a 10.5% improvement from 2020. However, it has not been growing very fast. This is largely because Sofi keeps growing the number of customers, which is their priority.

Once it becomes harder to acquire new users, Sofi will focus more on driving up the product per member.

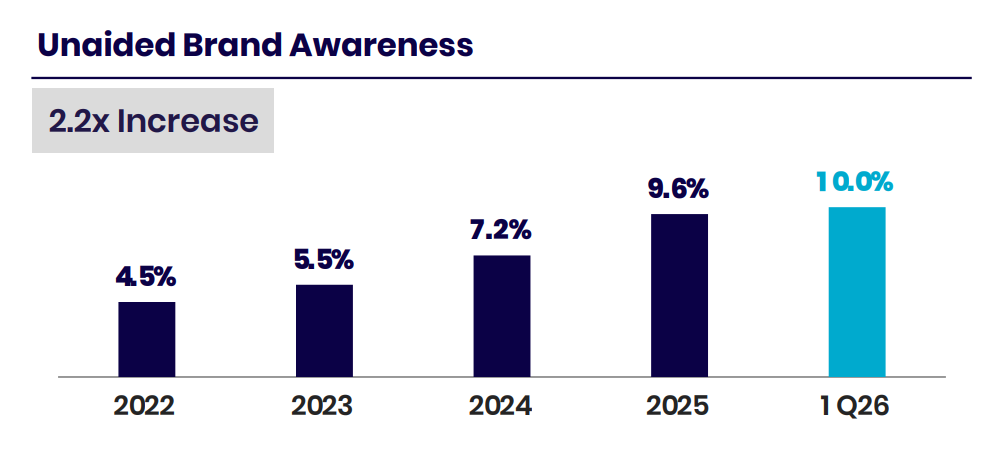

Sofi’s brand is also getting much stronger.

Unaided brand awareness hit 10% this quarter. This means that when you ask people to name a bank, 10% of them say Sofi without being prompted.

This is double the level of 2022. Sofi was also named the #1 U.S. Bank by Forbes and ranked #1 for DIY investor satisfaction by J.D. Power.

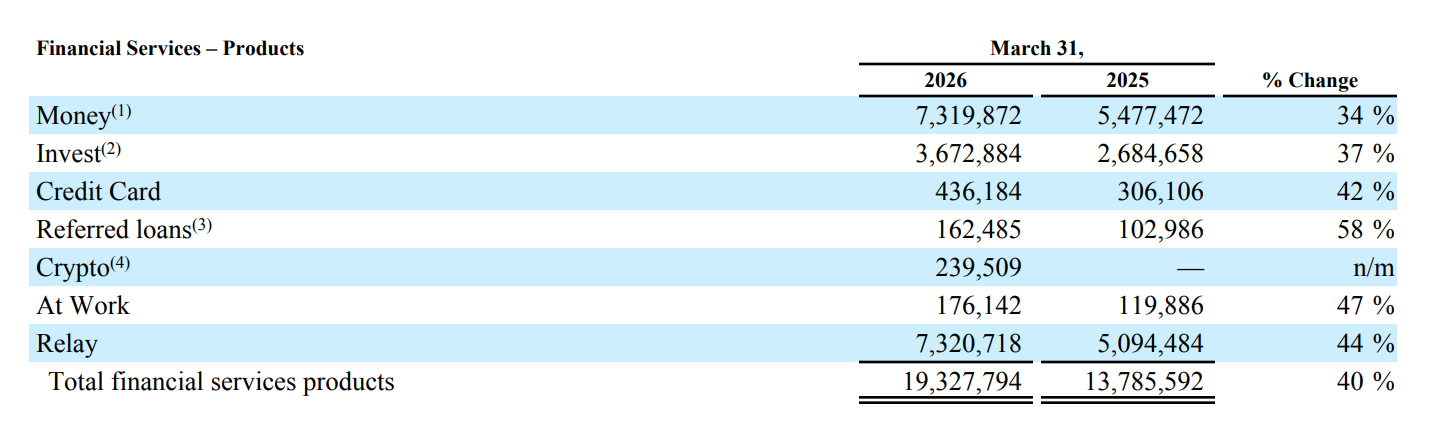

Much of the growth is coming from financial services products like Money and Relay. These products grew by 34% and 44% Y/Y.

But interestingly, Crypto products reached 239.5K after launching in Q4 2025.

This is a really strong growth in a single quarter, especially considering that crypto and growth stocks have not been doing that well since the Iran War.

Meanwhile, lending products also grew by 33%, driven by personal and home loans.

4. Lending

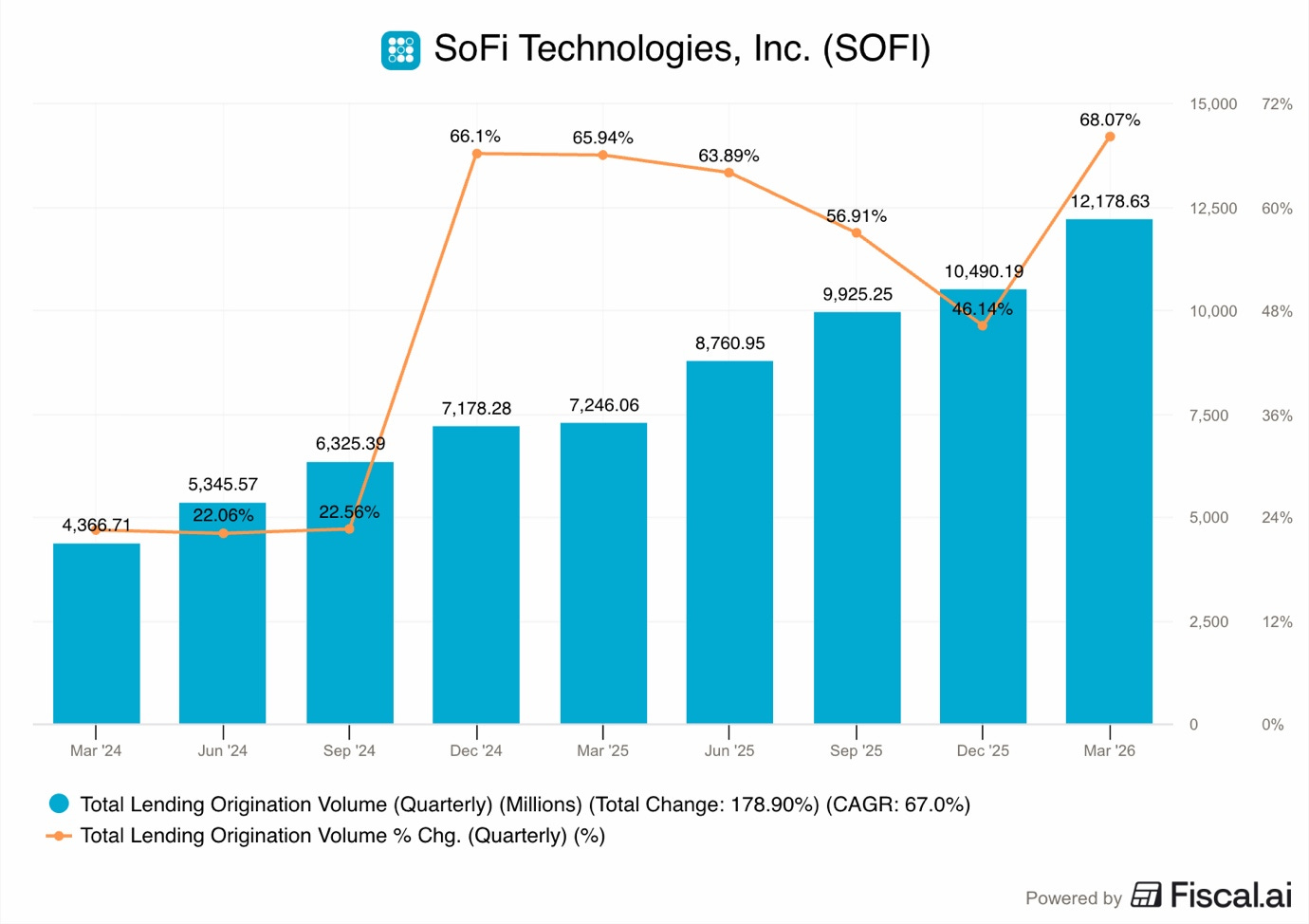

The lending segment is still the biggest part of Sofi’s business, and in Q1 2026, the segment was running at full speed.

Total loan originations hit $12.2B, +68% Y/Y from the $7.2B originated in Q1 2025 and +16% Q/Q from $10.49B in Q4 2025.

As you can see in the chart above, it was the strongest Y/Y lending growth in 9 quarters and an acceleration from Q4 2025.

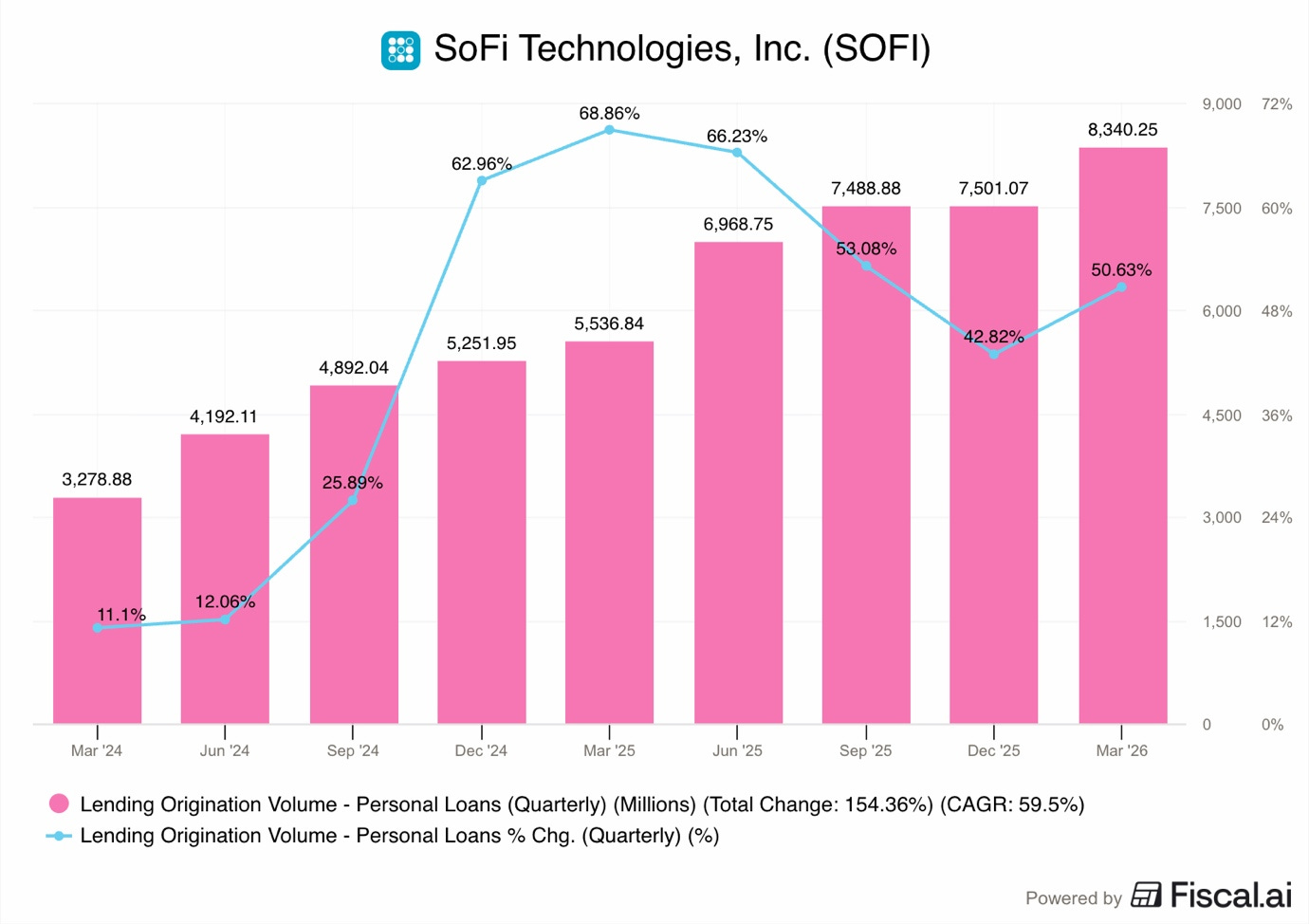

Personal loans were the largest part of this, reaching $8.3B, up 51% Y/Y.

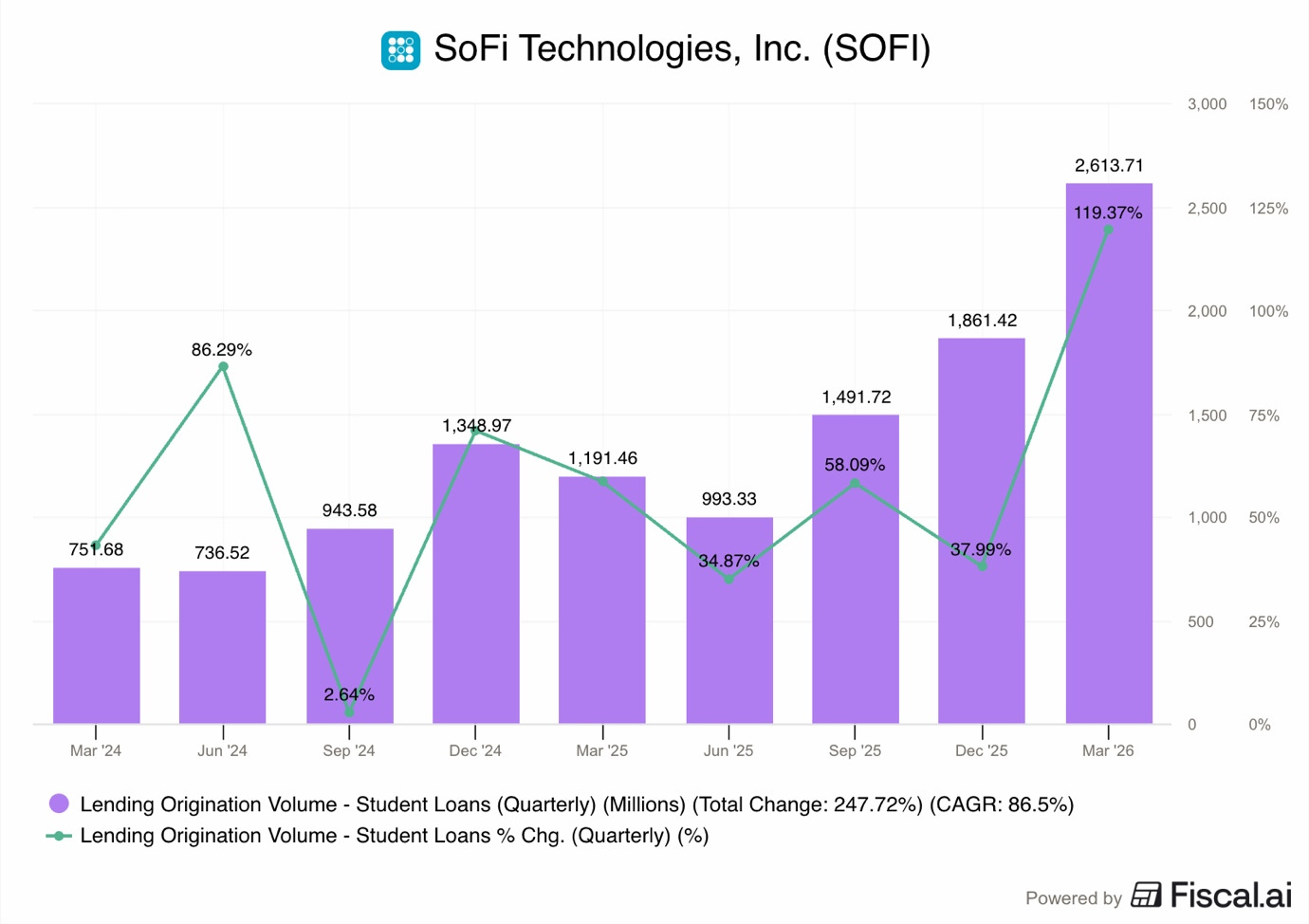

Whilst student loan originations accelerated massively, jumping 119% Y/Y to $2.6B.

This is the result of the Trump administration restarting student loan repayments that the Biden administration stopped during COVID. People are looking to refinance their student debt as they notice higher interest charges hitting their bank accounts.

This is how Sofi acquires high-value customers. By offering affordable loan refinancing, it is acquiring university graduates early in their careers. Then Sofi moves them down in the funnel, upselling them new products, like mortgages, which was suge growth this quarter.

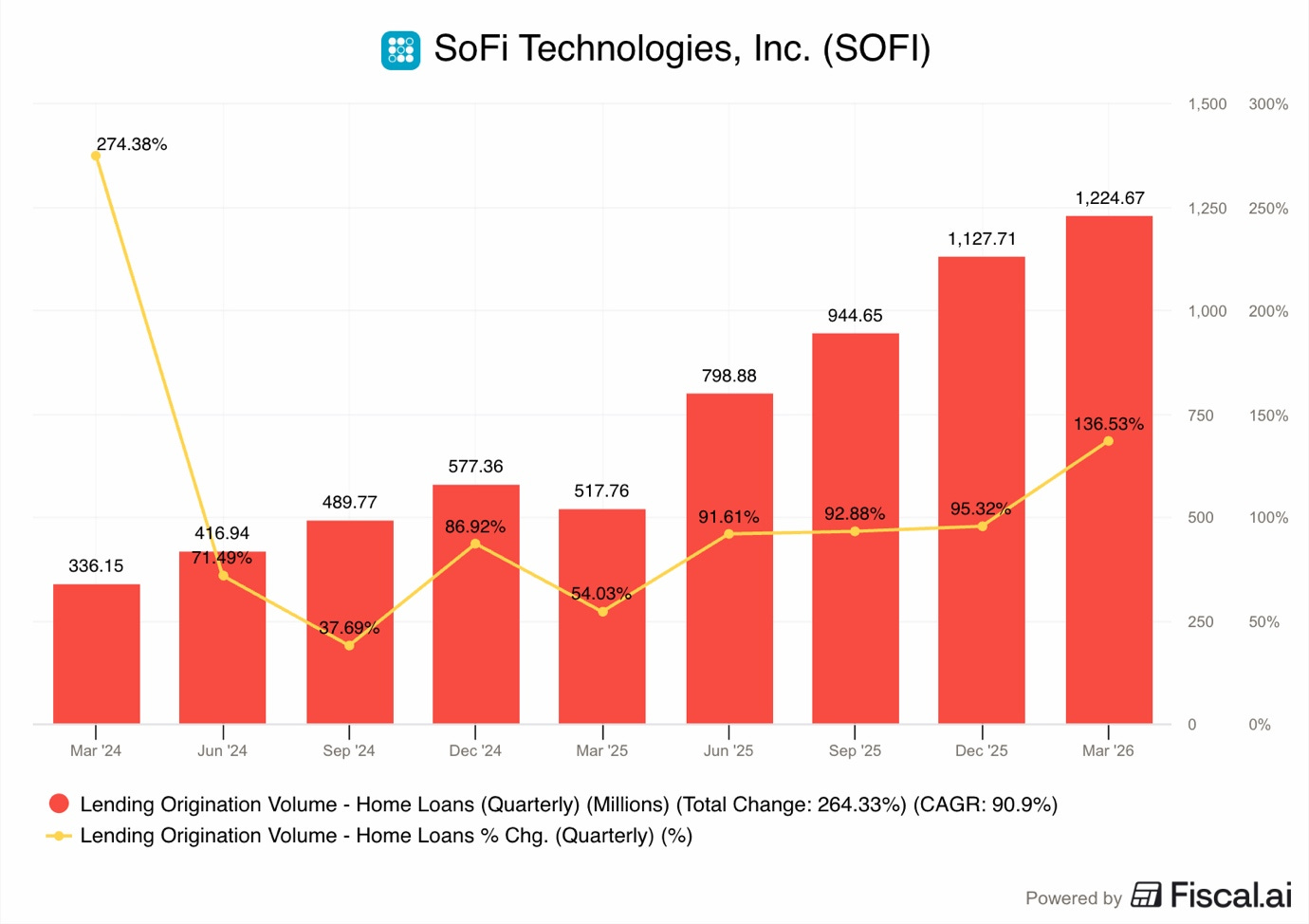

Home loans also saw huge growth, up 137% Y/Y to $1.2B.

This is an area that the company is increasing its focus on, in preparation for a possible real estate boom, which could happen if interest rates come down in the US.

Recently, Sofi announced its expansion into home equity lines of credit (HELOC). This allows people who own a home to borrow money against the appreciated equity value, even if the mortgage has not been fully paid off. This has become very popular because many people have a lot of equity in their homes as prices have risen in the last decade, but don’t want to sell

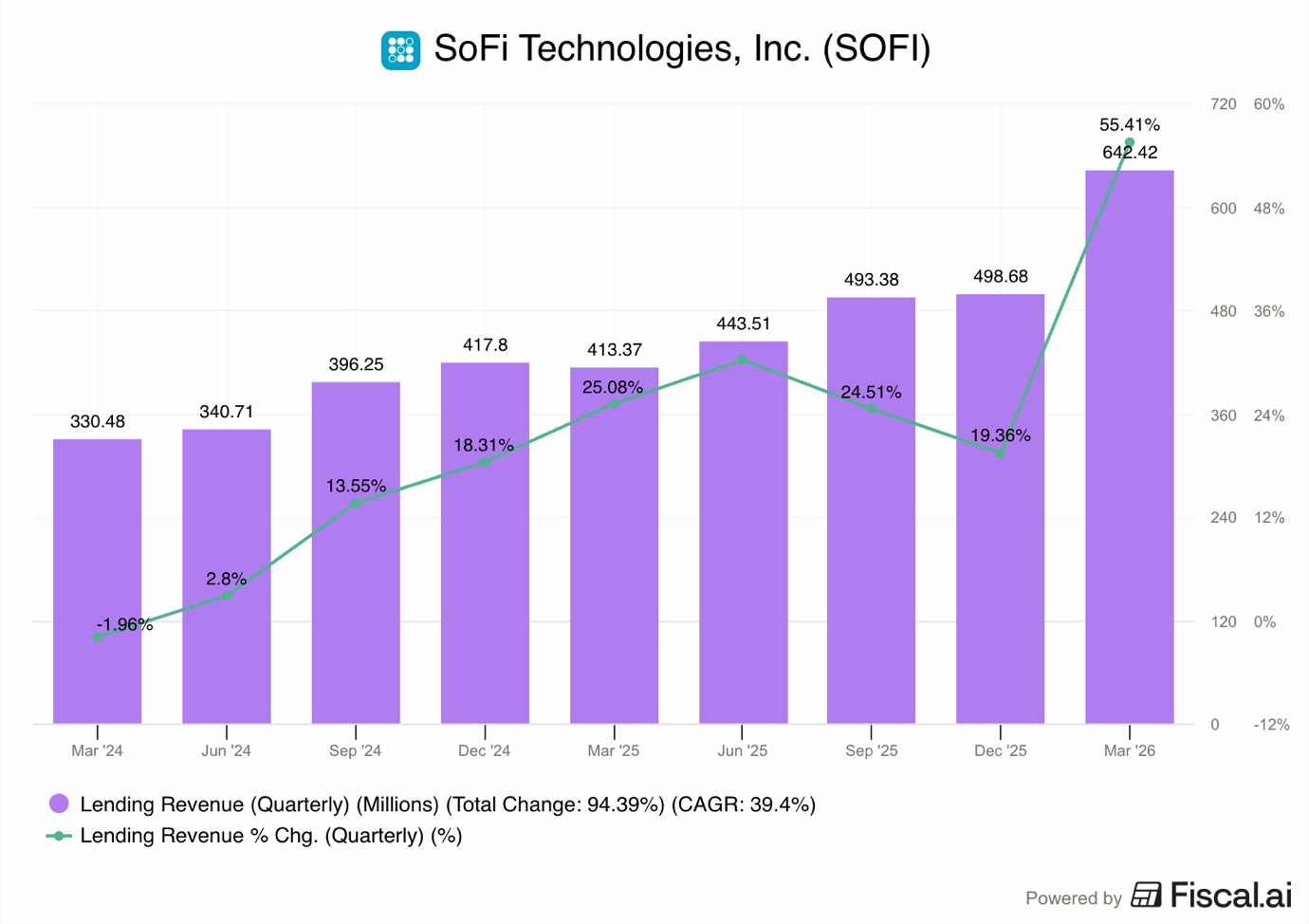

Overall, the revenues of the lending segment grew by 55.4% Y/Y to $642.4M.

In the chart above, you can clearly see that the company delivered strong Q/Q growth as well, growing by 28.9%.

This was the best growth in over 9 quarters!

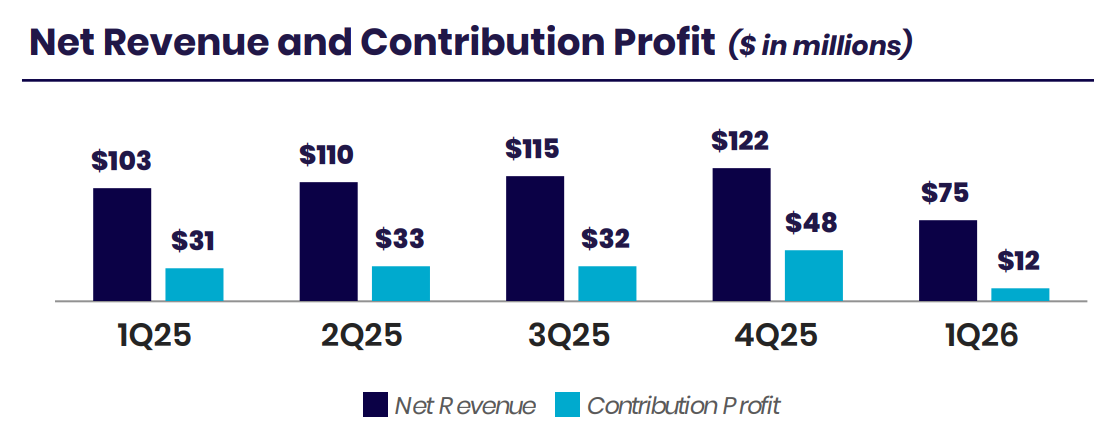

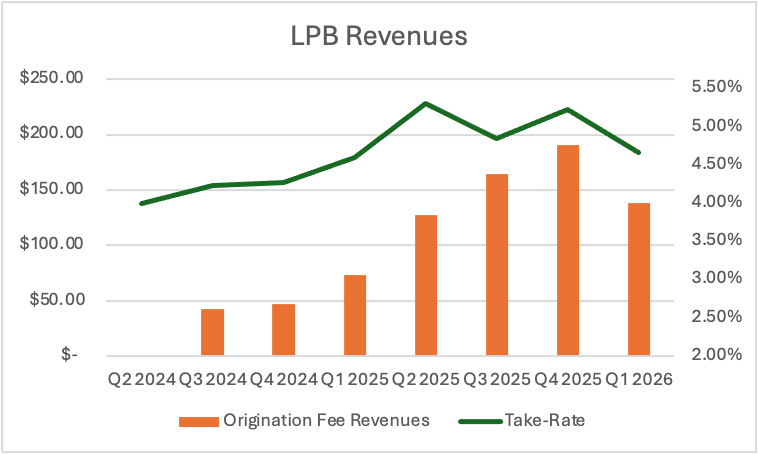

4.1. Loan Platform Business

The loan platform business has been a huge success and the company’s biggest innovation in the last 2 years.

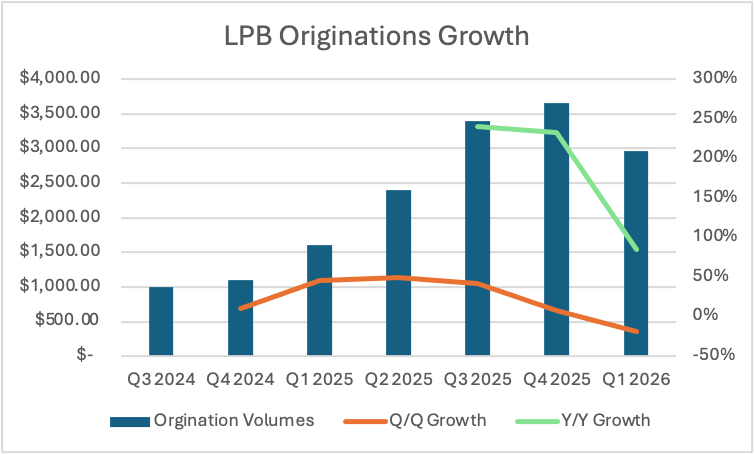

In Q1 2026, Sofi originated $2.96B on behalf of its partners, up 85% Y/Y.

While the growth looks impressive on a Y/Y basis, it was not as strong on a Q/Q basis, as you can see looking at the orange line in the graph above. Originations declined 19% sequantally, and this was part of the reason that added to the stock sell-off.

LPB generated $138.3M in revenues, which was a 88% Y/Y increase, but a 28% Q/Q decrease. Take-rate also went down from 5.22% in Q4 2025 to 4.67% this quarter.

Sofi CEO Anthony Noto later commented to Bloomberg and Yahoo Finance that this decline was not due to loss of interest from funders, but rather a focus on growing their own loan book. The fact that overall orignations grew so strongly, 68% Y/Y and 16% Q/Q, gives credence to this explanation.

The take rate may have fallen because there could be some volume incentives from the credit partner to issue more loans.

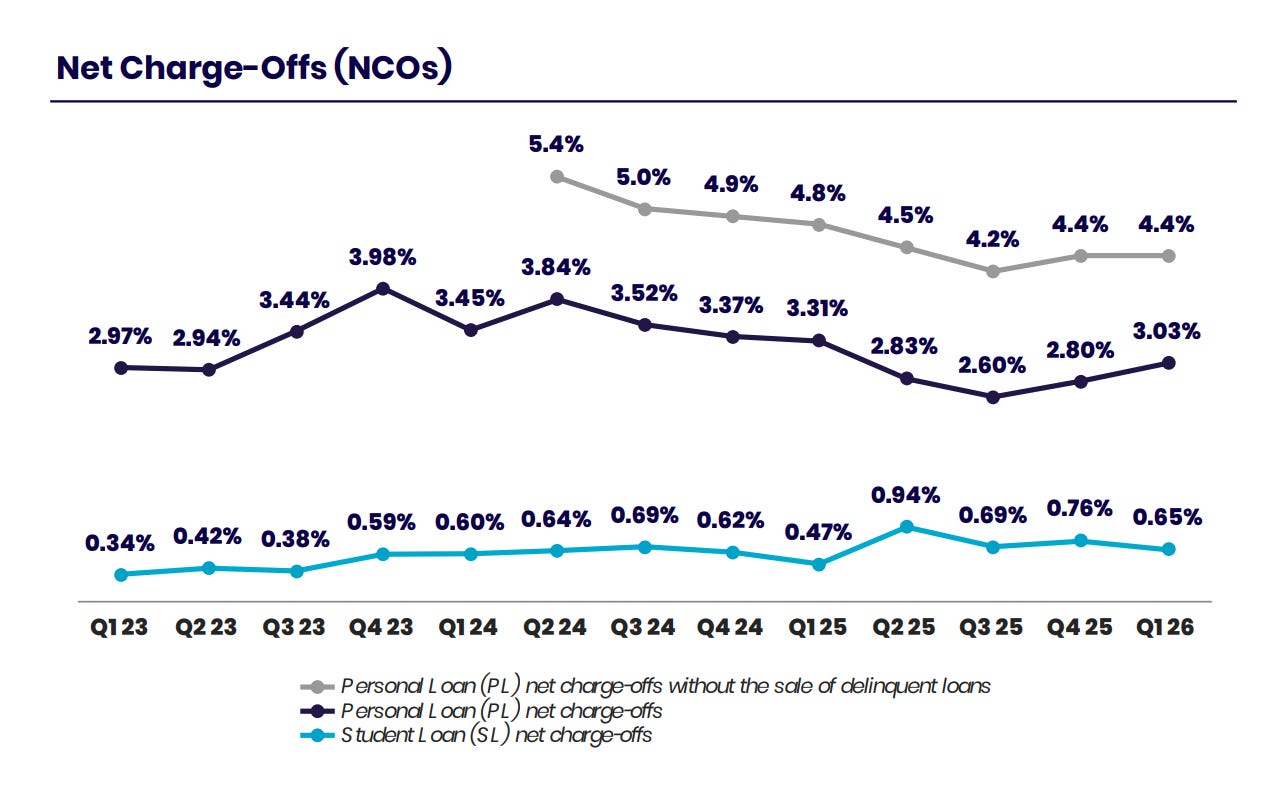

4.2. Credit Quality

Credit quality has always been a big topic for Sofi, especially since the short-sellers Muddy Waters recently claimed that Sofi’s loan book is riskier than the company claims.

They alleged that Sofi misstated $312M in debt and that the real charge-off rate for personal loans is 6.1%.

Sofi says these claims are “factually inaccurate and misleading”.

They reported a personal loan net charge-off rate of 3.03% for the quarter. This is up from 2.80% last quarter but down from 3.31% a year ago.

If you include the delinquent loans that Sofi sold, the rate would be 4.4%.

Management says their losses are well within the 7% to 8% range they planned for.

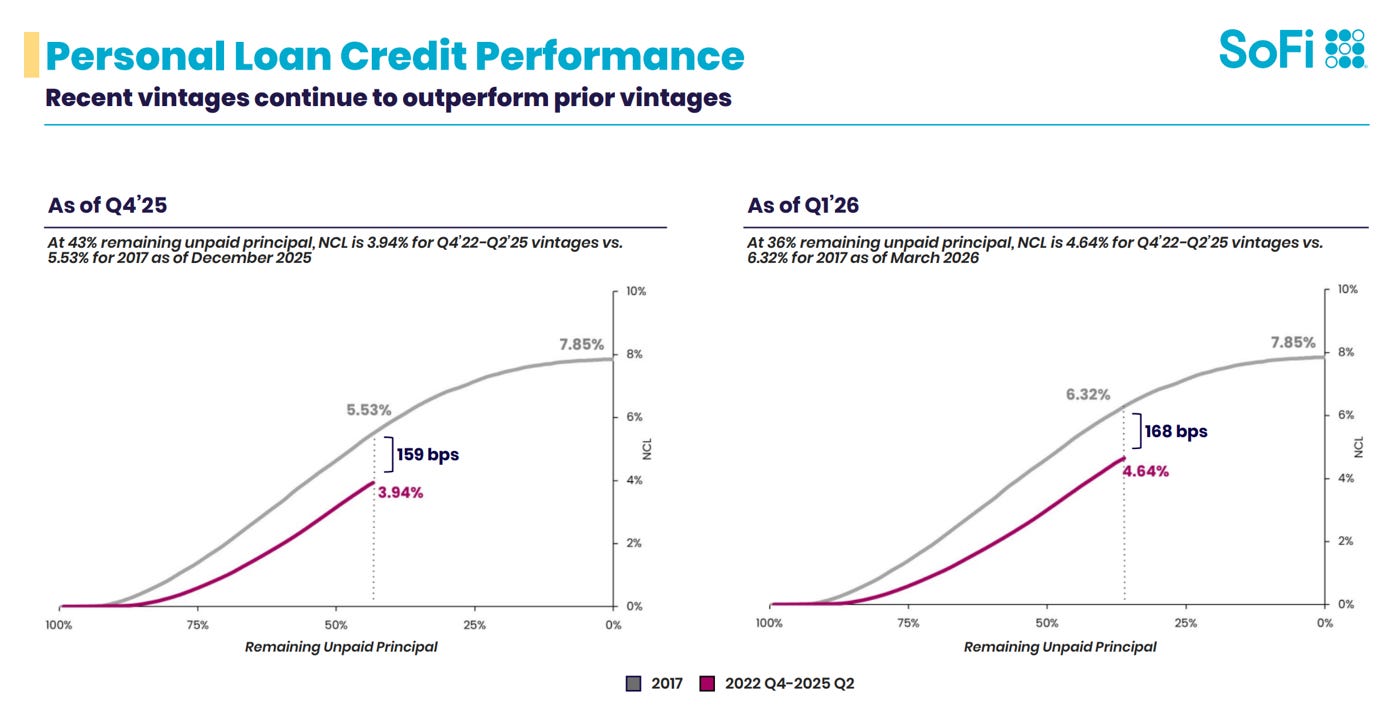

Furthermore, looking at historic loan quality vintages, we see that Sofi loans today are performing much better than the loans the company issued in 2017.

As of Q4 2025, 43% of the unpaid principal remained from issued loans.

3.94% of that was in default, compared to 5.93% at the same maturity for loans issued in 2017, a gap of 159 basis points.

As of Q1 2026, we see that the gap is improving, with 4.64% of loans in default compared to 6.32%, 168% basis points.

Simply put, Sofi defaults are lower than in 2017, despite issuing multiples more loans, because they are issuing less risky loans to richer people.

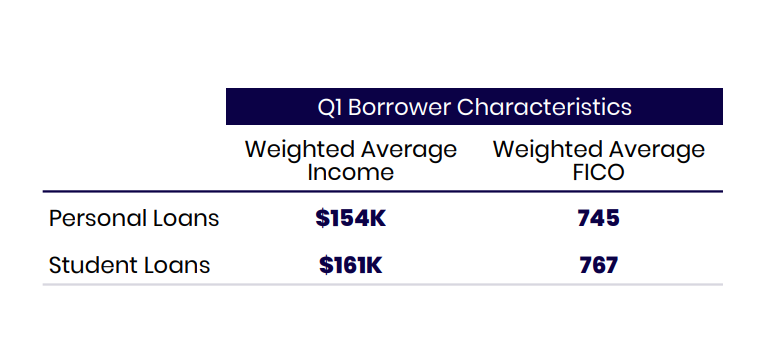

There is nothing to worry about, as the average Sofi personal loan borrower has an income of $154,000 and a credit score of 745. These are very high-quality borrowers. The student loan charge-off rate is even lower at just 0.65%.

Overall, Sofi’s credit performance seems stable, but the market remains nervous because of the short-seller reports.

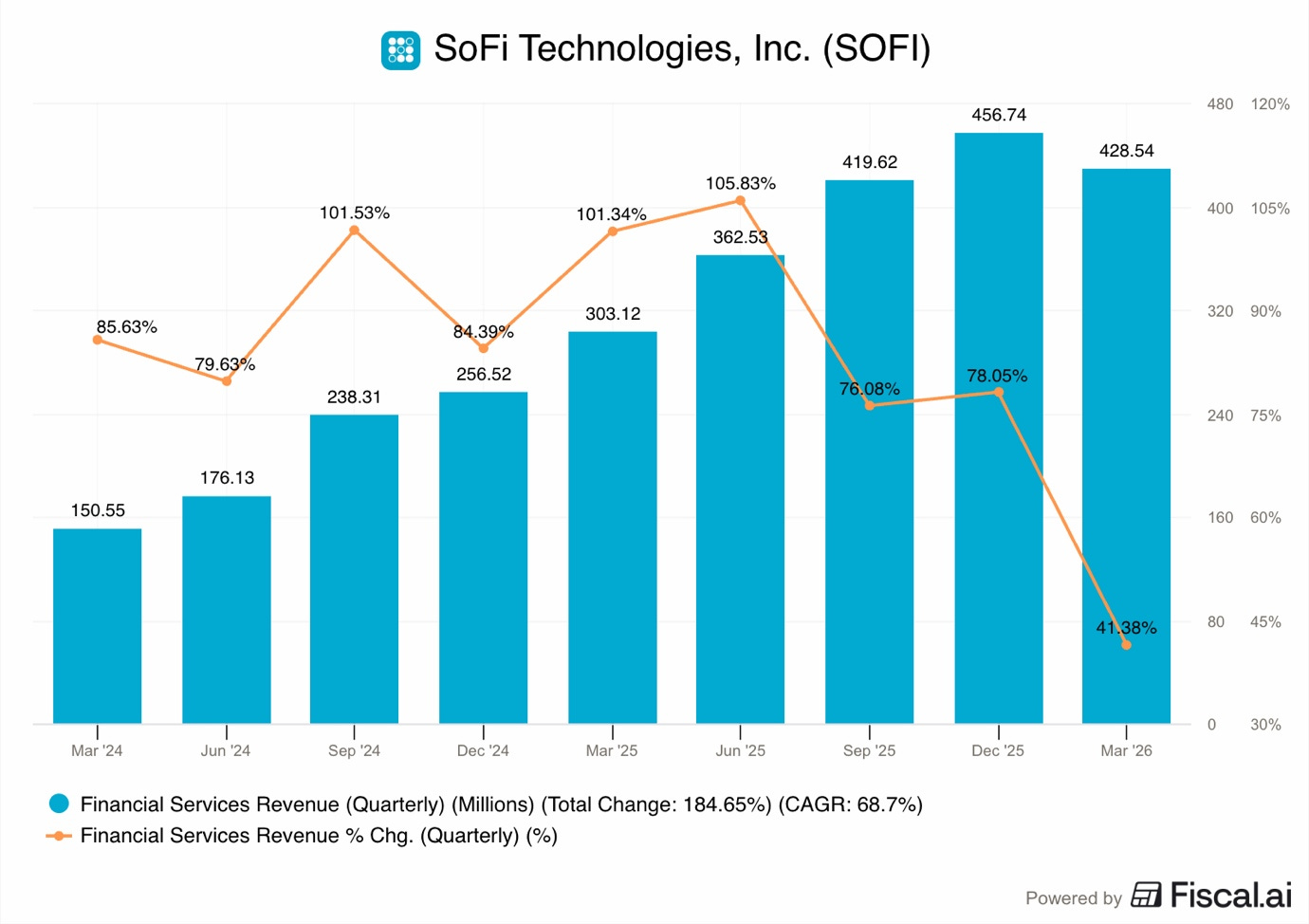

5. Financial Services

The Financial Services segment Revenue was $428.5M, up 41% Y/Y.

This was a meaningful deceleartion, and the worst growth quarter in over 9 quarters!

This was one of the reasons the stock sold off, but it doesn’t make much sense to me, as all other segments performed strongly.

I have to note that the LPB revenues are reported here, not part of lending, as lending revenues are where Sofi actually holds the loans on its balance sheet. The $50M Q/Q decrease in LPB revenues was essentially the main reason why this segment decelerated.

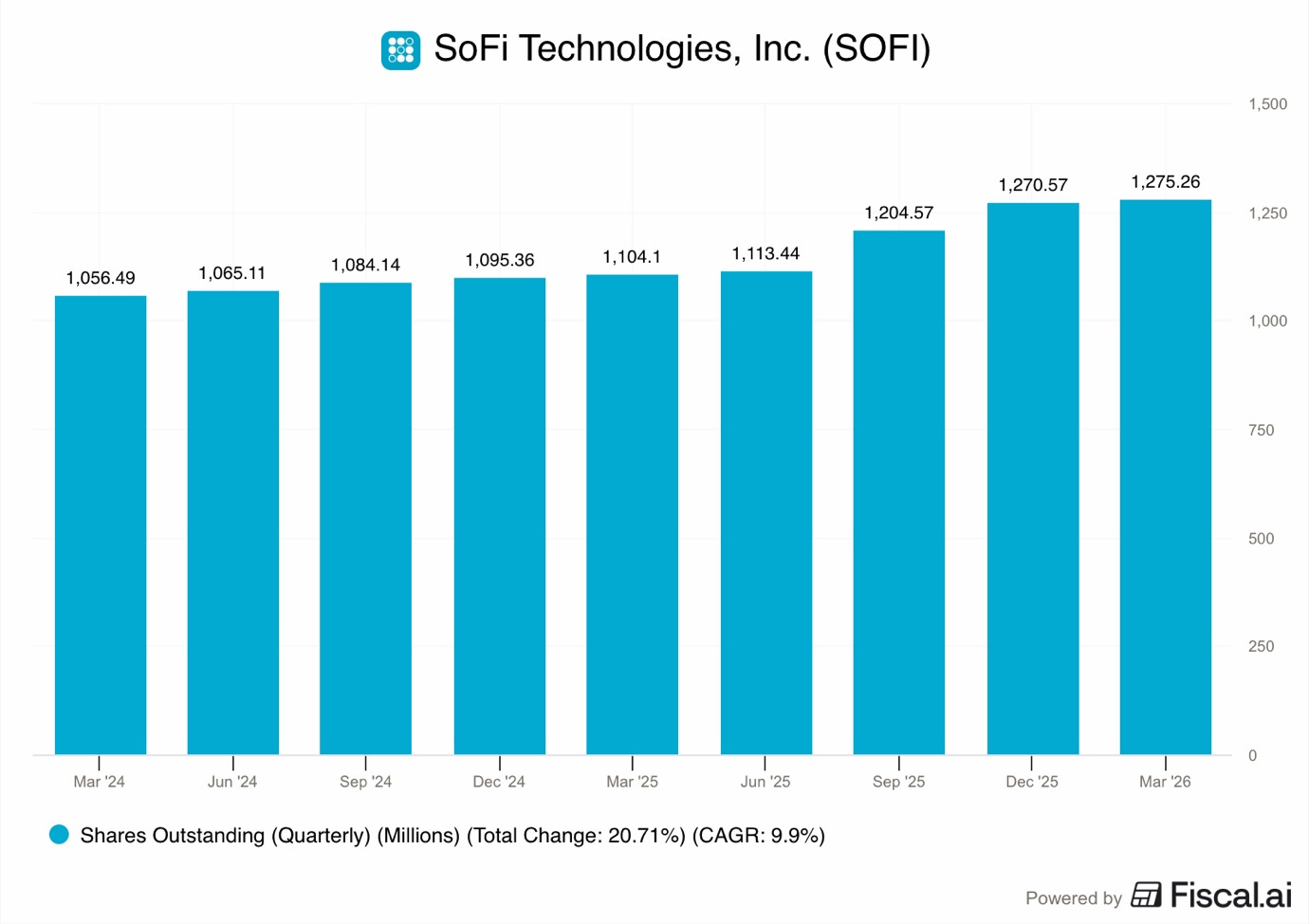

6. Dilution

The narrative is that Sofi is a heavily diluting company!

But that is simply not the case, as all dilution needs to be looked at in the context of the financial results delivered.

In the last 2 years, Sofi has been steadily increasing the number of shares outstanding by 10% per year.

During this time, revenues have grown with a 30.6% CAGR, while EPS has grown with 27.5% CAGR.

It is clear that Sofi dilution is smart, balanced, with a clear strategy, and most importantly, not financially dilutive.

However, by now, it is also clear that the last 2 dilutions were a strategic mistake, despite it not being a financial mistake.

It’s the only criticism that I see repeated again and again in comments, “Noto diluted,

is a terrible company, dilution is bad”.

I suspect that this dilution was actually the real reason why Muddypants attacked Sofi. They saw that this bear narrative is strong and persistent, and wanted to cash in on it by adding gasoline to it.

There is no objective metric by which Sofi could be a “terrible company”, yet this narrative persists because of the dilution and stock performance.

During the earnings call, they said that these note issuances were not economically dilutive to the EPS. This is because Sofi used the $3B+ it raised to grow the EPS.

Simply put, the EPS is larger today than if they hadn’t diluted, even though the share count is higher.

Here is the real issue, investors don’t care about it.

They only care about the share count going up.

It doesn’t matter what Sofi does with the money, selling stock to raise funds is “bad, full stop” and the market doesn’t want Sofi to do that.

If Sofi had not done these raises, the share price today would be higher, even though the EPS would be lower.

That’s why I am saying that it was a strategic mistake, despite it not being a financial mistake.

However, in the long term, Sofi is delivering strong results, releasing new products, and growing EPS.

Just looking at the number of shares outstanding, without taking into account the incredible EPS growth the company is delivering, is simplistic and stupid.

The market will realize this as Sofi continues to execute quarter after quarter, and this dilution narrative will die.

7. Conclusion

The Q1 2026 report for Sofi shows a company that is doing two very different things.

On one hand, the banking business is a massive success. Members are joining in record numbers, they are using more products, and the company is making a solid profit.

The lending business is also breaking records, despite high interest rates, persistent inflation, and the Iran War.

On the other hand, the technology business is in trouble.

Losing Chime was a big hit, and the rebranding to “Sofi Technology Solutions” shows that the company is attempting to change its strategy to survive.

But most importantly, even though Sofi hit its profit goals, the fact that they didn’t raise their guidance for the rest of the year made investors think that the best growth might be behind them.

For the rest of 2026, Sofi has to prove that it can keep growing without the technology platform being a major drag.

They also have to show that their loans are as safe as they say they are, especially with short-sellers watching every move.

If they can do that, the company could be very valuable in the long run.

But for now, the stock remains very volatile as the market weighs the record growth against the risks.

However, I firmly believe that Sofi is one of the most undervalued long-term opportunities on the market.

So I will be releasing a new updated Sofi 2030 valuation model, with my earnings estimates and updated share price target.

It will be available for my premium subscribers on Sunday!

Here is what my Premium Members can expect:

Portfolio Review - Each month, I will present the portfolio performance and discuss my stock watchlist and my best ideas.

Recent developments.

Unwarranted pullbacks.

Insider activity.

Potential catalysts.

Deep Dives – 8,000+ word detailed analysis of a company, delivered in 3 Parts.

Part 1 – Brief History of the company and its Business Model.

Part 2 – Management, Moats, Competitors, and Risks.

Part 3 – Opportunities, Financial Analysis, and a Valuation Model.

You can expect a comprehensive research report that is educational, interesting, and provides actionable insights!

To see what you can expect, read my Palantir Deep Dive!

Members of the Premium service get access to my library of 12 Deep Dives and to all future Deep Dives, which will be released on semi-monthly basis.

Investment Cases – A short, concise report with actionable insights.

This report is about the size of a single part of a Deep Dive.

Focused Investment Thesis

Main drivers of the Bull Case

Valuation Model

To see what you can expect, read my Oscar Health Investment Case!

Earnings Reviews and Updates – For companies that are of great interest to me and my readers, I will provide regular quarterly or semi-annual updates after earnings reports.

Financial performance

Business Update

New developments

Updated Valuation Model

To see what you can expect, read my Google Q2 2025 Earnings Review!

Equity Research Report List

You can follow me on Social Media below:

X(Twitter): TheRayMyers

Threads: @global_equity_briefing

LinkedIn: TheRayMyers

Disclaimer: Global Equity Briefing by Ray Myers

The information provided in the “Global Equity Briefing” newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. Ray Myers, as the author, is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented in this newsletter is based on publicly available information and sources believed to be reliable. However, Ray Myers does not guarantee the accuracy, completeness, or timeliness of the information provided. The author assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned in the “Global Equity Briefing” report. Any investment decisions made based on the information in this newsletter are at the sole discretion of the reader, and they assume full responsibility for their own investment activities.

Really Nice analysis! thank you very much!